Academic Profile

Statistics

Similar Authors

Papers on arXiv

Real-world imaging systems acquire measurements that are degraded by noise, optical aberrations, and other imperfections that make image processing for human viewing and higher-level perception task...

We address the problem of strategic asset allocation (SAA) with portfolios that include illiquid alternative asset classes. The main challenge in portfolio construction with illiquid asset classes i...

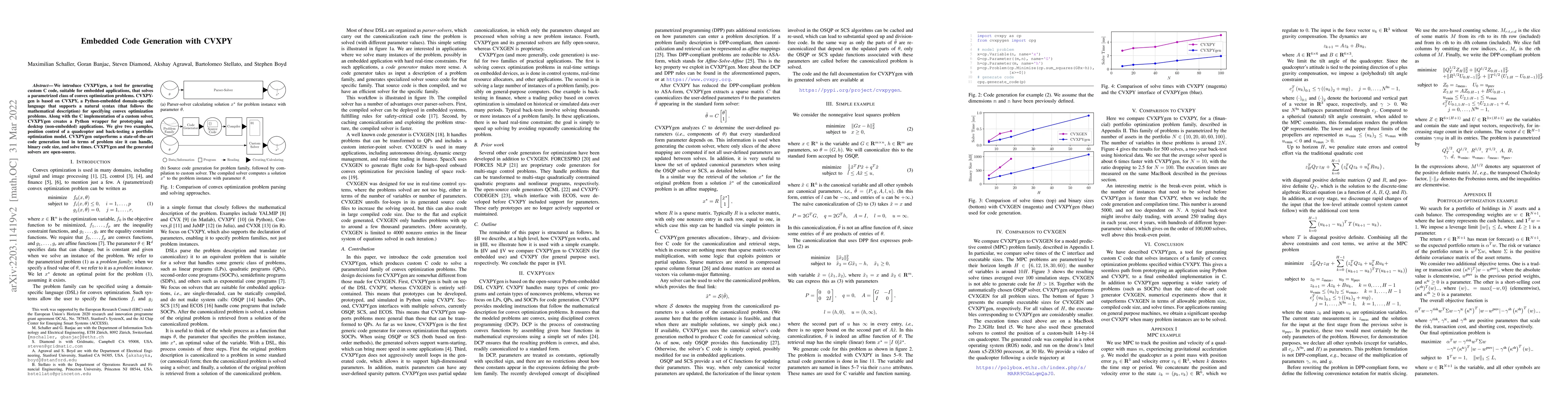

We introduce CVXPYgen, a tool for generating custom C code, suitable for embedded applications, that solves a parametrized class of convex optimization problems. CVXPYgen is based on CVXPY, a Python...

Using a lifecycle framework with Epstein-Zin (1989) utility and a mixed-integer optimization approach, we compute the optimal age to claim Social Security benefits. Taking advantage of homogeneity, ...

We present log-linear dynamical systems, a dynamical system model for positive quantities. We explain the connection to linear dynamical systems and show how convex optimization can be used to ident...

Recent work has shown how to embed differentiable optimization problems (that is, problems whose solutions can be backpropagated through) as layers within deep learning architectures. This method pr...

We introduce a fast and scalable method for solving quadratic programs with conditional value-at-risk (CVaR) constraints. While these problems can be formulated as standard quadratic programs, the num...

Chemical reaction networks in living cells maintain precise control over thousands of metabolites despite operating far from equilibrium under constant perturbations. While mass action kinetics accura...

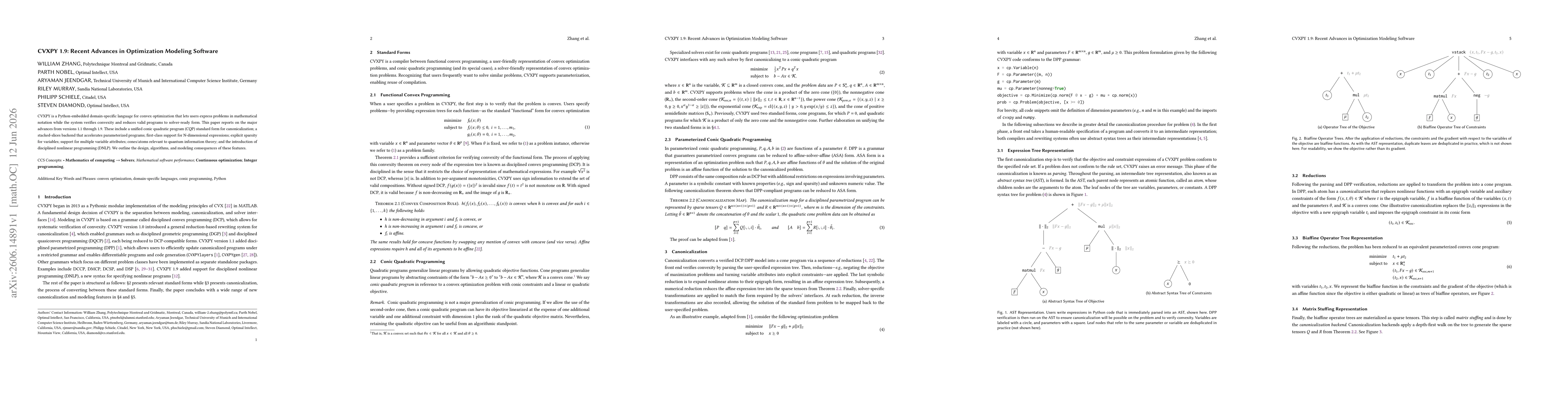

CVXPY is a Python-embedded domain-specific language for convex optimization that lets users express problems in mathematical notation while the system verifies convexity and reduces valid programs to ...