Academic Profile

Statistics

Similar Authors

Papers on arXiv

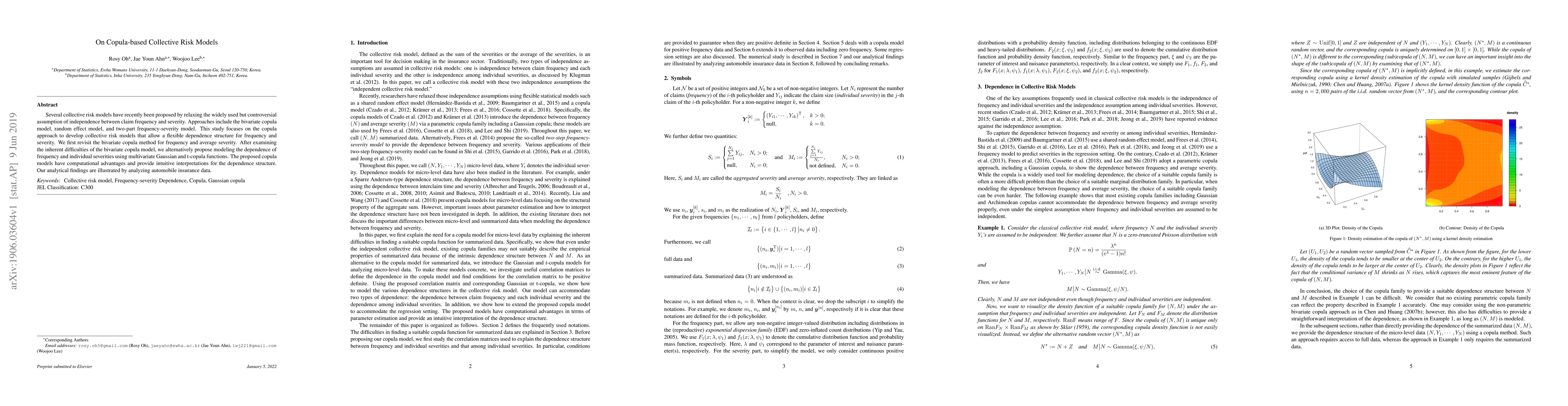

Copulas allow a flexible and simultaneous modeling of complicated dependence structures together with various marginal distributions. Especially if the density function can be represented as the pro...

As corporates and governments become more digital, they become vulnerable to various forms of cyber attack. Cyber insurance products have been used as risk management tools, yet their pricing does n...

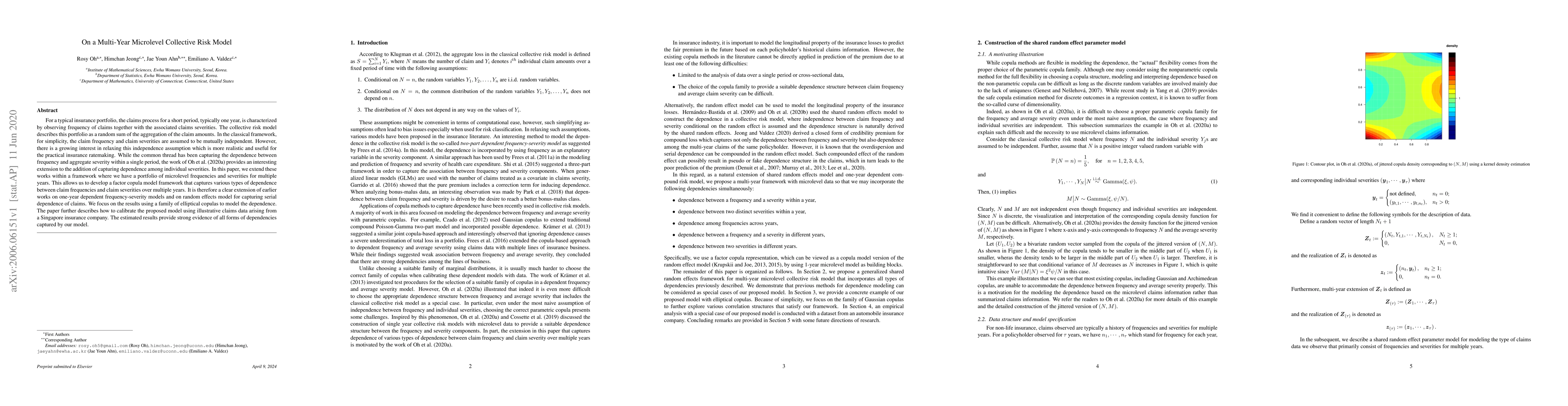

For a typical insurance portfolio, the claims process for a short period, typically one year, is characterized by observing frequency of claims together with the associated claims severities. The co...

In auto insurance, a Bonus-Malus System (BMS) is commonly used as a posteriori risk classification mechanism to set the premium for the next contract period based on a policyholder's claim history. ...

Typical risk classification procedure in insurance is consists of a priori risk classification determined by observable risk characteristics, and a posteriori risk classification where the premium i...

The bonus-malus system (BMS) is a widely used premium adjustment mechanism based on policyholder's claim history. Most auto insurance BMSs assume that policyholders in the same bonus-malus (BM) leve...

Several collective risk models have recently been proposed by relaxing the widely used but controversial assumption of independence between claim frequency and severity. Approaches include the bivar...