Academic Profile

Statistics

Similar Authors

Papers on arXiv

We suggest new closely related methods for numerical inversion of $Z$-transform and Wiener-Hopf factorization of functions on the unit circle, based on sinh-deformations of the contours of integrati...

This paper is a supplement to our recent paper ``Alternative models for FX, arbitrage opportunities and efficient pricing of double barrier options in L\'evy models". We introduce the class of regim...

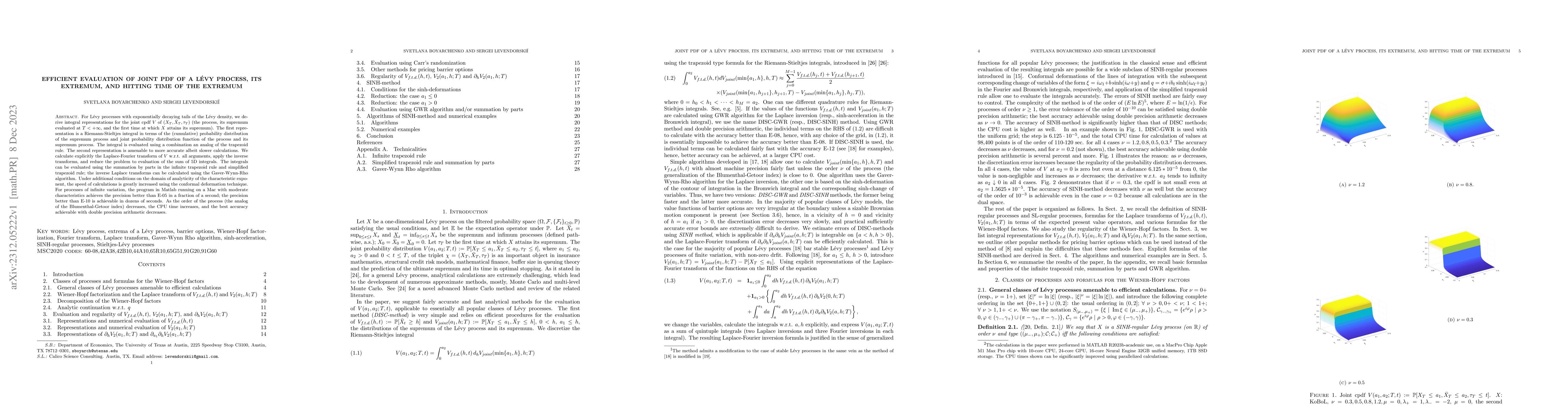

For L\'evy processes with exponentially decaying tails of the L\'evy density, we derive integral representations for the joint cpdf $V$ of $(X_T, \bar X_T,\tau_T)$ (the process, its supremum evaluat...

We suggest a general framework for simulation of the triplet $(X_T,\bar X_ T,\tau_T)$ (L\'evy process, its extremum, and hitting time of the extremum), and, separately, $X_T,\bar X_ T$ and pairs $(X...

We analyze the qualitative differences between prices of double barrier no-touch options in the Heston model and pure jump KoBoL model calibrated to the same set of the empirical data, and discuss t...

We derive several sets of sufficient conditions for applicability of the new efficient numerical realization of the inverse $Z$-transform. For large $n$, the complexity of the new scheme is dozens o...

In the paper, we develop a very fast and accurate method for pricing double barrier options with continuous monitoring in wide classes of L\'evy models; the calculations are in the dual space, and t...

Integral representations for expectations of functions of a stable L\'evy process $X$ and its supremum $\bar X$ are derived. As examples, cumulative probability distribution functions (cpdf) of $X_T...

We prove simple general formulas for expectations of functions of a random walk and its running extremum. Under additional conditions, we derive analytical formulas using the inverse $Z$-transform, ...

In our previous publications (IJTAF 2019, Math. Finance 2020), we introduced a general class of SINH-regular processes and demonstrated that efficient numerical methods for the evaluation of the Wie...

We clarify the relations among different Fourier-based approaches to option pricing, and improve the B-spline probability density projection method using the sinh-acceleration technique. This allows...

We use modifications of the Adams method and very fast and accurate sinh-acceleration method of the Fourier inversion (iFT) (S.Boyarchenko and Levendorski\u{i}, IJTAF 2019, v.22) to evaluate prices of...

The present paper is an addendum to the paper ``L\'evy models amenable to efficient calculations", where we introduced a general class of Stieltjes-L\'evy processes (SL-processes) and signed SL proces...

The paper is an extended and modified version of the preprint S.Boyarchenko and S.Levendorski\u{i} ``Correct implied volatility shapes and reliable pricing in the rough Heston model". We combine a mod...