Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we introduce a novel method for predicting intraday instantaneous volatility based on Ito semimartingale models using high-frequency financial data. Several studies have highlighted s...

In this paper, we develop a novel large volatility matrix estimation procedure for analyzing global financial markets. Practitioners often use lower-frequency data, such as weekly or monthly returns...

Several large volatility matrix inference procedures have been developed, based on the latent factor model. They often assumed that there are a few of common factors, which can account for volatilit...

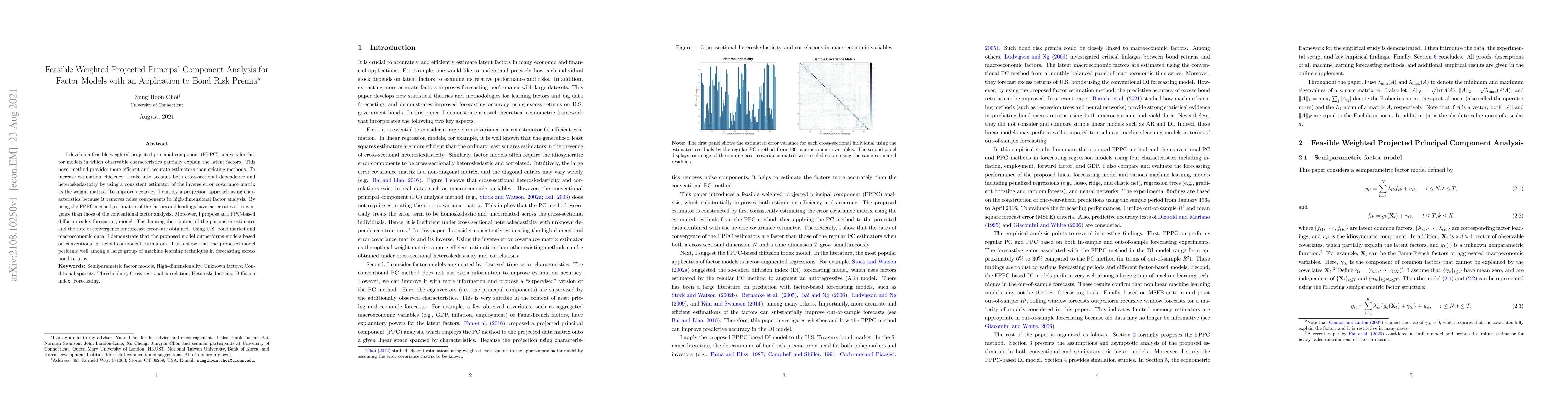

I develop a feasible weighted projected principal component (FPPC) analysis for factor models in which observable characteristics partially explain the latent factors. This novel method provides mor...

This paper develops a new standard-error estimator for linear panel data models. The proposed estimator is robust to heteroskedasticity, serial correlation, and cross-sectional correlation of unknow...

In this paper, we develop a novel method for predicting future large volatility matrices based on high-dimensional factor-based It\^o processes. Several studies have proposed volatility matrix predict...

Based on It\^o semimartingale models, several studies have proposed methods for forecasting intraday volatility using high-frequency financial data. These approaches typically rely on restrictive para...