Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper analyzes a problem of optimal static hedging using derivatives in incomplete markets. The investor is assumed to have a risk exposure to two underlying assets. The hedging instruments are...

This paper analyzes the robust long-term growth rate of expected utility and expected return from holding a leveraged exchange-traded fund (LETF). When the Markovian model parameters in the referenc...

We present the method of complementary ensemble empirical mode decomposition (CEEMD) and Hilbert-Huang transform (HHT) for analyzing nonstationary financial time series. This noise-assisted approach...

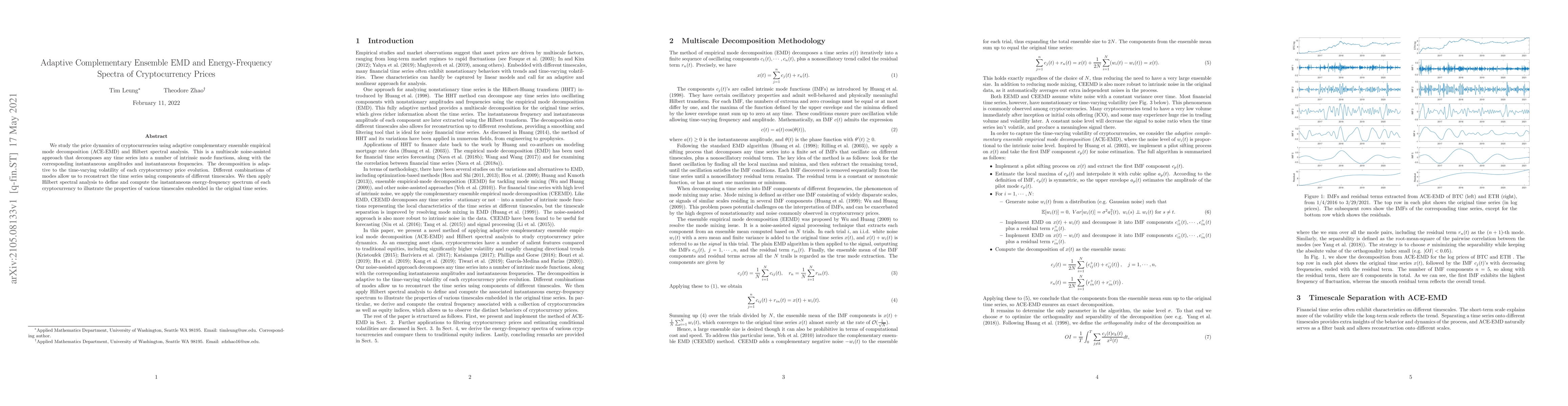

We study the price dynamics of cryptocurrencies using adaptive complementary ensemble empirical mode decomposition (ACE-EMD) and Hilbert spectral analysis. This is a multiscale noise-assisted approa...

We study the problem of dynamically trading multiple futures whose underlying asset price follows a multiscale central tendency Ornstein-Uhlenbeck (MCTOU) model. Under this model, we derive the clos...

We study the problem of dynamically trading futures in a regime-switching market. Modeling the underlying asset price as a Markov-modulated diffusion process, we present a utility maximization appro...

We study the problem of dynamically trading multiple futures contracts with different underlying assets. To capture the joint dynamics of stochastic bases for all traded futures, we propose a new mo...

We study a series of static and dynamic portfolios of VIX futures and their effectiveness to track the VIX index. We derive each portfolio using optimization methods, and evaluate its tracking perfo...

We study the problem of dynamically trading a futures contract and its underlying asset under a stochastic basis model. The basis evolution is modeled by a stopped scaled Brownian bridge to account ...

We consider a financial market in which the short rate is modeled by a continuous time Markov chain (CTMC) with a finite state space. In this setting, we show how to price any financial derivative who...

We consider the pricing of energy spread options for spot prices following an exponential Ornstein-Uhlenbeck process driven by a sum of independent multivariate variance gamma processes. Within this c...

We price European options in a class of models in which the volatility of the underlying risky asset depends on the short rate of interest. Our study results in an explicit pricing formula that depend...