Academic Profile

Statistics

Similar Authors

Papers on arXiv

Methods for estimating heterogeneous treatment effects (HTE) from observational data have largely focused on continuous or binary outcomes, with less attention paid to survival outcomes and almost n...

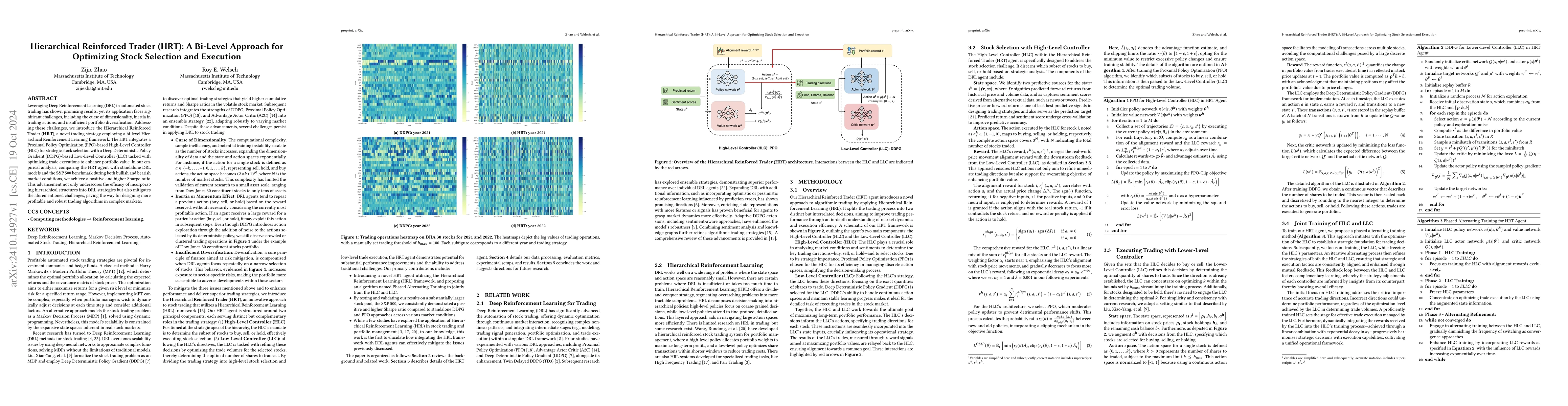

Leveraging Deep Reinforcement Learning (DRL) in automated stock trading has shown promising results, yet its application faces significant challenges, including the curse of dimensionality, inertia in...

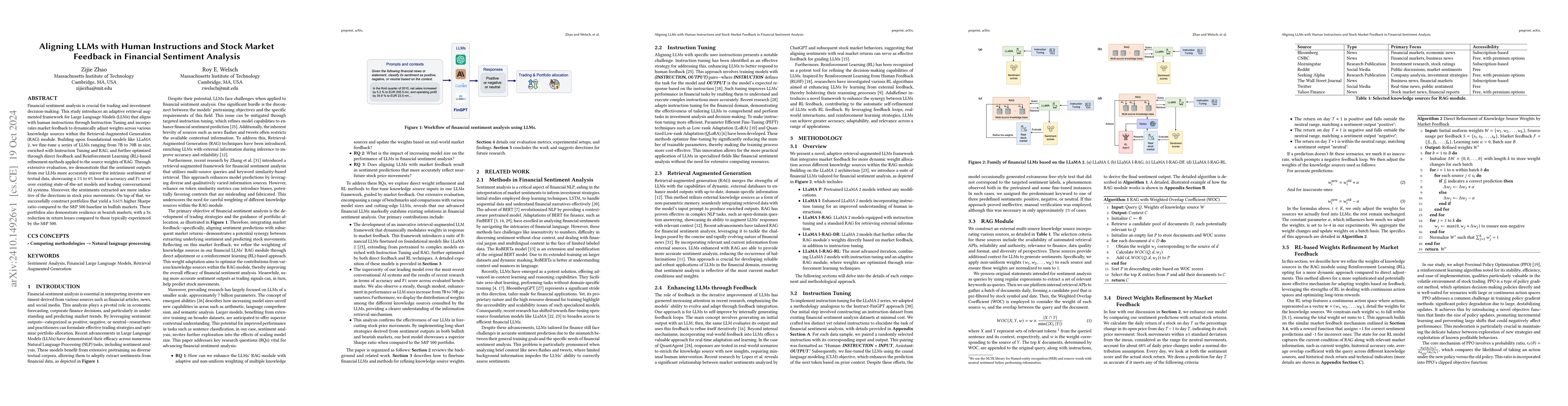

Financial sentiment analysis is crucial for trading and investment decision-making. This study introduces an adaptive retrieval augmented framework for Large Language Models (LLMs) that aligns with hu...

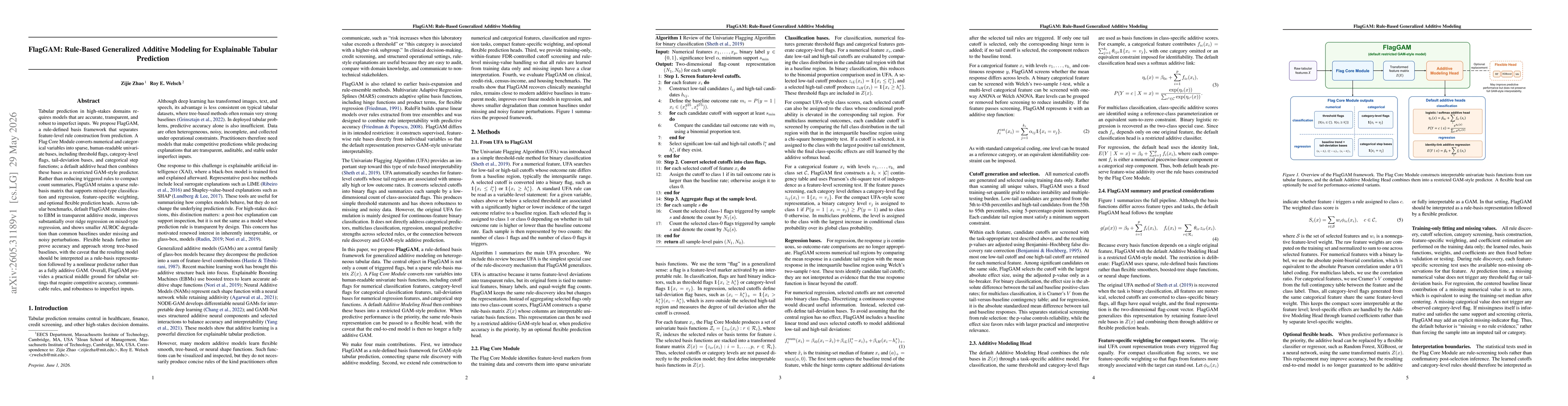

Tabular prediction in high-stakes domains requires models that are accurate, transparent, and robust to imperfect inputs. We propose FlagGAM, a rule-defined basis framework that separates feature-leve...

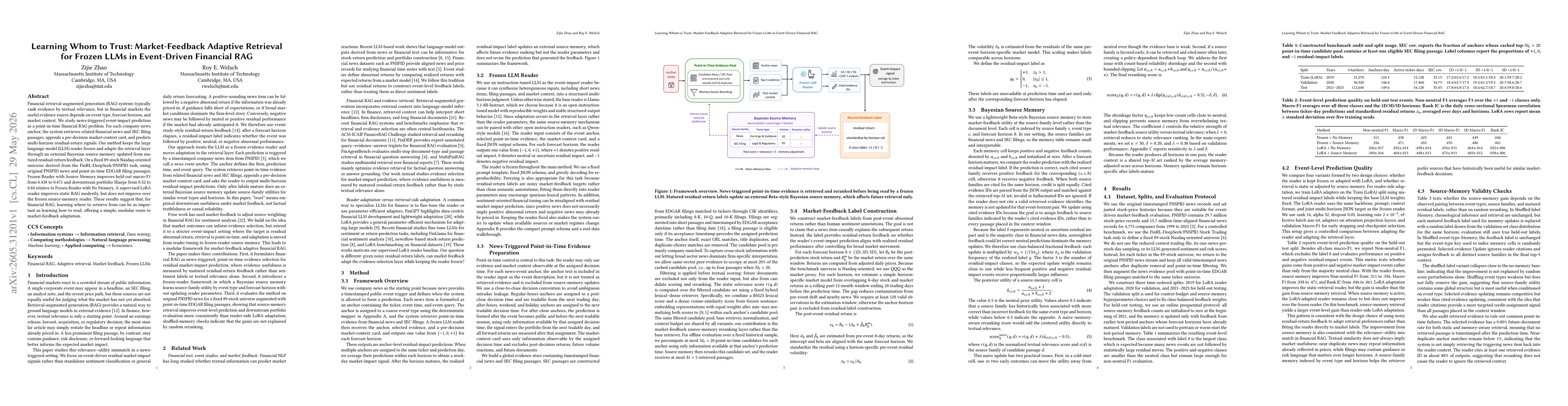

Financial retrieval-augmented generation (RAG) systems typically rank evidence by textual relevance, but in financial markets the useful evidence source depends on event type, forecast horizon, and ma...