Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper develops a general framework for stochastic modeling of goals and other events in football (soccer) matches. The events are modelled as Cox processes (doubly stochastic Poisson processes)...

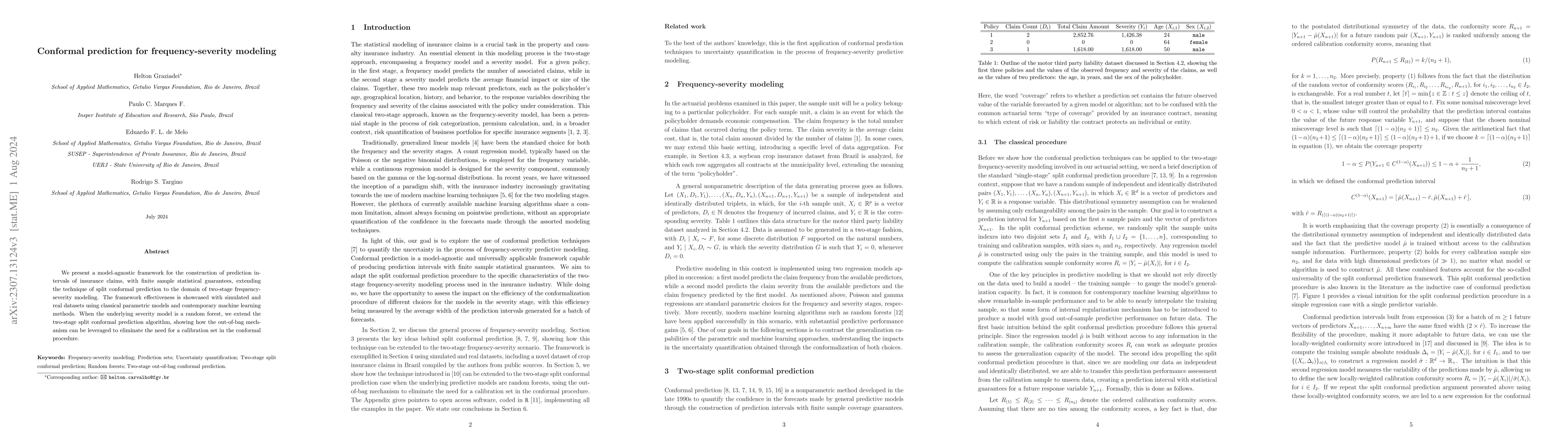

We present a nonparametric model-agnostic framework for building prediction intervals of insurance claims, with finite sample statistical guarantees, extending the technique of split conformal predi...

We define and develop an approach for risk budgeting allocation -- a risk diversification portfolio strategy -- where risk is measured using a dynamic time-consistent risk measure. For this, we intr...

Risk budgeting is a portfolio strategy where each asset contributes a prespecified amount to the aggregate risk of the portfolio. In this work, we propose an efficient numerical framework that uses ...

This paper is concerned with the process of risk allocation for a generic multivariate model when the risk measure is chosen as the Value-at-Risk (VaR). We recast the traditional Euler contributions...

We propose a stochastic model for claims reserving that captures dependence along development years within a single triangle. This dependence is of autoregressive form of order $p$ and is achieved t...

The methodology for measuring financial assets in defined contribution (DC) pension plans has significant implications whether wealth transfers will occur among participants. In December 2024, a regul...

Recently, there has been a growing interest in generative models based on diffusions driven by the empirical robustness of these methods in generating high-dimensional photorealistic images and the po...

Pension fund populations often have mortality experiences that are substantially different from the national benchmark. In a motivating case study of Brazilian corporate pension funds, pensioners are ...

Prediction of outstanding claims has been done via nonparametric models (chain ladder), semiparametric models (overdispersed poisson) or fully parametric models. In this paper, we propose models based...

This paper introduces a novel perspective on the use of reverse diffusion processes for sampling from unnormalized densities. The central idea is to embed the target density as the marginal at the ini...