Academic Profile

Statistics

Similar Authors

Papers on arXiv

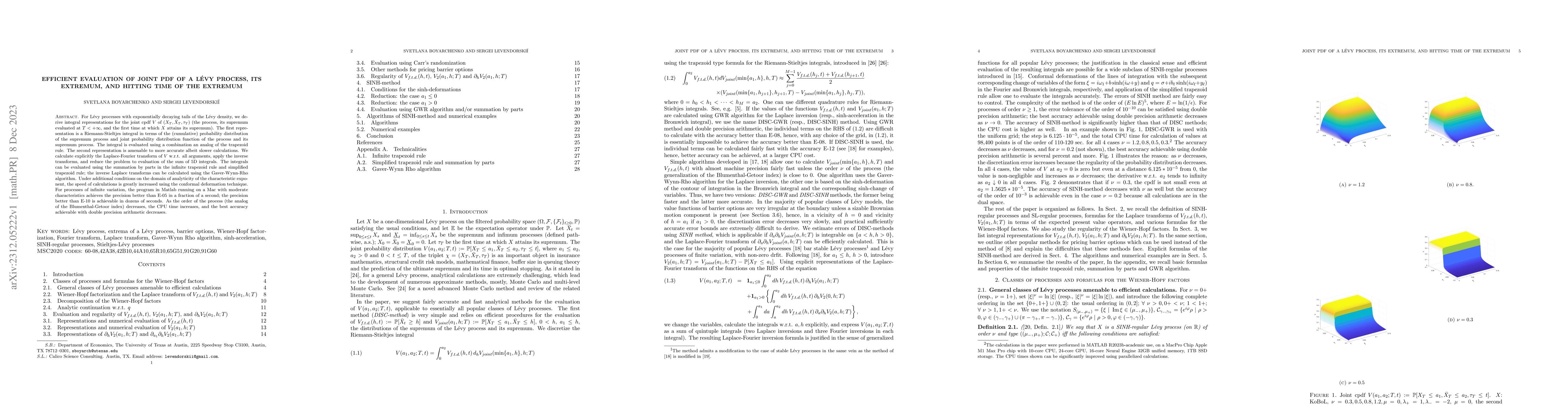

For L\'evy processes with exponentially decaying tails of the L\'evy density, we derive integral representations for the joint cpdf $V$ of $(X_T, \bar X_T,\tau_T)$ (the process, its supremum evaluat...

We suggest a general framework for simulation of the triplet $(X_T,\bar X_ T,\tau_T)$ (L\'evy process, its extremum, and hitting time of the extremum), and, separately, $X_T,\bar X_ T$ and pairs $(X...

We analyze the qualitative differences between prices of double barrier no-touch options in the Heston model and pure jump KoBoL model calibrated to the same set of the empirical data, and discuss t...