Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study risk-sensitive multi-agent reinforcement learning under general-sum Markov games, where agents optimize the entropic risk measure of rewards with possibly diverse risk preferences. We show ...

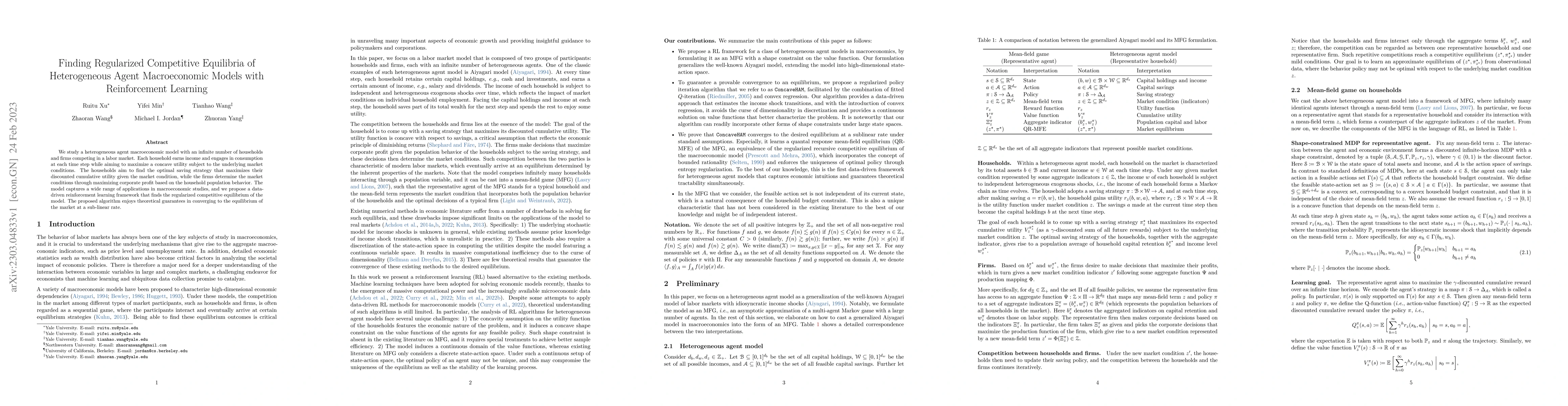

We study a heterogeneous agent macroeconomic model with an infinite number of households and firms competing in a labor market. Each household earns income and engages in consumption at each time st...

We study a Markov matching market involving a planner and a set of strategic agents on the two sides of the market. At each step, the agents are presented with a dynamical context, where the context...

In this paper, we study gap-dependent regret guarantees for risk-sensitive reinforcement learning based on the entropic risk measure. We propose a novel definition of sub-optimality gaps, which we c...

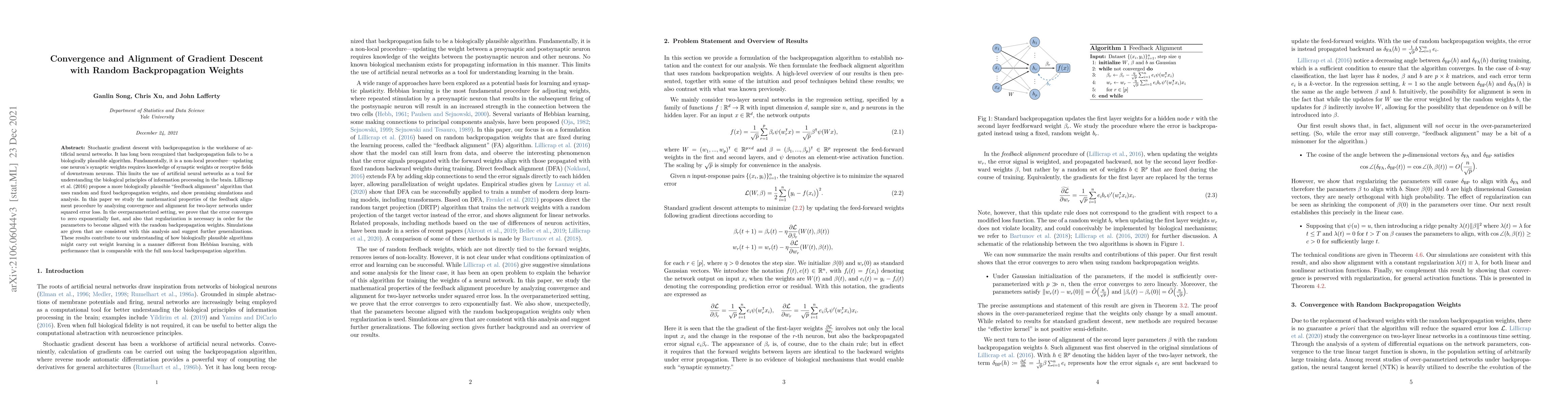

Stochastic gradient descent with backpropagation is the workhorse of artificial neural networks. It has long been recognized that backpropagation fails to be a biologically plausible algorithm. Fund...

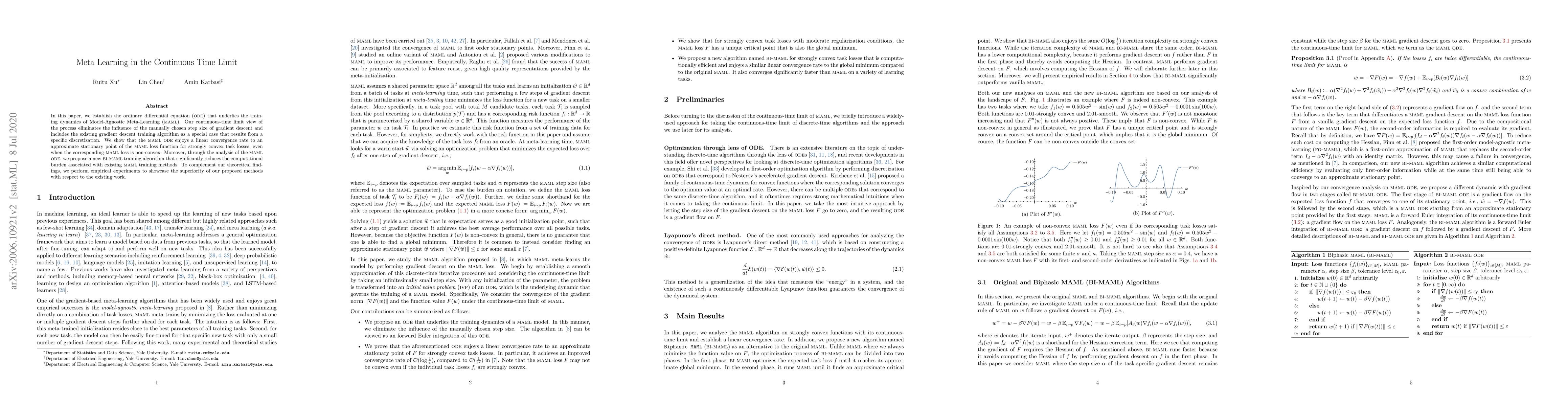

In this paper, we establish the ordinary differential equation (ODE) that underlies the training dynamics of Model-Agnostic Meta-Learning (MAML). Our continuous-time limit view of the process elimin...