Academic Profile

Statistics

Similar Authors

Papers on arXiv

The aim of this work is to study risk measures generated by distortion functions in a dynamic discrete time setup, and to investigate the corresponding dynamic coherent acceptability indices (DCAIs)...

We consider an additive functional driven by a time-inhomogeneous Markov chain with a finite state space. Our study focuses on the joint distribution of the two-sided exit time and the state of the ...

We consider a Markov decision process subject to model uncertainty in a Bayesian framework, where we assume that the state process is observed but its law is unknown to the observer. In addition, wh...

In this paper we study a class of risk-sensitive Markovian control problems in discrete time subject to model uncertainty. We consider a risk-sensitive discounted cost criterion with finite time hor...

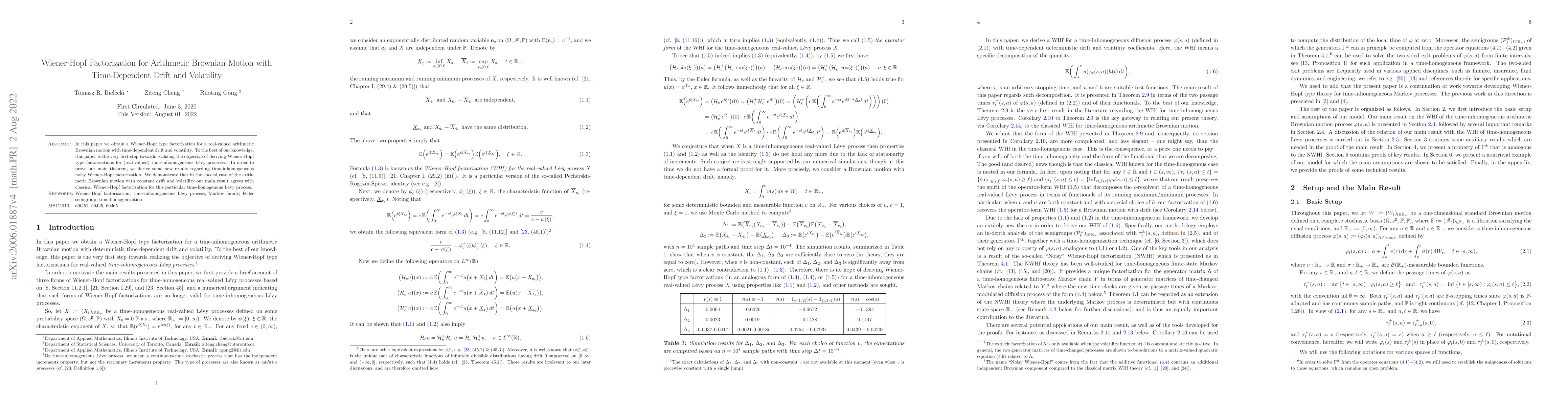

In this paper we obtain a Wiener-Hopf type factorization for a real-valued arithmetic Brownian motion with time-dependent drift and volatility. To the best of our knowledge, this paper is the very f...

This work contributes to the theory and applications of Hawkes processes. We introduce and examine a new class of Hawkes processes that we call generalized Hawkes processes, and their special subcla...

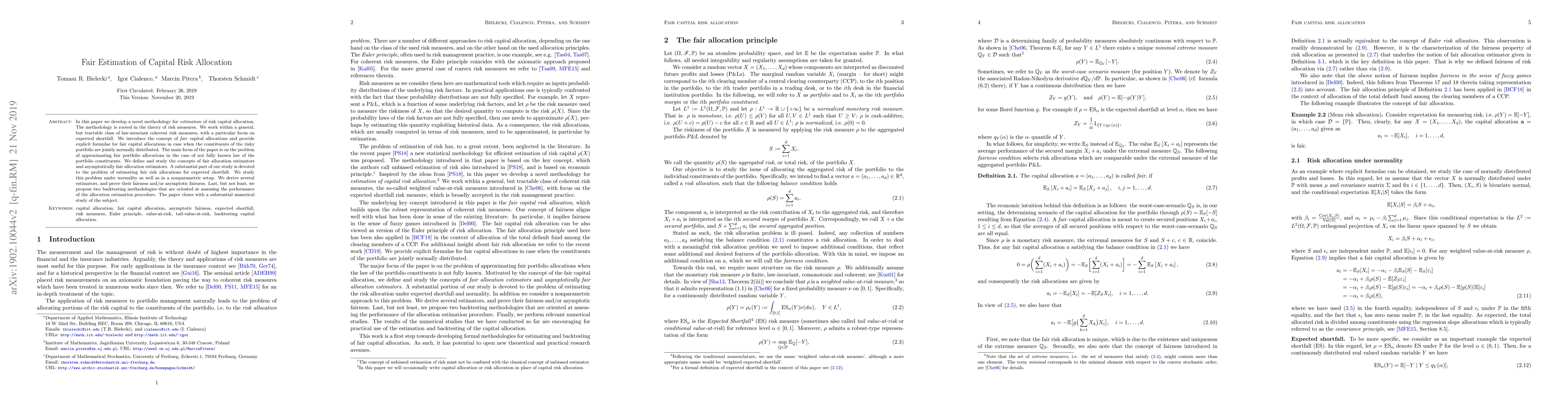

In this paper we develop a novel methodology for estimation of risk capital allocation. The methodology is rooted in the theory of risk measures. We work within a general, but tractable class of law...

We consider a complete probability space $(\Omega,\mathcal{F},\mathbb{P})$, which is endowed with two filtrations, $\mathbb{G}$ and $\mathbb{F}$, assumed to satisfy the usual conditions and such tha...

This paper discusses a special class of nonlinear Hawkes processes, where the rate function is the exponential function. We call these processes loglinear Hawkes processes. In the main theorem, we giv...

We give functional laws of large numbers for a class of marked Hawkes processes and marked compound Hawkes processes with a general mark space. Our results provide some complement to those presented p...

Robo-advisors (RAs) are automated portfolio management systems that complement traditional financial advisors by offering lower fees and smaller initial investment requirements. While most existing RA...