Academic Profile

Statistics

Similar Authors

Papers on arXiv

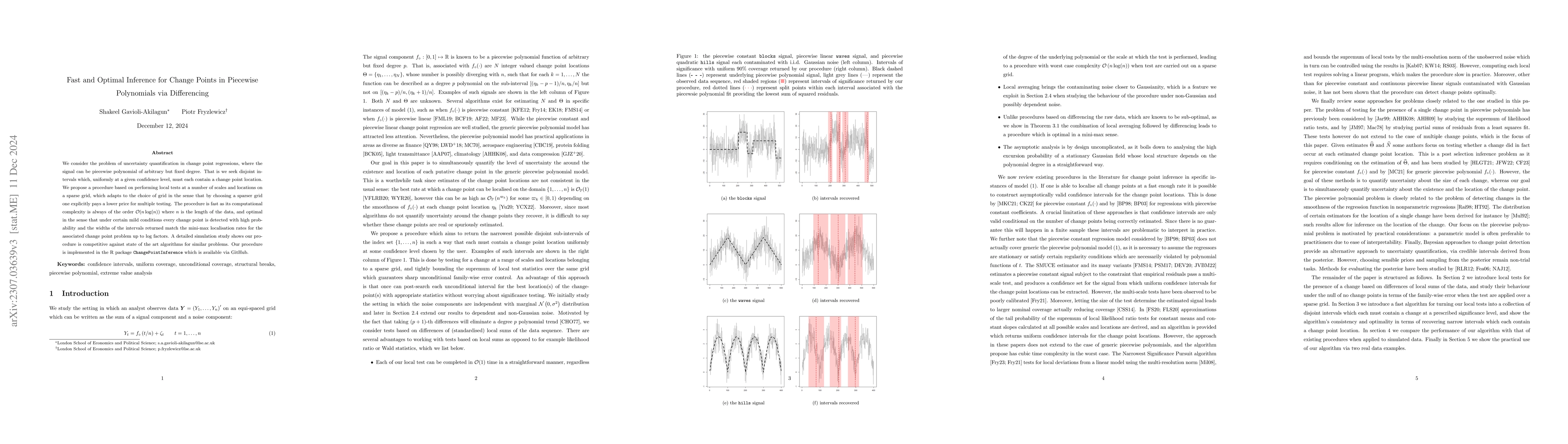

We consider the problem of uncertainty quantification in change point regressions, where the signal can be piecewise polynomial of arbitrary but fixed degree. That is we seek disjoint intervals whic...

This article studies the problem of online non-parametric change point detection in multivariate data streams. We approach the problem through the lens of kernel-based two-sample testing and introduce...

We introduce kernel integrated $R^2$, a new measure of statistical dependence that combines the local normalization principle of the recently introduced integrated $R^2$ with the flexibility of reprod...

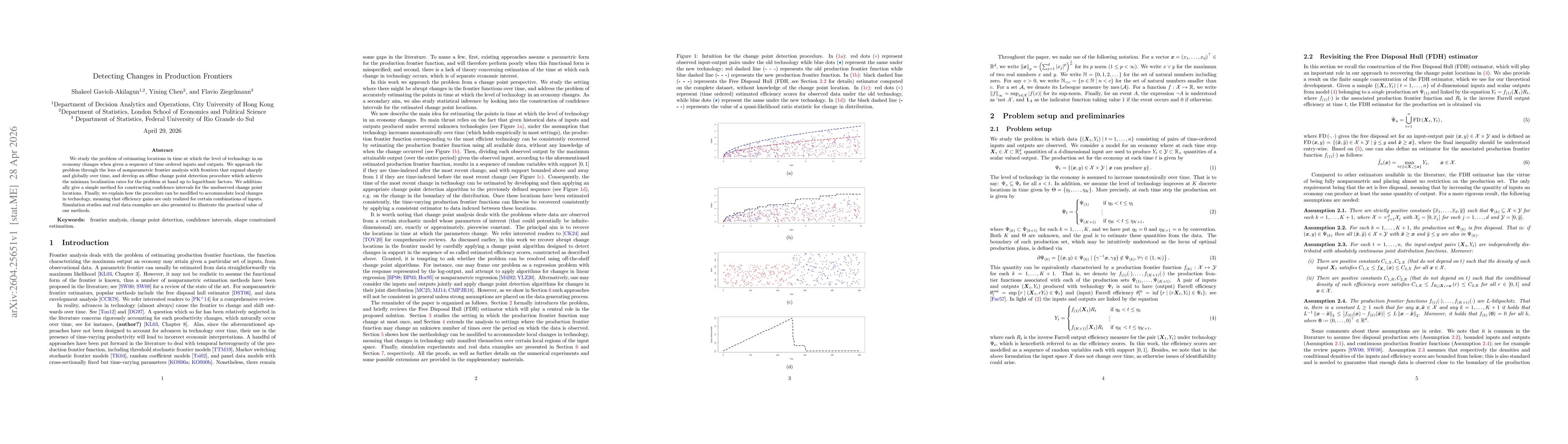

We study the problem of estimating locations in time at which the level of technology in an economy changes when given a sequence of time ordered inputs and outputs. We approach the problem through th...

We propose a framework for determining whether the causal dependence of an outcome $Y$ on a covariate $X$ changes at a given time point, given confounders $\boldsymbol{Z}$. For instance, in financial ...