Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, to address the optimization problem on a compact matrix manifold, we introduce a novel algorithmic framework called the Transformed Gradient Projection (TGP) algorithm, using the proj...

We investigate how to solve smooth matrix optimization problems with general linear inequality constraints on the eigenvalues of a symmetric matrix. We present solution methods to obtain exact globa...

In this paper we consider a non-monotone (mixed) variational inequality model with (nonlinear) convex conic constraints. Through developing an equivalent Lagrangian function-like primal-dual saddle-...

In this paper, we discuss variational inequality (VI) problems without monotonicity from the perspective of convergence of projection-type algorithms. In particular, we identify existing conditions ...

In this paper, we develop stochastic variance reduced algorithms for solving a class of finite-sum monotone VI, where the operator consists of the sum of finitely many monotone VI mappings and the s...

In this paper, we propose a general extra-gradient scheme for solving monotone variational inequalities (VI), referred to here as Approximation-based Regularized Extra-gradient method (ARE). The fir...

Matrix functions are utilized to rewrite smooth spectral constrained matrix optimization problems as smooth unconstrained problems over the set of symmetric matrices which are then solved via the cu...

A popular approach to minimize a finite-sum of convex functions is stochastic gradient descent (SGD) and its variants. Fundamental research questions associated with SGD include: (i) To find a lower...

Characterizing simultaneously diagonalizable (SD) matrices has been receiving considerable attention in the recent decades due to its wide applications and its role in matrix analysis. However, the ...

In this work we study a special minimax problem where there are linear constraints that couple both the minimization and maximization decision variables. The problem is a generalization of the tradi...

We consider the convex-concave saddle point problem $\min_{\mathbf{x}}\max_{\mathbf{y}}\Phi(\mathbf{x},\mathbf{y})$, where the decision variables $\mathbf{x}$ and/or $\mathbf{y}$ subject to a multi-...

In this paper, we propose two new solution schemes to solve the stochastic strongly monotone variational inequality problems: the stochastic extra-point solution scheme and the stochastic extra-mome...

Many large-scale optimization problems can be expressed as composite optimization models. Accelerated first-order methods such as the fast iterative shrinkage-thresholding algorithm (FISTA) have pro...

In this paper, we propose a unifying framework incorporating several momentum-related search directions for solving strongly monotone variational inequalities. The specific combinations of the searc...

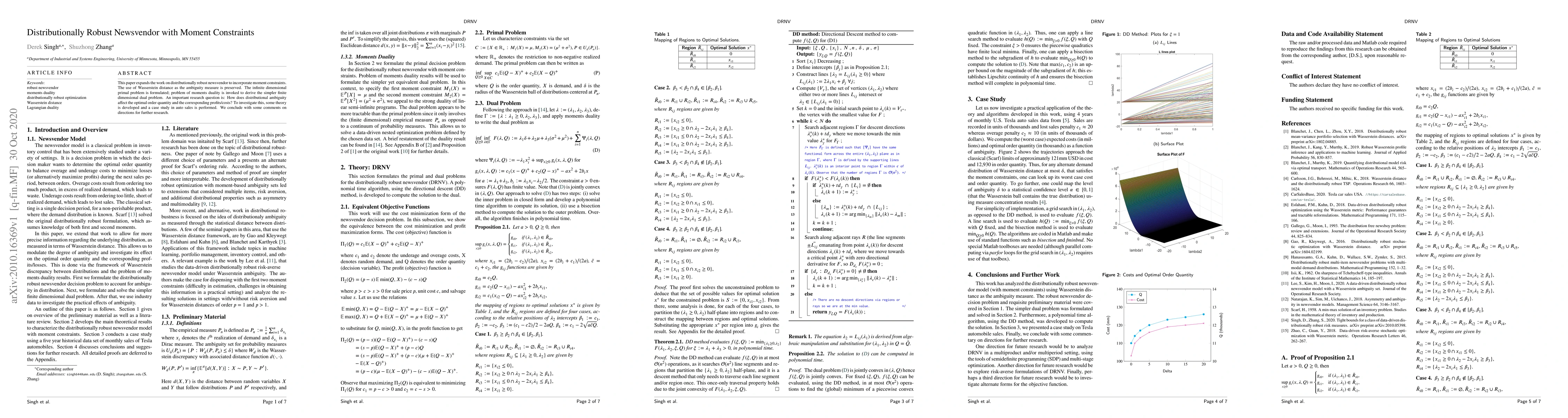

This paper expands the work on distributionally robust newsvendor to incorporate moment constraints. The use of Wasserstein distance as the ambiguity measure is preserved. The infinite dimensional p...

In this paper, we propose a cubic regularized Newton (CRN) method for solving convex-concave saddle point problems (SPP). At each iteration, a cubic regularized saddle point subproblem is constructe...

Nonlinearly constrained nonconvex and nonsmooth optimization models play an increasingly important role in machine learning, statistics and data analytics. In this paper, based on the augmented Lagr...

Random projection is often used to project higher-dimensional vectors onto a lower-dimensional space, while approximately preserving their pairwise distances. It has emerged as a powerful tool in va...

This paper expands the notion of robust profit opportunities in financial markets to incorporate distributional uncertainty using Wasserstein distance as the ambiguity measure. Financial markets wit...

This paper studies the generalization bounds for the empirical saddle point (ESP) solution to stochastic saddle point (SSP) problems. For SSP with Lipschitz continuous and strongly convex-strongly c...

This paper investigates arbitrage properties of financial markets under distributional uncertainty using Wasserstein distance as the ambiguity measure. The weak and strong forms of the classical arb...

In this paper, we study the lower iteration complexity bounds for finding the saddle point of a strongly convex and strongly concave saddle point problem: $\min_x\max_yF(x,y)$. We restrict the class...

This paper investigates calculations of robust funding valuation adjustment (FVA) for over the counter (OTC) derivatives under distributional uncertainty using Wasserstein distance as the ambiguity ...

This paper is concerned with finding an optimal algorithm for minimizing a composite convex objective function. The basic setting is that the objective is the sum of two convex functions: the first ...

We propose a new framework to implement interior point method (IPM) to solve very large linear programs (LP). Traditional IPMs typically use Newton's method to approximately solve a subproblem that ...

In this paper, we consider an unconstrained optimization model where the objective is a sum of a large number of possibly nonconvex functions, though overall the objective is assumed to be smooth an...

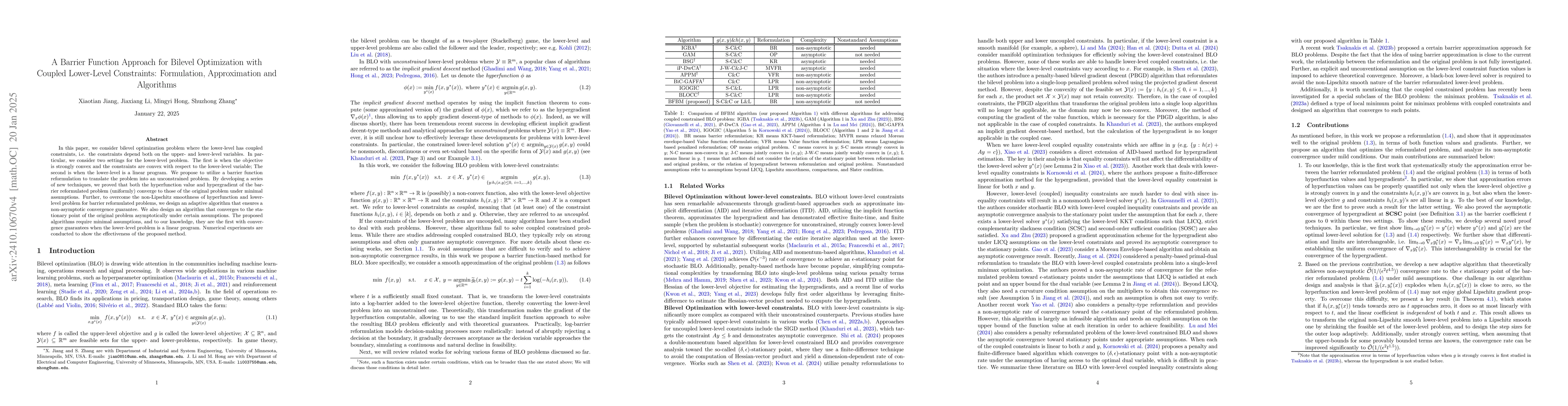

In this paper, we consider bilevel optimization problem where the lower-level has coupled constraints, i.e. the constraints depend both on the upper- and lower-level variables. In particular, we consi...

In this paper, we introduce a new optimization algorithm that is well suited for solving parameter estimation problems. We call our new method cubic regularized Newton with affine scaling (CRNAS). In ...

This paper presents and analyzes the first matrix optimization model which allows general coordinate and spectral constraints. The breadth of problems our model covers is exemplified by a lengthy list...

We introduce and study various algorithms for solving nonconvex minimization with inequality constraints, based on the construction of convex surrogate envelopes that majorize the objective and the co...

We study optimization over Riemannian embedded submanifolds, where the objective function is relatively smooth in the ambient Euclidean space. Such problems have broad applications but are still large...

This paper studies bandit convex optimization in non-stationary environments with two-point feedback, using dynamic regret as the performance measure. We propose an algorithm based on bandit mirror de...

We consider bilevel optimization problems with general nonconvex lower-level objectives and show that the classical hyperfunction-based formulation is unsettled, since the global minimizer of the lowe...

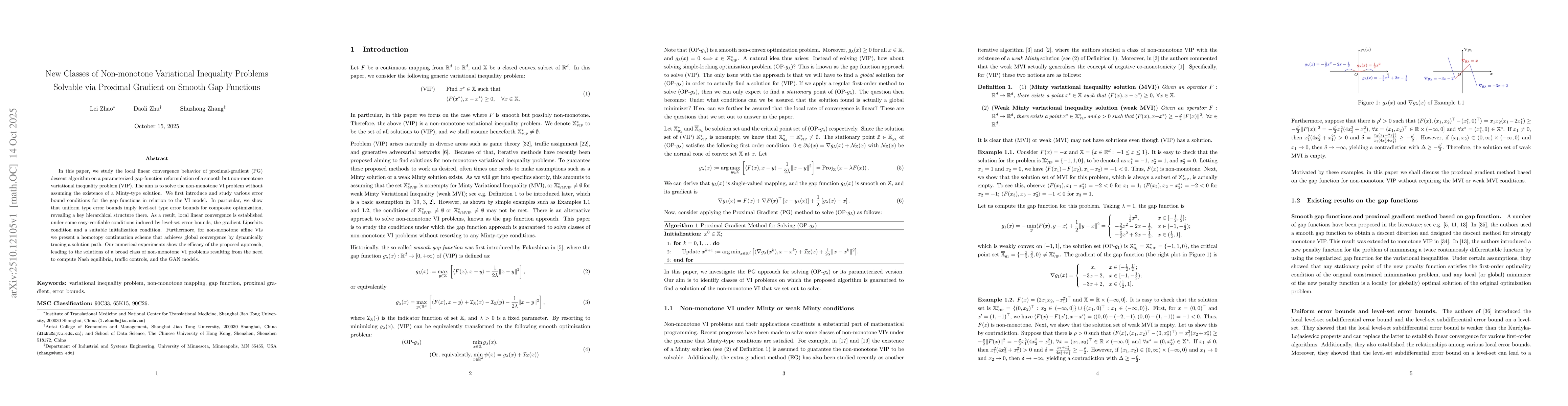

In this paper, we study the local linear convergence behavior of proximal-gradient (PG) descent algorithm on a parameterized gap-function reformulation of a smooth but non-monotone variational inequal...

In this paper, we develop a new adaptive regularization method for minimizing a composite function, which is the sum of a $p$th-order ($p \ge 1$) Lipschitz continuous function and a simple, convex, an...

In this paper, we revisit a classical adaptive stepsize strategy for gradient descent: the Polyak stepsize (\texttt{PolyakGD}), originally proposed in \cite{polyak1969minimization}. We study the conve...

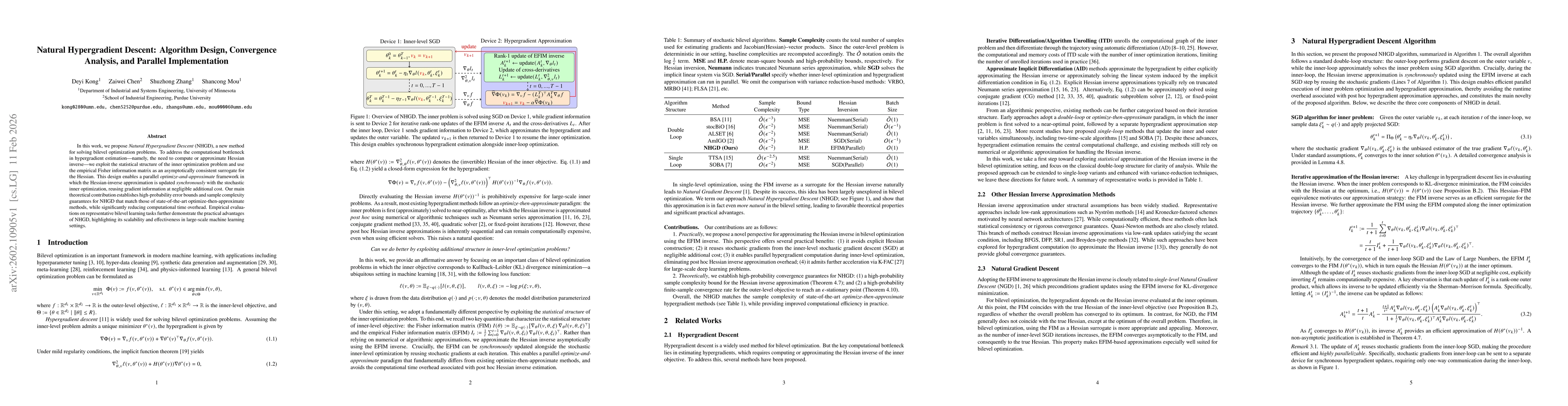

In this work, we propose Natural Hypergradient Descent (NHGD), a new method for solving bilevel optimization problems. To address the computational bottleneck in hypergradient estimation--namely, the ...

In this paper, we study the regularity assumptions commonly adopted in bilevel optimization with constrained lower-level problems, including the linear independence constraint qualification, the stric...

Bilevel optimization is an indispensable modeling tool for modern machine learning and engineering design. However, the theory and practice for finding second order stationary points in the context of...