Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper studies an optimal insurance contracting problem in which the preferences of the decision maker given by the sum of the expected loss and a convex, increasing function of a deviation meas...

We examine a problem of demand for insurance indemnification, when the insured is sensitive to ambiguity and behaves according to the Maxmin-Expected Utility model of Gilboa and Schmeidler (1989), w...

We introduce a strategic behavior in reinsurance bilateral transactions, where agents choose the risk preferences they will appear to have in the transaction. Within a wide class of risk measures, w...

This paper considers an insurance company that faces two key constraints: a ratcheting dividend constraint and an irreversible reinsurance constraint. The company allocates part of its reserve to pay ...

This paper explores optimal insurance solutions based on the Lambda-Value-at-Risk ($\Lambda\VaR$). If the expected value premium principle is used, our findings confirm that, similar to the VaR model,...

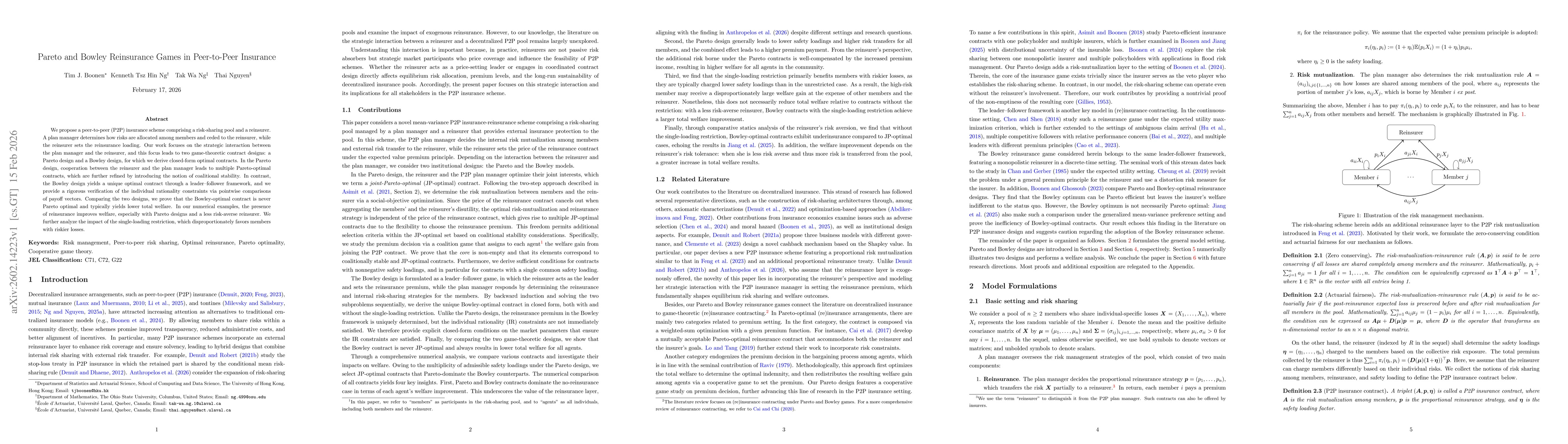

This paper considers an insurer with two collaborating business lines, and the risk exposure of each line follows a diffusion risk model. The manager of the insurer makes three decisions for each line...

This paper considers an insurer with two collaborating business lines that must make three critical decisions: (1) dividend payout, (2) a combination of proportional and excess-of-loss reinsurance cov...

This study models the monopoly pricing of weather index insurance as a Bowley-type sequential game involving a profit-maximizing insurer (leader) and a farmer (follower). The farmer chooses an insuran...

This paper studies Pareto-optimal reinsurance design in a monopolistic market with multiple primary insurers and a single reinsurer, all with heterogeneous risk preferences. The risk preferences are c...

Machine learning improves predictive accuracy in insurance pricing but exacerbates trade-offs between competing fairness criteria across different discrimination measures, challenging regulators and i...

We propose a peer-to-peer (P2P) insurance scheme comprising a risk-sharing pool and a reinsurer. A plan manager determines how risks are allocated among members and ceded to the reinsurer, while the r...

This paper considers an insurer with two collaborating business lines that faces three critical decisions: (1) dividend payout, (2) reinsurance coverage, and (3) capital injection between the lines, i...