Academic Profile

Statistics

Similar Authors

Papers on arXiv

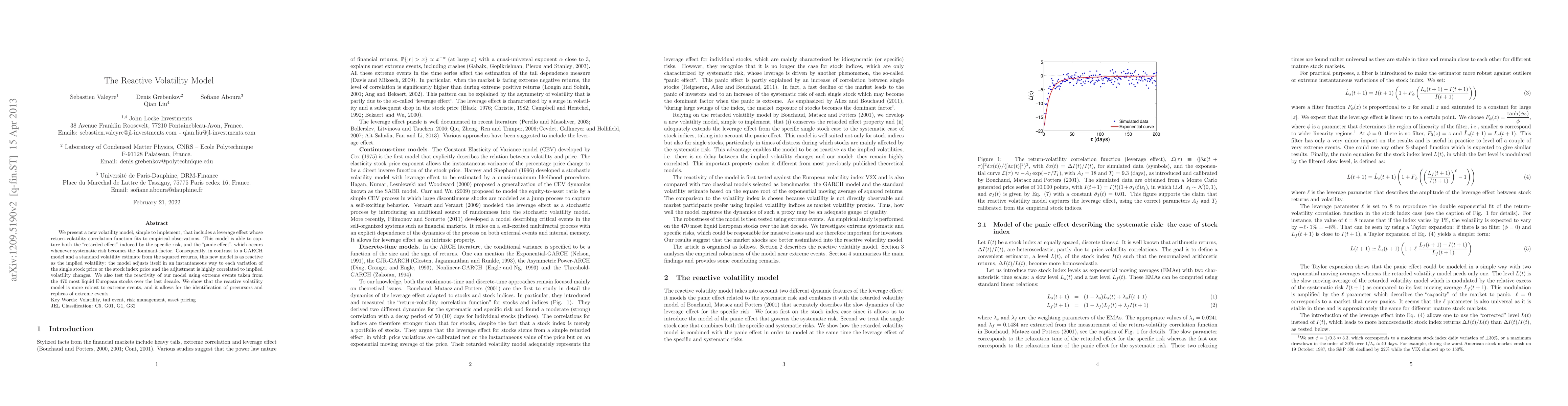

We present a new volatility model, simple to implement, that includes a leverage effect whose return-volatility correlation function fits to empirical observations. This model is able to capture bot...

This paper derives an optimal portfolio that is based on trend-following signal. Building on an earlier related article, it provides a unifying theoretical setting to introduce an autocorrelation mo...

A new methodology has been introduced to clean the correlation matrix of single stocks returns based on a constrained principal component analysis using financial data. Portfolios were introduced, n...

We present a reactive beta model that includes the leverage effect to allow hedge fund managers to target a near-zero beta for market neutral strategies. For this purpose, we derive a metric of corr...

Recently, LLMs (Large Language Models) have been adapted for time series prediction with significant success in pattern recognition. However, the common belief is that these models are not suitable fo...

Our empirical results, illustrated in Fig.5, show an impressive fit with the pretty complex theoritical Sharpe formula of a Trend following strategy depending on the parameter of the signal, which was...