Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the local (in time) expansion of a continuous-time process and its conditional moments, including the process' characteristic function. The expansions are conducted by using the properties of...

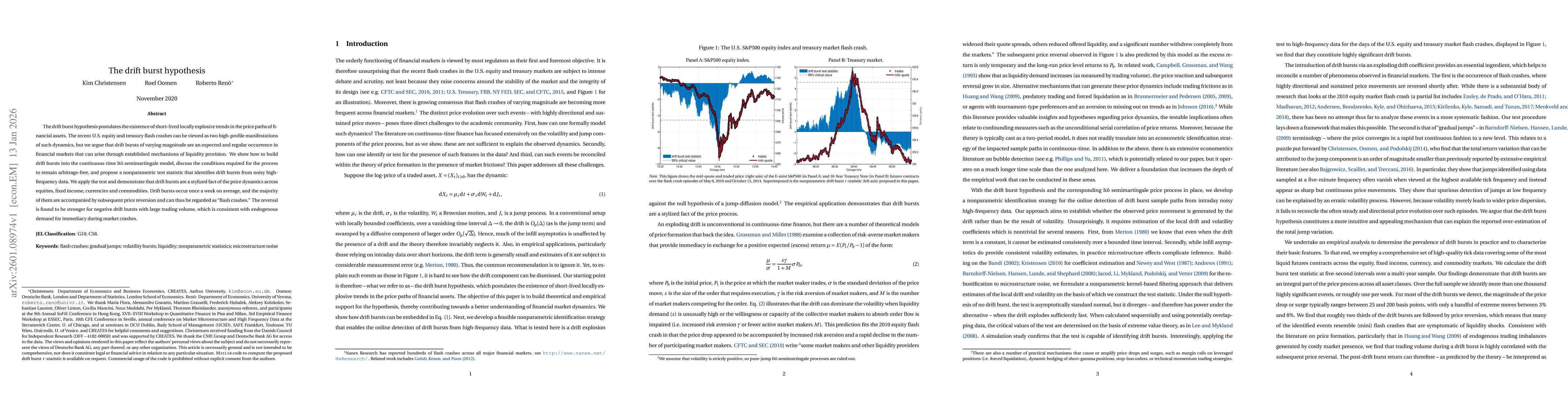

The drift burst hypothesis postulates the existence of short-lived locally explosive trends in the price paths of financial assets. The recent U.S. equity and treasury flash crashes can be viewed as t...

We study the trading activity of designated market makers (DMMs) in electronic markets using a unique dataset with audit-trail information on trader classification. DMMs may either adhere to their mar...

Options with maturities below one week, hereafter "ultra-short-term" options, have seen a sharp increase in trading activity in recent years. Yet, these instruments are difficult to price jointly usin...