Academic Profile

Statistics

Similar Authors

Papers on arXiv

A novel procedure is presented for finding the true but latent endpoints within the repayment histories of individual loans. The monthly observations beyond these true endpoints are false, largely d...

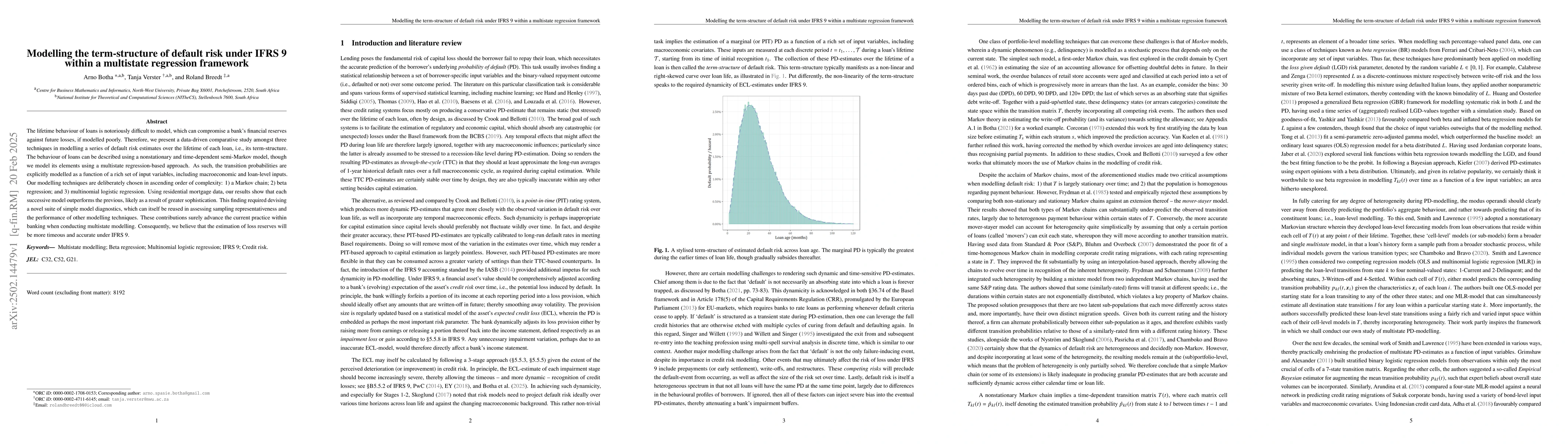

The lifetime behaviour of loans is notoriously difficult to model, which can compromise a bank's financial reserves against future losses, if modelled poorly. Therefore, we present a data-driven compa...

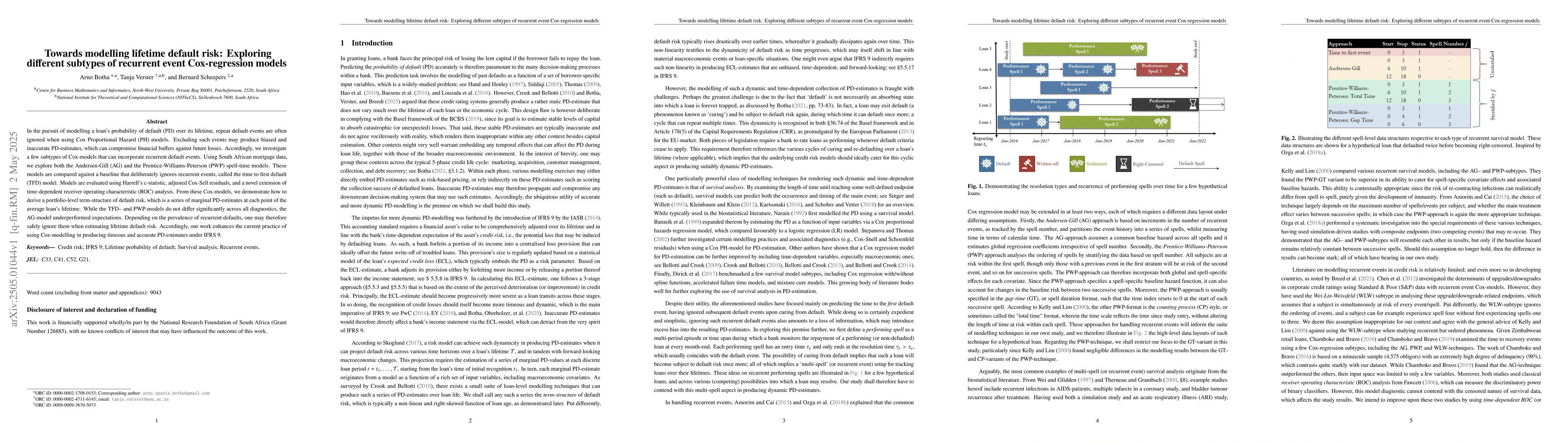

In the pursuit of modelling a loan's probability of default (PD) over its lifetime, repeat default events are often ignored when using Cox Proportional Hazard (PH) models. Excluding such events may pr...

Under the International Financial Reporting Standards (IFRS) 9, credit losses ought to be recognised timeously and accurately. This requirement belies a certain degree of dynamicity when estimating th...