2

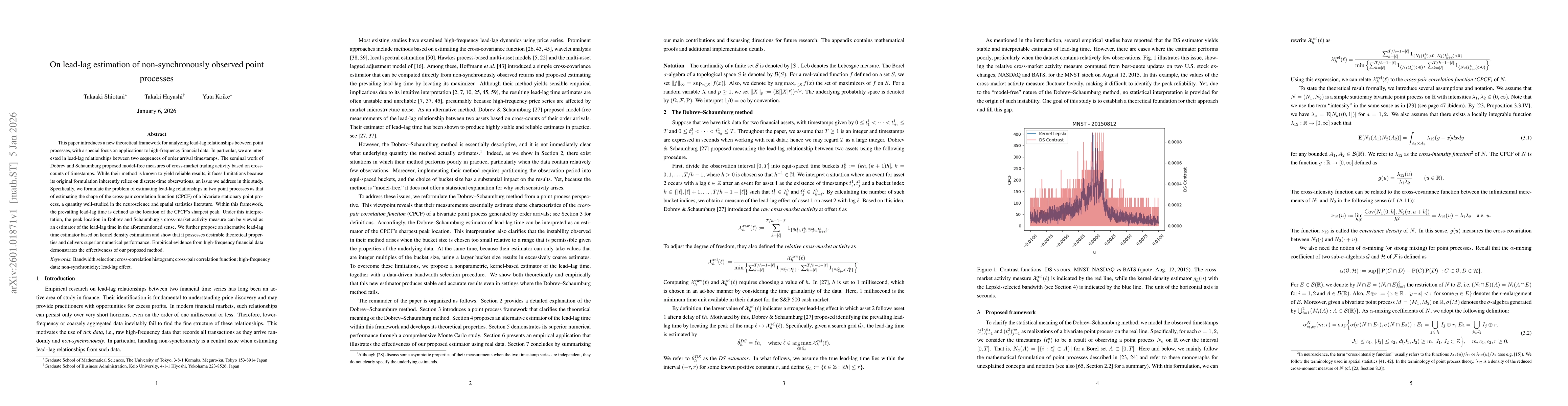

arXiv Papers

2

Total Publications

Profile

Academic Profile

Metrics

Statistics

2

arXiv Papers

2

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Statistical inference for highly correlated stationary point processes

and noisy bivariate Neyman-Scott processes

Motivated by estimating the lead-lag relationships in high-frequency financial data, we propose noisy bivariate Neyman-Scott point processes with gamma kernels (NBNSP-G). NBNSP-G tolerates noises that...

arXiv

On lead-lag estimation of non-synchronously observed point processes

This paper introduces a new theoretical framework for analyzing lead-lag relationships between point processes, with a special focus on applications to high-frequency financial data. In particular, we...