Academic Profile

Statistics

Similar Authors

Papers on arXiv

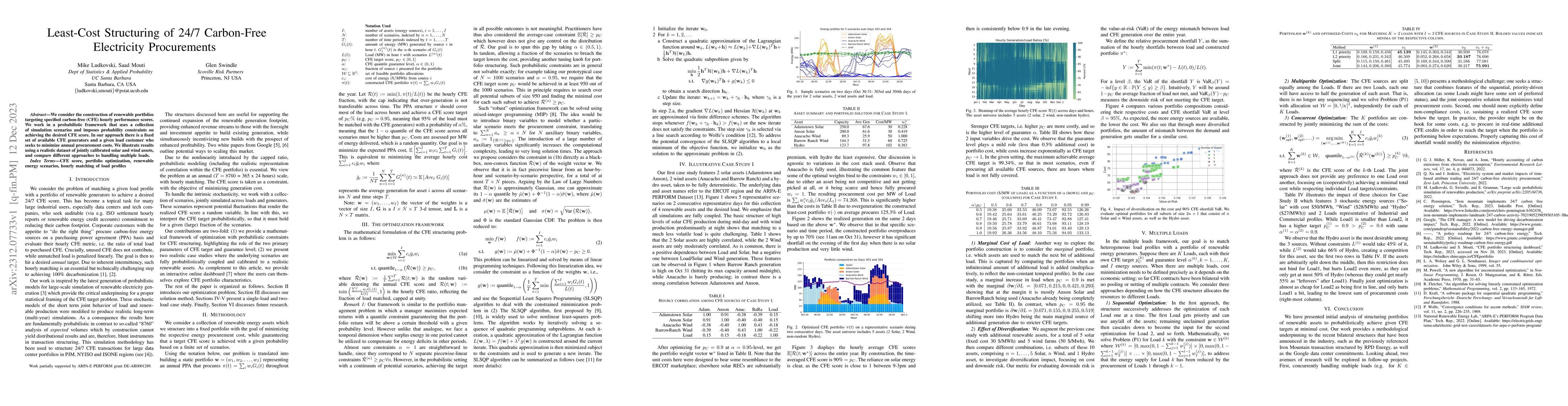

We consider the construction of renewable portfolios targeting specified carbon-free (CFE) hourly performance scores. We work in a probabilistic framework that uses a collection of simulation scenar...

In Gatheral et al. 2018, first posted in 2014, volatility is characterized by fractional behavior with a Hurst exponent $H < 0.5$, challenging traditional views of volatility dynamics. Gatheral et a...

Two-point time-series data, characterized by baseline and follow-up observations, are frequently encountered in health research. We study a novel two-point time series structure without a control gr...

We use supervised learning to identify factors that predict the cross-section of returns and maximum drawdown for stocks in the US equity market. Our data run from January 1970 to December 2019 and ...