Academic Profile

Statistics

Similar Authors

Papers on arXiv

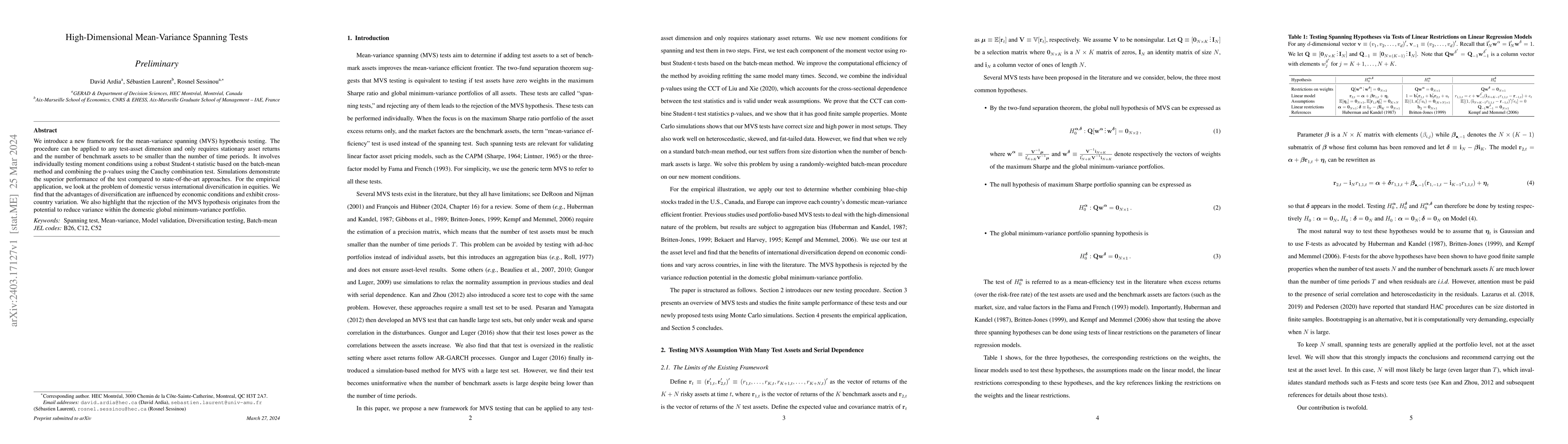

We introduce a new framework for the mean-variance spanning (MVS) hypothesis testing. The procedure can be applied to any test-asset dimension and only requires stationary asset returns and the numb...

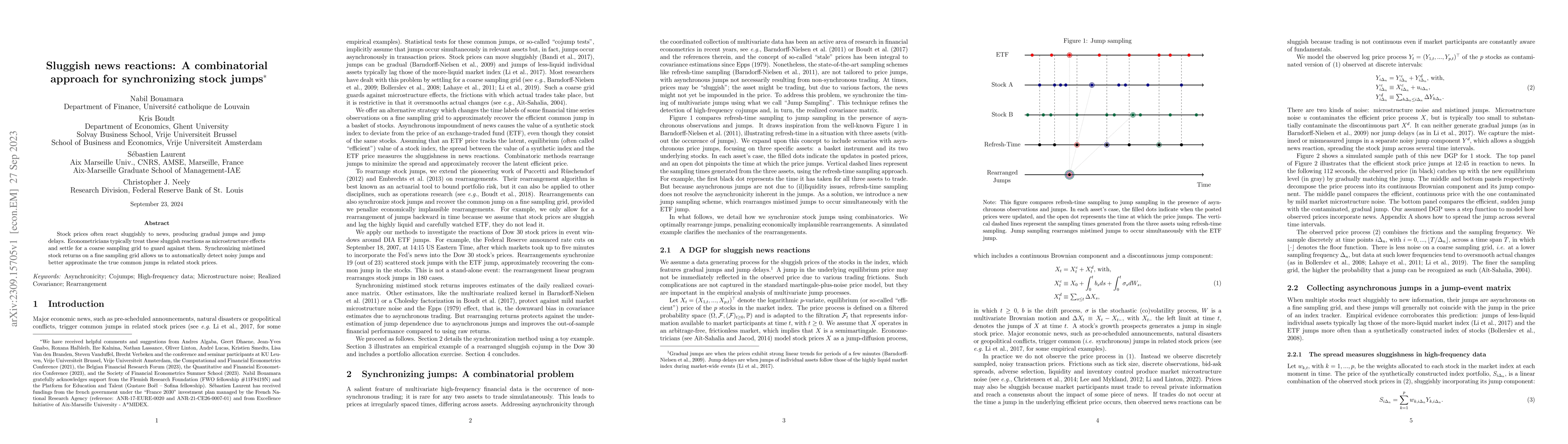

Stock prices often react sluggishly to news, producing gradual jumps and jump delays. Econometricians typically treat these sluggish reactions as microstructure effects and settle for a coarse sampl...

We introduce a simple tool to control for false discoveries and identify individual signals in scenarios involving many tests, dependent test statistics, and potentially sparse signals. The tool app...

Despite their high predictive performance, random forest and gradient boosting are often considered as black boxes or uninterpretable models which has raised concerns from practitioners and regulato...

Post-Double-Lasso is becoming the most popular method for estimating linear regression models with many covariates when the purpose is to obtain an accurate estimate of a parameter of interest, such a...