Academic Profile

Statistics

Similar Authors

Papers on arXiv

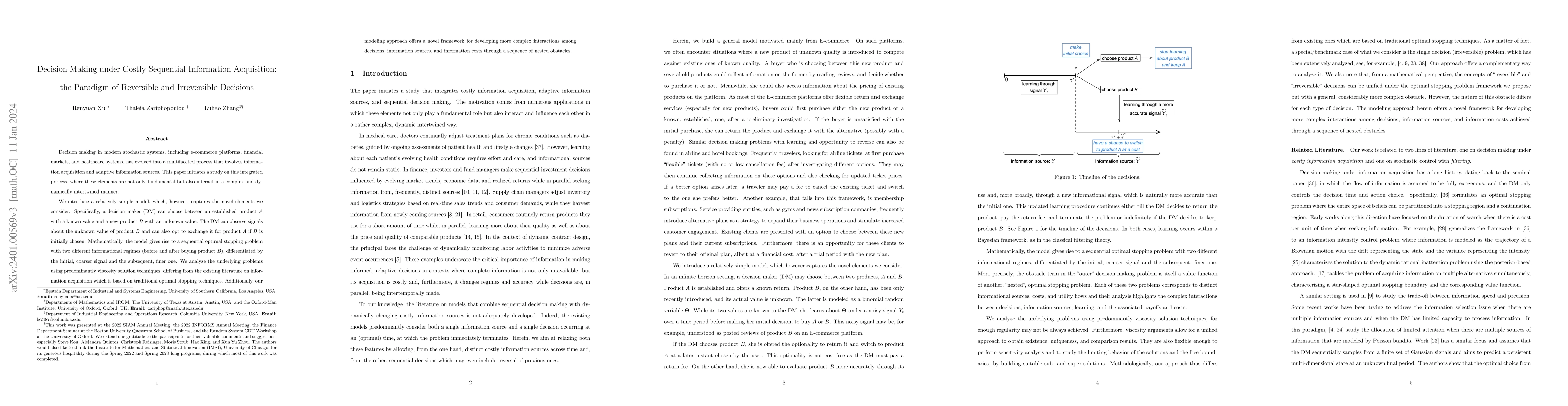

Decision making in modern stochastic systems, including e-commerce platforms, financial markets, and healthcare systems, has evolved into a multifaceted process that involves information acquisition...

We extend the notion of forward performance criteria to settings with random endowment in incomplete markets. Building on these results, we introduce and develop the novel concept of forward optimiz...

In an Ito-diffusion market, two fund managers trade under relative performance concerns. For both the asset specialization and diversification settings, we analyze the passive and competitive cases....

Entropy regularization has been extensively adopted to improve the efficiency, the stability, and the convergence of algorithms in reinforcement learning. This paper analyzes both quantitatively and...

We study optimal portfolio choice models in markets with partial information about the stock's drift. We solve the single agent problem for general utilities using a new approach that yields regularit...