Academic Profile

Statistics

Similar Authors

Papers on arXiv

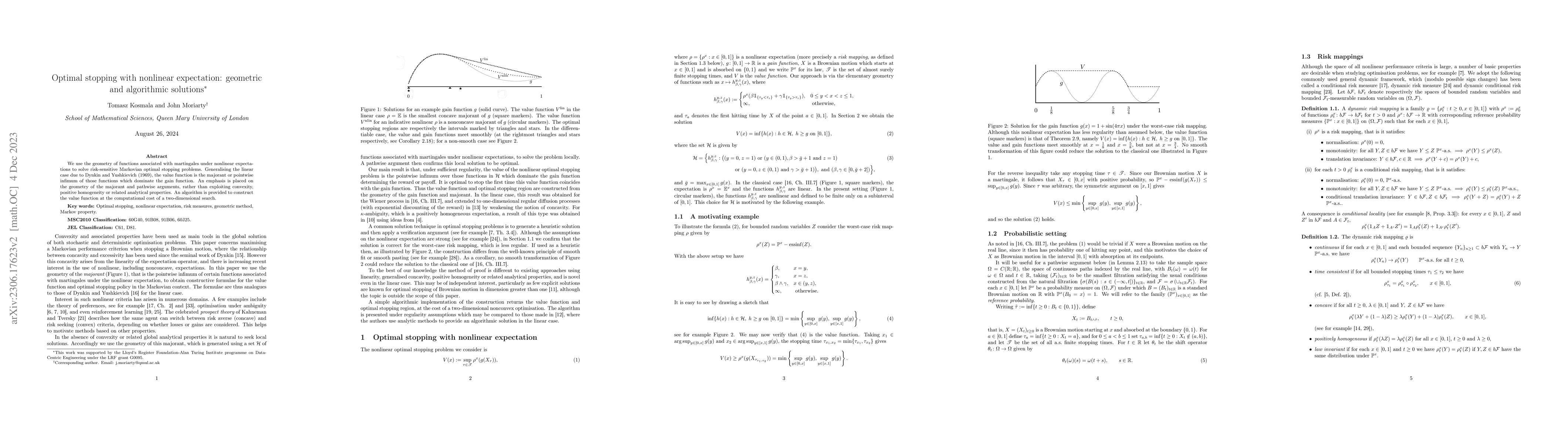

We use the geometry of functions associated with martingales under nonlinear expectations to solve risk-sensitive Markovian optimal stopping problems. Generalising the linear case due to Dynkin and ...

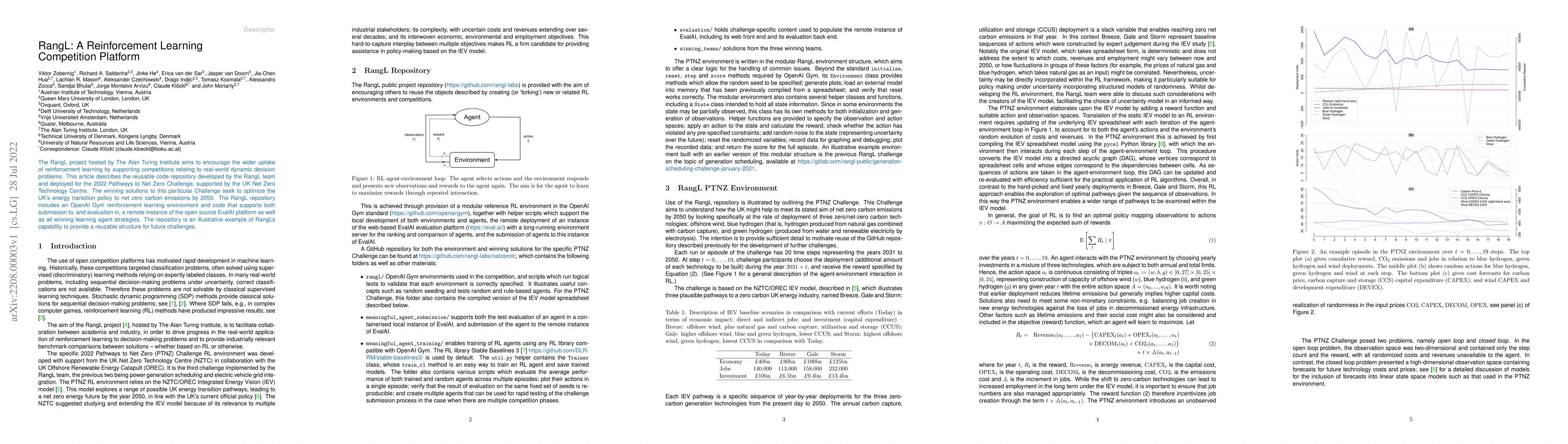

The RangL project hosted by The Alan Turing Institute aims to encourage the wider uptake of reinforcement learning by supporting competitions relating to real-world dynamic decision problems. This a...

We prove existence and uniqueness of a mild solution of a stochastic evolution equation driven by a standard $\alpha$-stable cylindrical L\'evy process defined on a Hilbert space for $\alpha \in (1,...

We formulate a probabilistic Markov property in discrete time under a dynamic risk framework with minimal assumptions. This is useful for recursive solutions to risk-sensitive versions of dynamic op...

We introduce a stochastic integral with respect to cylindrical L\'evy processes with finite $p$-th weak moment for $p\in [1,2]$. The space of integrands consists of $p$-summing operators between Ban...

In this paper we prove the existence of weak martingale solutions to the stochastic Navier-Stokes Equations driven by pure jump L\'evy processes. Our proof consists of two parts. In the first one, mos...