Academic Profile

Statistics

Similar Authors

Papers on arXiv

Geographical and Temporal Weighted Regression (GTWR) model is an important local technique for exploring spatial heterogeneity in data relationships, as well as temporal dependence due to its high f...

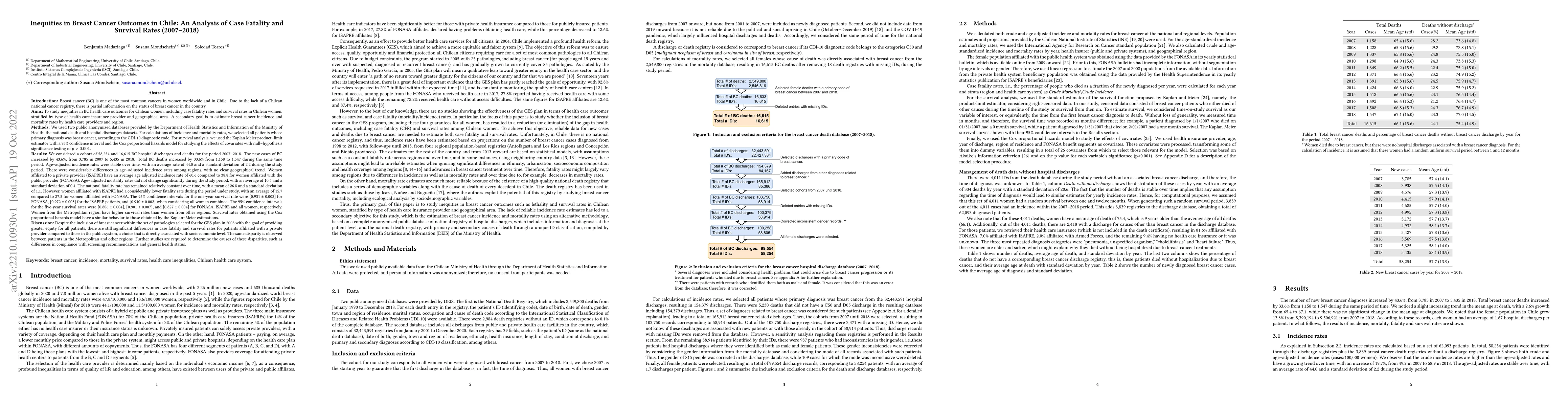

Introduction: The goal of this paper is to study inequities in breast cancer (BC) health care outcomes for Chilean women, including case fatality (FR) and survival rates (SR), stratified by type of ...

In this article we study the asymptotic behaviour of the least square estimator in a linear regression model based on random observation instances. We provide mild assumptions on the moments and dep...

In this article, we study the limit distribution of the least square estimator, properly normalized, from a regression model in which observations are assumed to be finite ($\alpha N$) and sampled u...

Generalisations of the Ornstein-Uhlenbeck process defined through Langevin equation $dU_t = - \Theta U_t dt + dG_t,$ such as fractional Ornstein-Uhlenbeck processes, have recently received a lot of ...

We study one-dimensional stochastic differential equations of form $dX_t = \sigma(X_t)dY_t$, where $Y$ is a suitable H\"older continuous driver such as the fractional Brownian motion $B^H$ with $H>\...

In this article we introduce and study oscillating Gaussian processes defined by $X_t = \alpha_+ Y_t {\bf 1}_{Y_t >0} + \alpha_- Y_t{\bf 1}_{Y_t<0}$, where $\alpha_+,\alpha_->0$ are free parameters ...

In this article, we study the explosion time of the solution to autonomous stochastic differential equations driven by the fractional Brownian motion with Hurst parameter $H>1/2$. With the help of the...

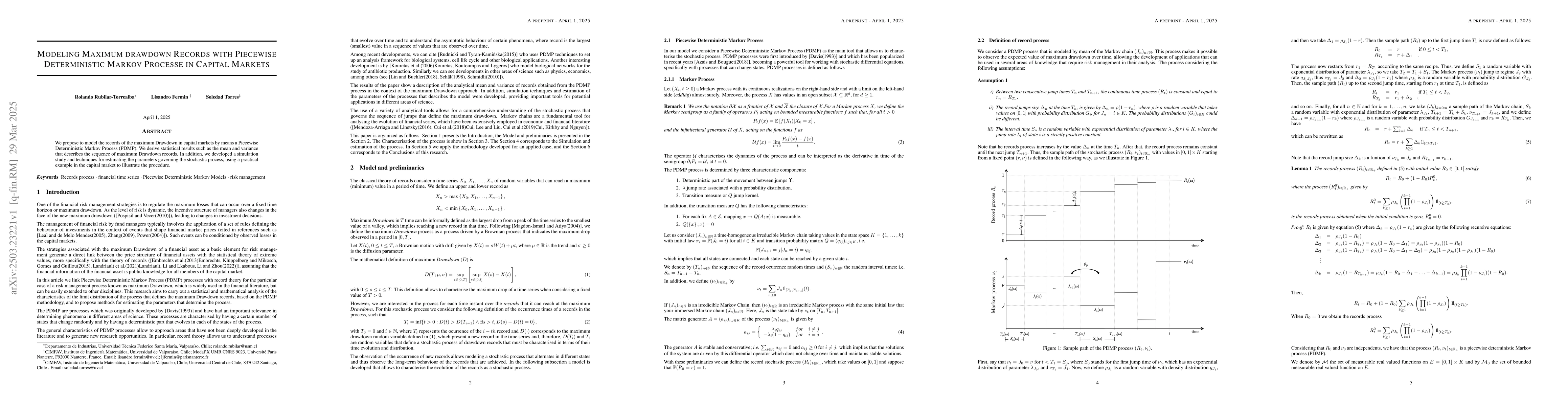

We propose to model the records of the maximum Drawdown in capital markets by means a Piecewise Deterministic Markov Process (PDMP). We derive statistical results such as the mean and variance that de...

In this paper, we apply rough paths techniques to provide an approximation of the solution of stochastic functional differential equations driven by fractional Brownian motion with Hurst parameter $H>...

We study a stochastic functional differential equation (SFDE) with memory driven by a fractional Brownian motion (fBm) with Hurst parameter H>1/2. An Euler-type numerical scheme is proposed and analyz...