Academic Profile

Statistics

Similar Authors

Papers on arXiv

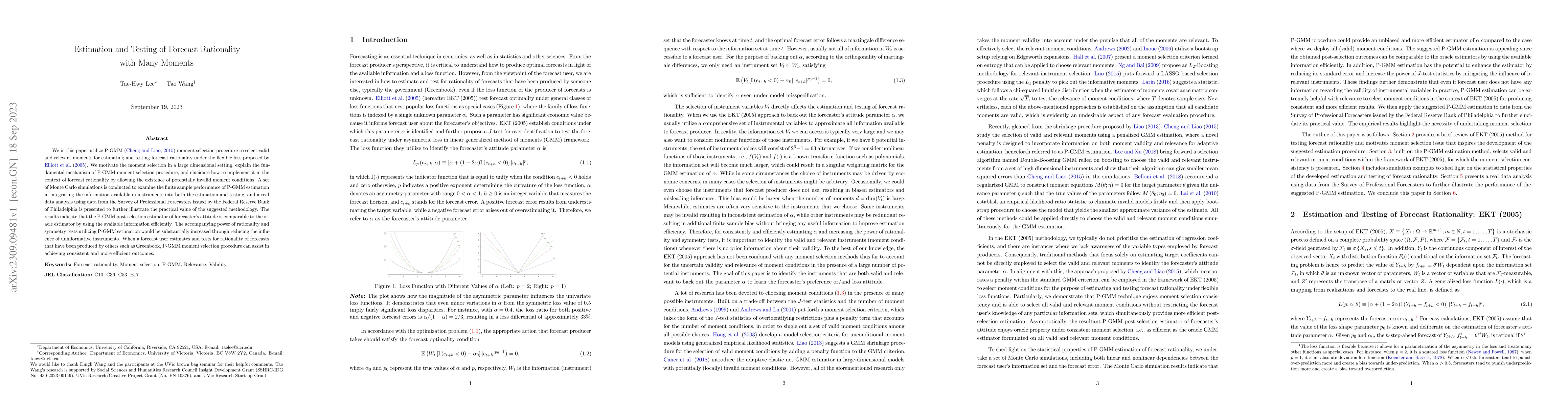

We in this paper utilize P-GMM (Cheng and Liao, 2015) moment selection procedure to select valid and relevant moments for estimating and testing forecast rationality under the flexible loss proposed...

In this paper we develop a novel method of combining many forecasts based on a machine learning algorithm called Graphical LASSO (GL). We visualize forecast errors from different forecasters as a ne...

The Granular Instrumental Variables (GIV) methodology exploits panels with factor error structures to construct instruments to estimate structural time series models with endogeneity even after cont...

Forecasters often use common information and hence make common mistakes. We propose a new approach, Factor Graphical Model (FGM), to forecast combinations that separates idiosyncratic forecast error...

Graphical models are a powerful tool to estimate a high-dimensional inverse covariance (precision) matrix, which has been applied for a portfolio allocation problem. The assumption made by these mod...