Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper provides a Feller's test for explosions of one-dimensional continuous stochastic Volterra processes of convolution type. The study focuses on dynamics governed by nonsingular kernels, whi...

We study the class of continuous polynomial Volterra processes, which we define as solutions to stochastic Volterra equations driven by a continuous semimartingale with affine drift and quadratic di...

We study an extension of the Heston stochastic volatility model that incorporates rough volatility and jump clustering phenomena. In our model, named the rough Hawkes Heston stochastic volatility mo...

We provide sufficient conditions that guarantee the existence of relaxed optimal controls in the weak formulation of stochastic control problems for stochastic Volterra equations (SVEs). Our study c...

The theory of affine processes has been recently extended to the framework of stochastic Volterra equations with continuous trajectories. These so-called affine Volterra processes overcome modeling ...

We price American options using kernel-based approximations of the Volterra Heston model. We choose these approximations because they allow simulation-based techniques for pricing. We prove the conv...

We obtain general weak existence and stability results for stochastic convolution equations with jumps under mild regularity assumptions, allowing for non-Lipschitz coefficients and singular kernels...

We introduce affine Volterra processes, defined as solutions of certain stochastic convolution equations with affine coefficients. Classical affine diffusions constitute a special case, but affine V...

We study discretizations of polynomial processes using finite state Markov processes satisfying suitable moment matching conditions. The states of these Markov processes together with their transiti...

This study presents a quantitative framework to compare teams in collective sports with respect to their style of play. The style of play is characterized by the team's spatial distribution over a col...

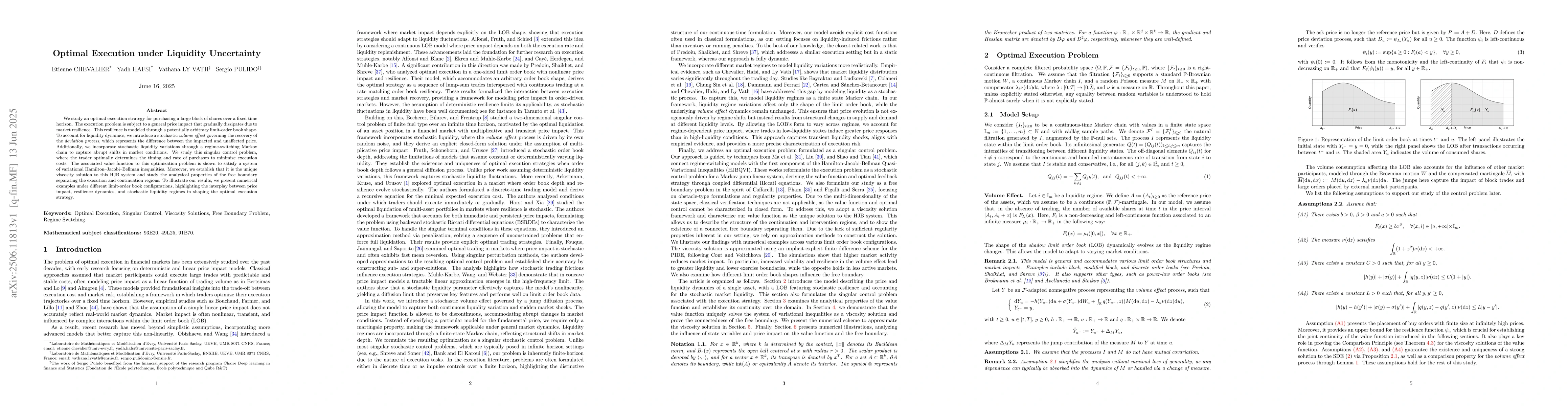

We study an optimal execution strategy for purchasing a large block of shares over a fixed time horizon. The execution problem is subject to a general price impact that gradually dissipates due to mar...