Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we introduce various machine learning solvers for (coupled) forward-backward systems of stochastic differential equations (FBSDEs) driven by a Brownian motion and a Poisson random mea...

We develop a model for the long-term dynamics of electricity market, based on mean-field games of optimal stopping. Our paper extends the recent contribution [A\"id, Ren\'e, Roxana Dumitrescu, and P...

We study the impact of transition scenario uncertainty, namely that of future carbon price and electricity demand, on the pace of decarbonization of the electricity industry. To this end, we develop...

In this paper, we consider the problem of a Principal aiming at designing a reward function for a population of heterogeneous agents. We construct an incentive based on the ranking of the agents, so...

We develop the fictitious play algorithm in the context of the linear programming approach for mean field games of optimal stopping and mean field games with regular control and absorption. This alg...

We introduce a zero-sum game problem of mean-field type as an extension of the classical zero-sum Dynkin game problem to the case where the payoff processes might depend on the value of the game and...

In this article, we establish a propagation of chaos result for weakly interacting nonlinear Snell envelopes which converge to a class of mean-field reflected backward stochastic differential equati...

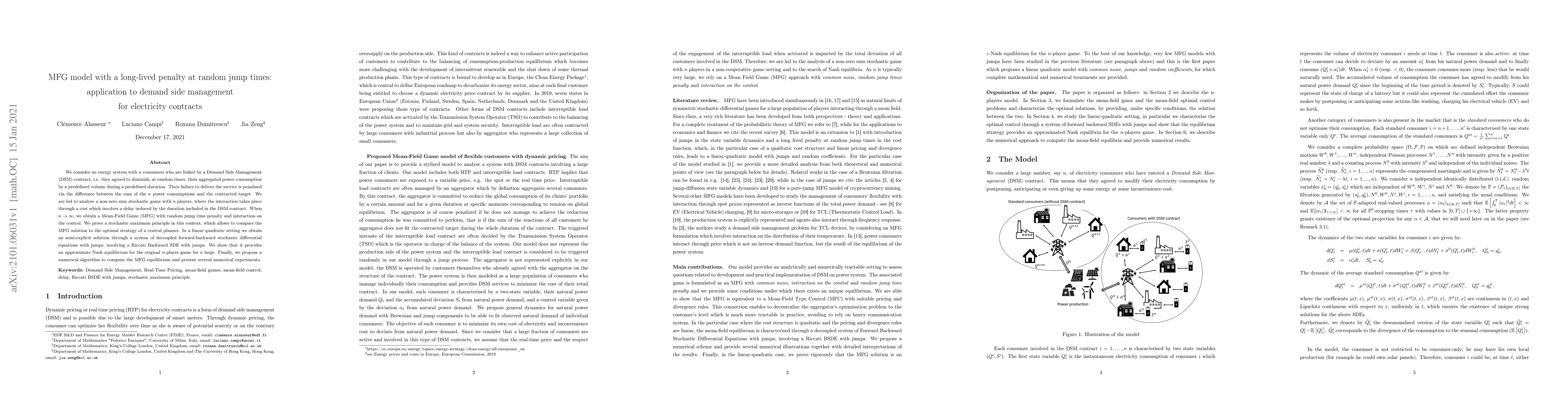

We consider an energy system with $n$ consumers who are linked by a Demand Side Management (DSM) contract, i.e. they agreed to diminish, at random times, their aggregated power consumption by a pred...

We develop the linear programming approach to mean-field games in a general setting. This relaxed control approach allows to prove existence results under weak assumptions, and lends itself well to ...

We develop a model for the industry dynamics in the electricity market, based on mean-field games of optimal stopping. In our model, there are two types of agents: the renewable producers and the co...

We consider the mean-field game where each agent determines the optimal time to exit the game by solving an optimal stopping problem with reward function depending on the density of the state proces...

We study the price impact of storage facilities in electricity markets and analyze the long-term profitability of these facilities in prospective scenarios of energy transition. To this end, we begin ...

We study mean-field games of optimal stopping (OS-MFGs) and introduce an entropy-regularized framework to enable learning-based solution methods. By utilizing randomized stopping times, we reformulate...

This article constructs a forward exponential utility in a market with multiple defaultable risks. Using the Jacod-Pham decomposition for random fields, we first characterize forward performance proce...

We provide a new characterization of law-invariant BSDEs with quadratic growth. This answers the open question raised in Xu-Xu-Zhou (2022) [44] on necessary conditions for law-invariance of g-expectat...