Academic Profile

Statistics

Similar Authors

Papers on arXiv

Time series forecasting is an active research topic in academia as well as industry. Although we see an increasing amount of adoptions of machine learning methods in solving some of those forecastin...

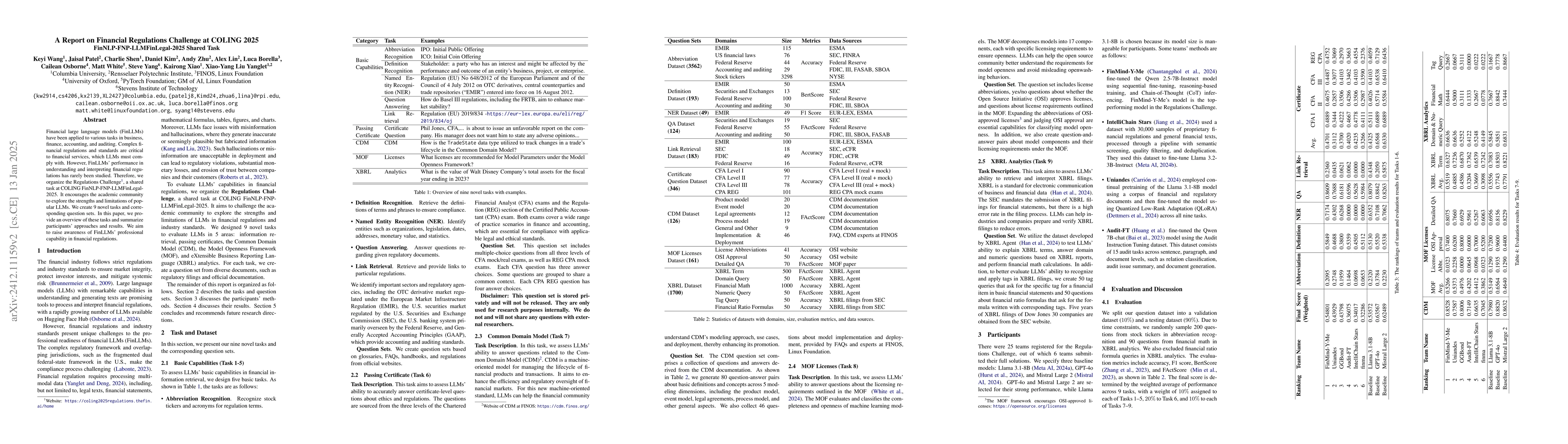

Financial large language models (FinLLMs) have been applied to various tasks in business, finance, accounting, and auditing. Complex financial regulations and standards are critical to financial servi...

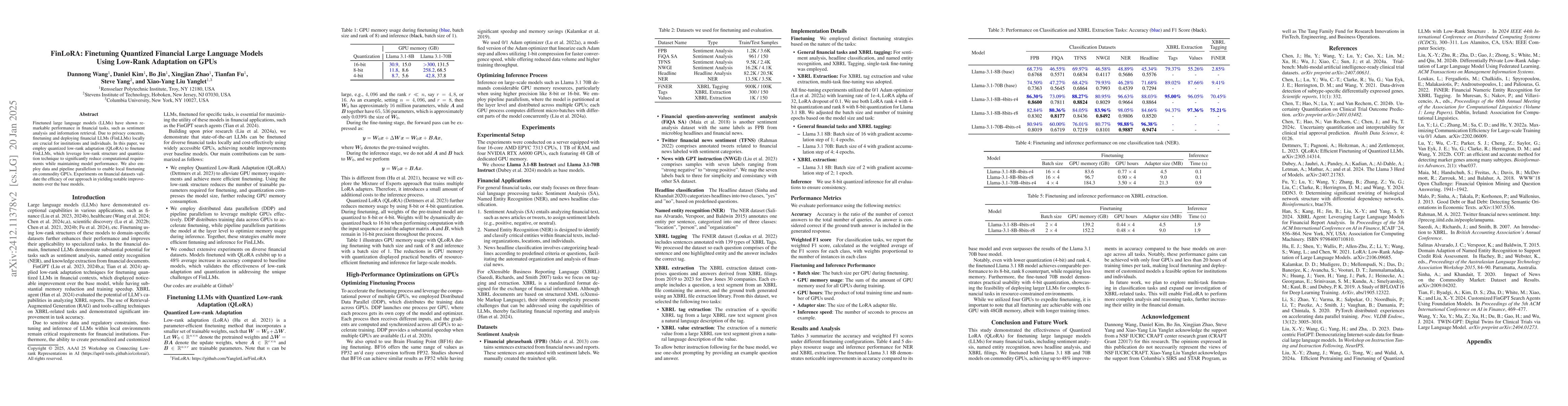

Finetuned large language models (LLMs) have shown remarkable performance in financial tasks, such as sentiment analysis and information retrieval. Due to privacy concerns, finetuning and deploying Fin...

In this study, we propose a novel integrated Generalized Autoregressive Conditional Heteroskedasticity-Gated Recurrent Unit (GARCH-GRU) model for financial volatility modeling and forecasting. The mod...

High-frequency trading (HFT) is an investing strategy that continuously monitors market states and places bid and ask orders at millisecond speeds. Traditional HFT approaches fit models with historica...