Academic Profile

Statistics

Similar Authors

Papers on arXiv

It is well-known that the approximate factor models have the rotation indeterminacy. It has been considered that the principal component (PC) estimators estimate some rotations of the true factors a...

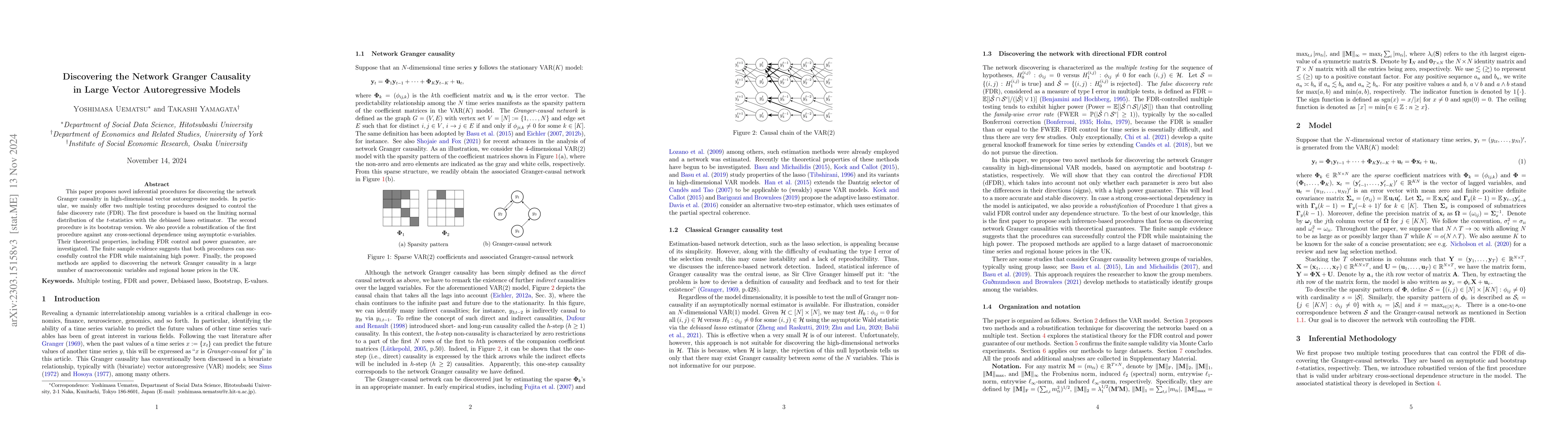

This paper proposes novel inferential procedures for discovering the network Granger causality in high-dimensional vector autoregressive models. In particular, we mainly offer two multiple testing p...

This paper develops a Mean Group Instrumental Variables (MGIV) estimator for spatial dynamic panel data models with interactive effects, under large N and T asymptotics. Unlike existing approaches tha...

In this paper, we study the asymptotic bias of the factor-augmented regression estimator and its reduction, which is augmented by the $r$ factors extracted from a large number of $N$ variables with $T...

In this paper, we propose a novel bootstrap algorithm that is more efficient than existing methods for approximating the distribution of the factor-augmented regression estimator for a rotated paramet...