Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a framework for the analysis of transmission channels in a large class of dynamic models. To this end, we formulate our approach both using graph theory and potential outcomes, which we s...

In this paper we test for Granger causality in high-dimensional vector autoregressive models (VARs) to disentangle and interpret the complex causal chains linking radiative forcings and global tempe...

In this paper we construct an inferential procedure for Granger causality in high-dimensional non-stationary vector autoregressive (VAR) models. Our method does not require knowledge of the order of...

We introduce a high-dimensional multiplier bootstrap for time series data based capturing dependence through a sparsely estimated vector autoregressive model. We prove its consistency for inference ...

In this paper, we estimate impulse responses by local projections in high-dimensional settings. We use the desparsified (de-biased) lasso to estimate the high-dimensional local projections, while le...

We propose a novel text-analytic approach for incorporating textual information into structural economic models and apply this to study the effects of tax news. We first develop a novel semi-supervi...

Unit root tests form an essential part of any time series analysis. We provide practitioners with a single, unified framework for comprehensive and reliable unit root testing in the R package bootUR...

In this paper we develop valid inference for high-dimensional time series. We extend the desparsified lasso to a time series setting under Near-Epoch Dependence (NED) assumptions allowing for non-Ga...

We investigate how the possible presence of unit roots and cointegration affects forecasting with Big Data. As most macroeoconomic time series are very persistent and may contain unit roots, a prope...

Ethane is the most abundant non-methane hydrocarbon in the Earth's atmosphere and an important precursor of tropospheric ozone through various chemical pathways. Ethane is also an indirect greenhous...

A fixed-design residual bootstrap method is proposed for the two-step estimator of Francq and Zako\"ian (2015) associated with the conditional Value-at-Risk. The bootstrap's consistency is proven fo...

In this paper we propose an autoregressive wild bootstrap method to construct confidence bands around a smooth deterministic trend. The bootstrap method is easy to implement and does not require any...

In many macroeconomic applications, confidence intervals for impulse responses are constructed by estimating VAR models in levels - ignoring cointegration rank uncertainty. We investigate the conseq...

We introduce a panel data model where coefficients vary both over time and the cross-section. Slope coefficients change smoothly over time and follow a latent group structure, being homogeneous within...

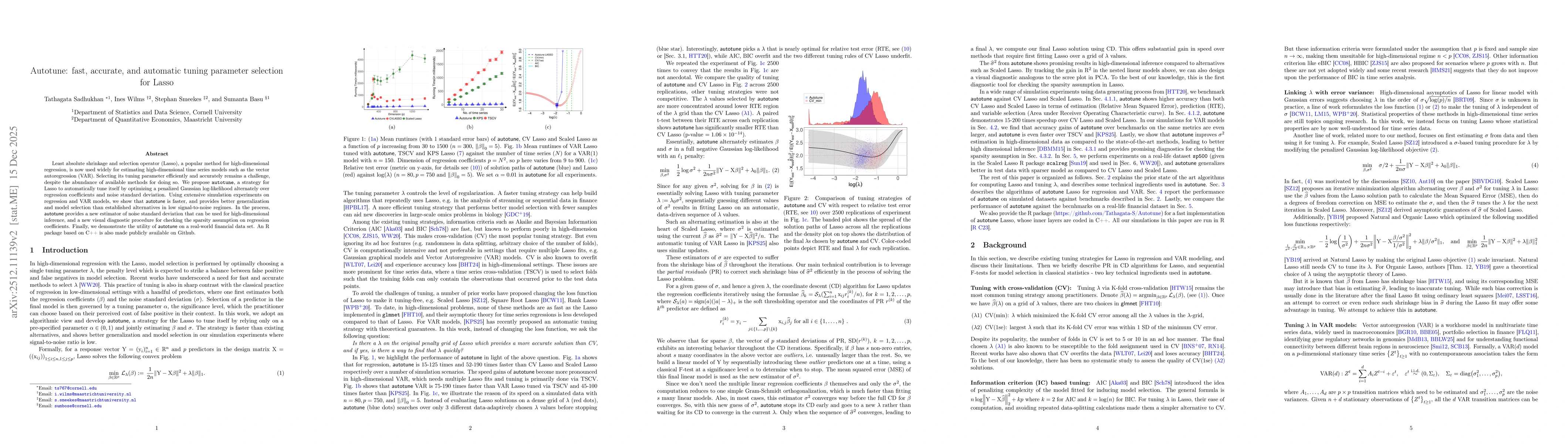

Least absolute shrinkage and selection operator (Lasso), a popular method for high-dimensional regression, is now used widely for estimating high-dimensional time series models such as the vector auto...

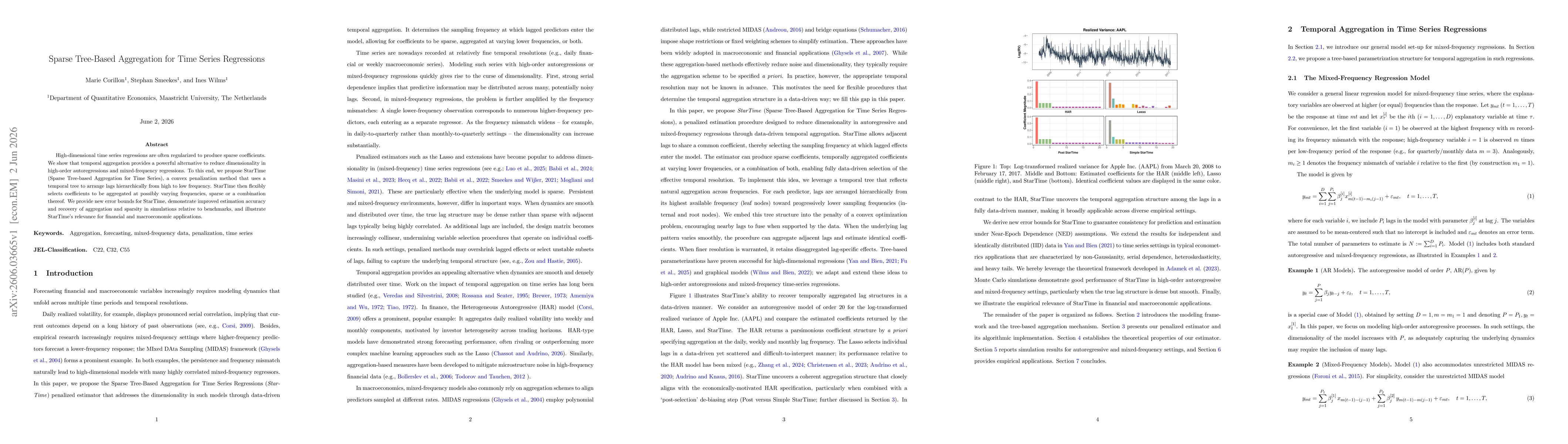

High-dimensional time series regressions are often regularized to produce sparse coefficients. We show that temporal aggregation provides a powerful alternative to reduce dimensionality in high-order ...