Academic Profile

Statistics

Similar Authors

Papers on arXiv

Geometric Asian options are a type of options where the payoff depends on the geometric mean of the underlying asset over a certain period of time. This paper is concerned with the pricing of such o...

We study and solve the worst-case optimal portfolio problem as pioneered by Korn and Wilmott (2002) of an investor with logarithmic preferences facing the possibility of a market crash with stochast...

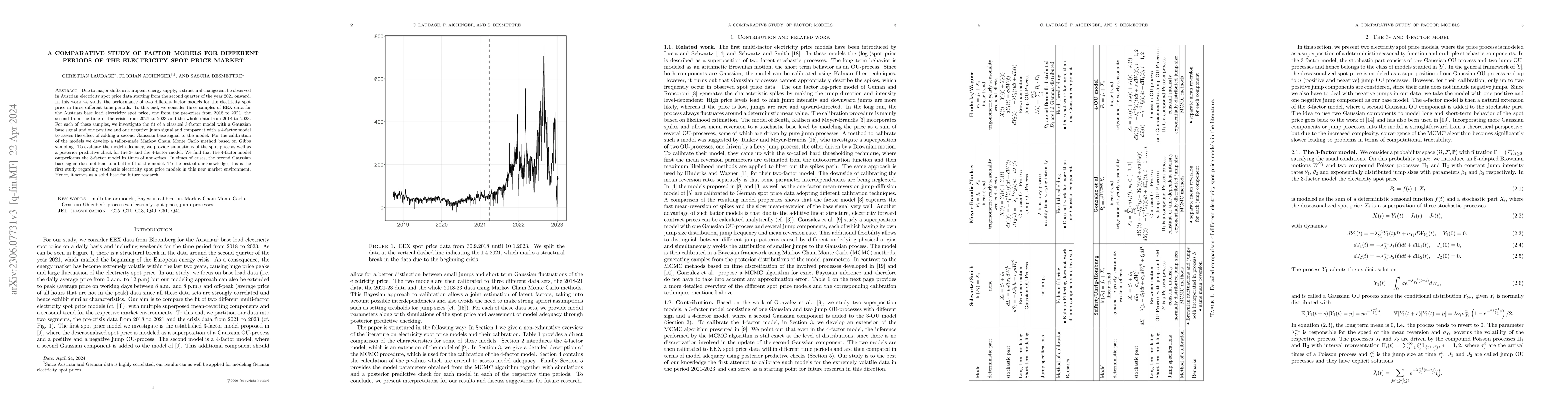

Due to major shifts in European energy supply, a structural change can be observed in Austrian electricity spot price data starting from the second quarter of the year 2021 onward. In this work we s...

In this working paper we present our current progress in the training of machine learning models to execute short option strategies on the S&P500. As a first step, this paper is breaking this proble...

This paper is concerned with portfolio selection for an investor with power utility in multi-asset financial markets in a rough stochastic environment. We investigate Merton's portfolio problem for ...

We introduce a mean-field extension of the LIBOR market model (LMM) which preserves the basic features of the original model. Among others, these features are the martingale property, a directly imp...

It is generally understood that a given one-dimensional diffusion may be transformed by Cameron-Martin-Girsanov measure change into another one-dimensional diffusion with the same volatility but a d...

In this paper we investigate the representation of a class of non Gaussian processes, namely generalized grey Brownian motion, in terms of a weighted integral of a stochastic process which is a solu...

When dealing with Heston's stochastic volatility model, the change of measure from the subjective measure P to the objective measure Q is usually investigated under the assumption that the Feller co...

This paper presents a novel approach to pricing American options using piecewise diffusion Markov processes (PDifMPs), a type of generalised stochastic hybrid system that integrates continuous dynamic...

In intertemporal settings, the multiattribute utility theory of Kihlstrom and Mirman suggests the application of a concave transform of the lifetime utility index. This construction, while allowing ti...

The first-passage time (FPT) is a fundamental concept in stochastic processes, representing the time it takes for a process to reach a specified threshold for the first time. Often, considering a time...

Piecewise Diffusion Markov Processes (PDifMPs) are valuable for modelling systems where continuous dynamics are interrupted by sudden shifts and/or changes in drift and diffusion. The first-passage ti...

The first-passage time is a key concept in stochastic modeling, representing the time at which a process first reaches a specified threshold. In this work, we consider a jump-diffusion (JD) model with...

Piecewise diffusion Markov processes (PDifMPs) form a versatile class of stochastic hybrid systems that combine continuous diffusion processes with discrete event-driven dynamics, enabling flexible mo...

We study a continuous-time portfolio choice problem for an investor whose state-dependent preferences are determined by an exogenous factor that evolves as an Itô diffusion process. Since risk attitud...