Academic Profile

Statistics

Similar Authors

Papers on arXiv

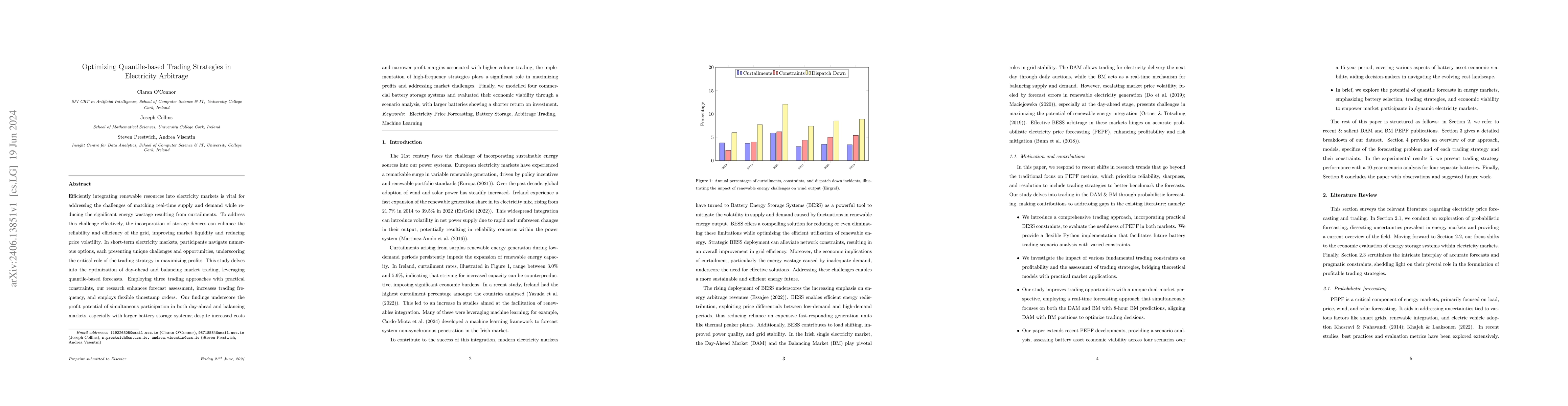

Efficiently integrating renewable resources into electricity markets is vital for addressing the challenges of matching real-time supply and demand while reducing the significant energy wastage result...

Only two Croston-style forecasting methods are currently known for handling stochastic intermittent demand with possible demand obsolescence: TSB and HES, both shown to be unbiased. When an item bec...

Short-term electricity markets are becoming more relevant due to less-predictable renewable energy sources, attracting considerable attention from the industry. The balancing market is the closest t...

Predicting future resource demand in Cloud Computing is essential for optimizing the trade-off between serving customers' requests efficiently and minimizing the provisioning cost. Modelling predict...

The (R, s, S) is a stochastic inventory control policy widely used by practitioners. In an inventory system managed according to this policy, the inventory is reviewed at instant R; if the observed ...

In this study we propose a hybrid estimation of distribution algorithm (HEDA) to solve the joint stratification and sample allocation problem. This is a complex problem in which each the quality of ...

In this paper we combine the k-means and/or k-means type algorithms with a hill climbing algorithm in stages to solve the joint stratification and sample allocation problem. This is a combinatorial ...

A well-know control policy in stochastic inventory control is the (R, s, S) policy, in which inventory is raised to an order-up-to-level S at a review instant R whenever it falls below reorder-level...

This study combines simulated annealing with delta evaluation to solve the joint stratification and sample allocation problem. In this problem, atomic strata are partitioned into mutually exclusive ...

In this work we compare several new computational approaches to an inventory routing problem, in which a single product is shipped from a warehouse to retailers via an uncapacitated vehicle. We surv...

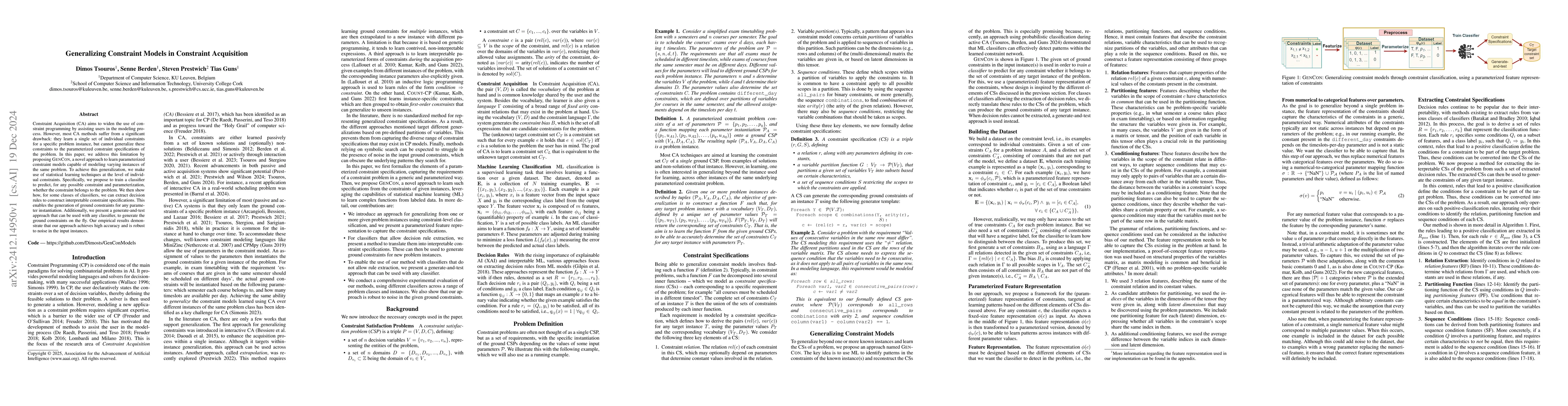

Constraint Acquisition (CA) aims to widen the use of constraint programming by assisting users in the modeling process. However, most CA methods suffer from a significant drawback: they learn a single...

Electricity price forecasting has become a critical tool for decision-making in energy markets, particularly as the increasing penetration of renewable energy introduces greater volatility and uncerta...