Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce methodology to bridge scenario analysis and model-based risk forecasting, leveraging their respective strengths in policy settings. Our Bayesian framework addresses the fundamental challe...

We analyse growth vulnerabilities in the US using quantile partial correlation regression, a selection-based machine-learning method that achieves model selection consistency under time series. We fin...

The Growth-at-Risk (GaR) framework has garnered attention in recent econometric literature, yet current approaches implicitly assume a constant Pareto exponent. We introduce novel and robust econometr...

We discuss probabilistic measures of concordance between two probability distributions based on the expected misclassification rate (EMR). The focus is on comparing a given reference distribution with...

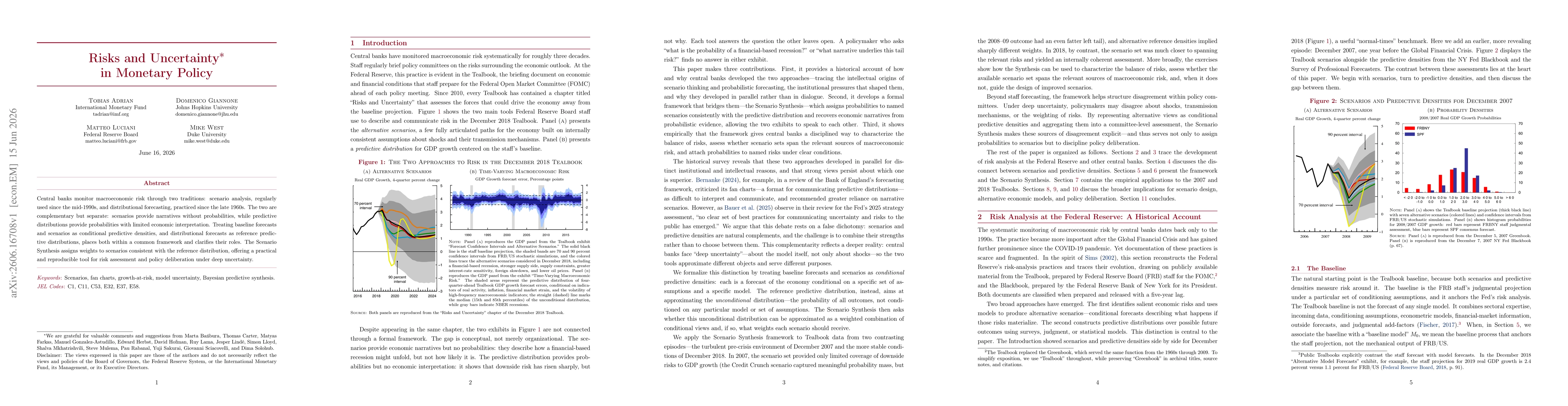

Central banks monitor macroeconomic risk through two traditions: scenario analysis, regularly used since the mid-1990s, and distributional forecasting, practiced since the late 1960s. The two are comp...