Academic Profile

Statistics

Similar Authors

Papers on arXiv

Sparse high dimensional graphical model selection is a topic of much interest in modern day statistics. A popular approach is to apply l1-penalties to either (1) parametric likelihoods, or, (2) regu...

Sparse high dimensional graphical model selection is a popular topic in contemporary machine learning. To this end, various useful approaches have been proposed in the context of $\ell_1$-penalized ...

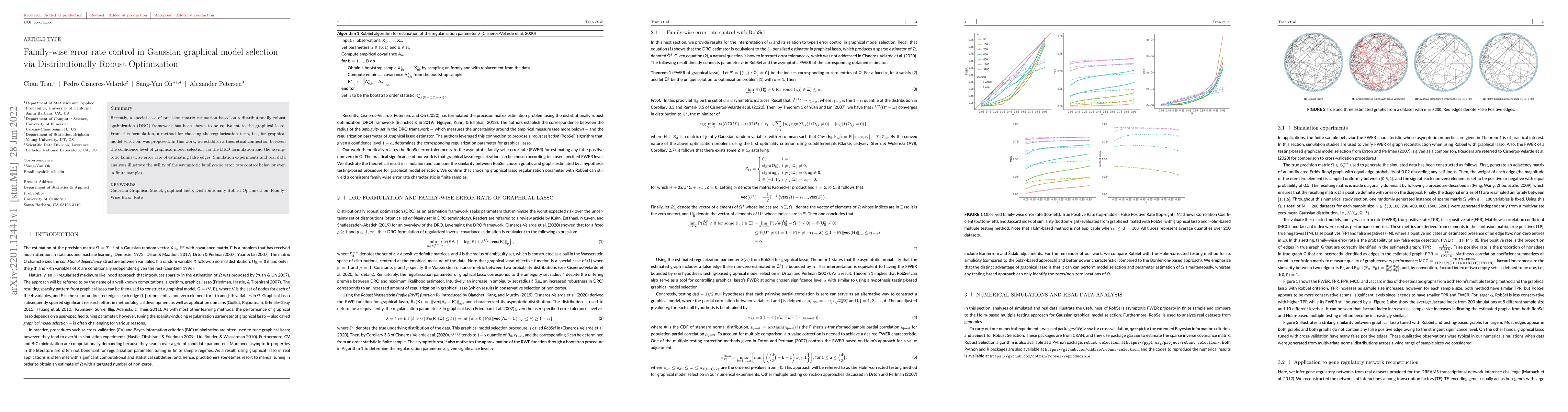

Recently, a special case of precision matrix estimation based on a distributionally robust optimization (DRO) framework has been shown to be equivalent to the graphical lasso. From this formulation,...

Gaussian Graphical models (GGM) are widely used to estimate the network structures in many applications ranging from biology to finance. In practice, data is often corrupted by latent confounders wh...

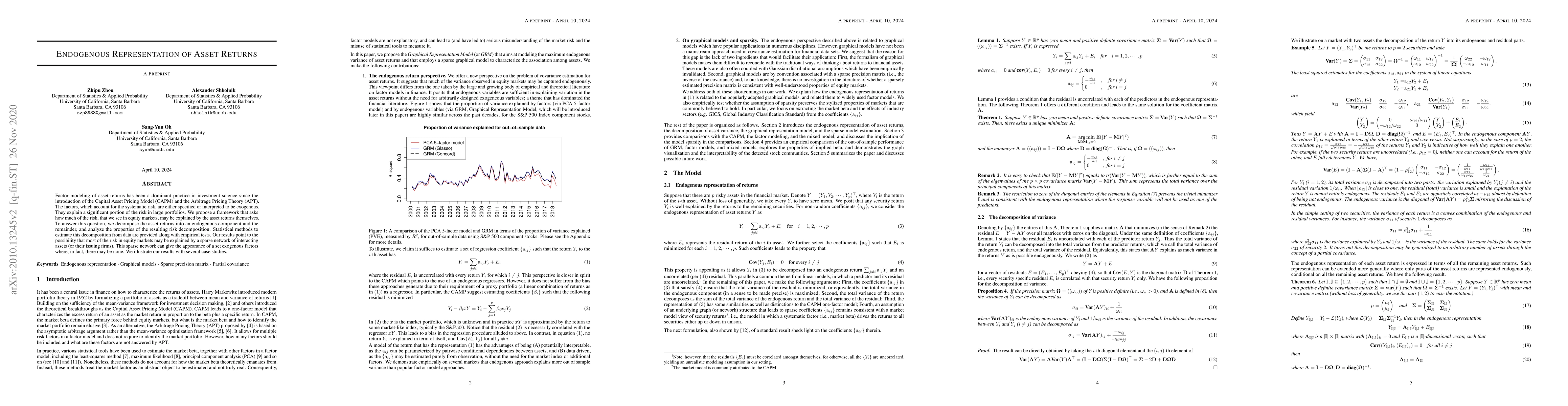

Factor modeling of asset returns has been a dominant practice in investment science since the introduction of the Capital Asset Pricing Model (CAPM) and the Arbitrage Pricing Theory (APT). The facto...

The covariance structure of multivariate functional data can be highly complex, especially if the multivariate dimension is large, making extensions of statistical methods for standard multivariate ...

Across a variety of scientific disciplines, sparse inverse covariance estimation is a popular tool for capturing the underlying dependency relationships in multivariate data. Unfortunately, most est...

Graphical model estimation from modern multi-omics data requires a balance between statistical estimation performance and computational scalability. We introduce a novel pseudolikelihood-based graphic...

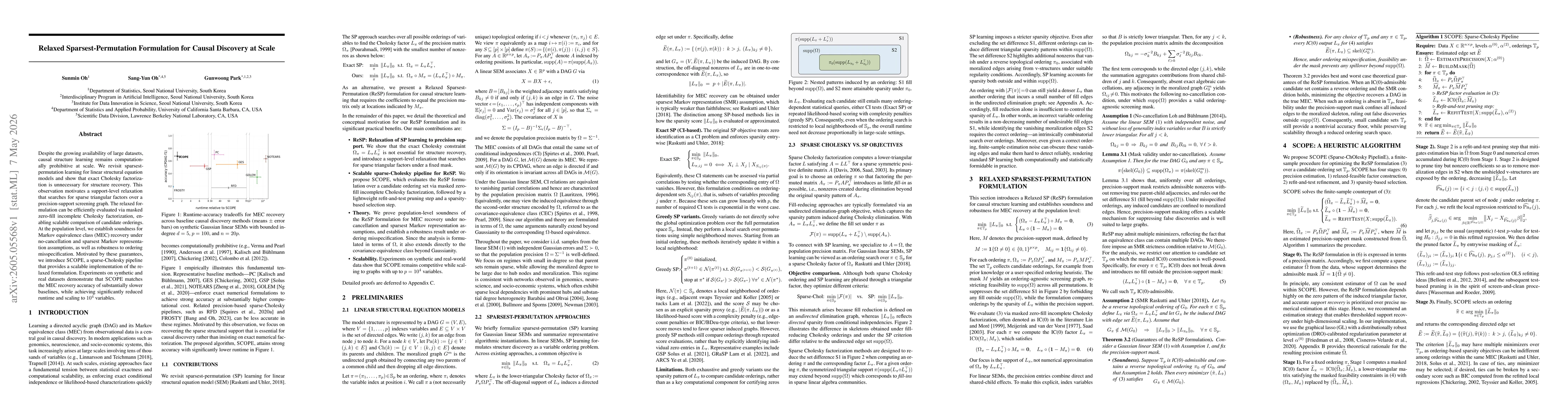

Despite the growing availability of large datasets, causal structure learning remains computationally prohibitive at scale. We revisit sparsest-permutation learning for linear structural equation mode...