Academic Profile

Statistics

Similar Authors

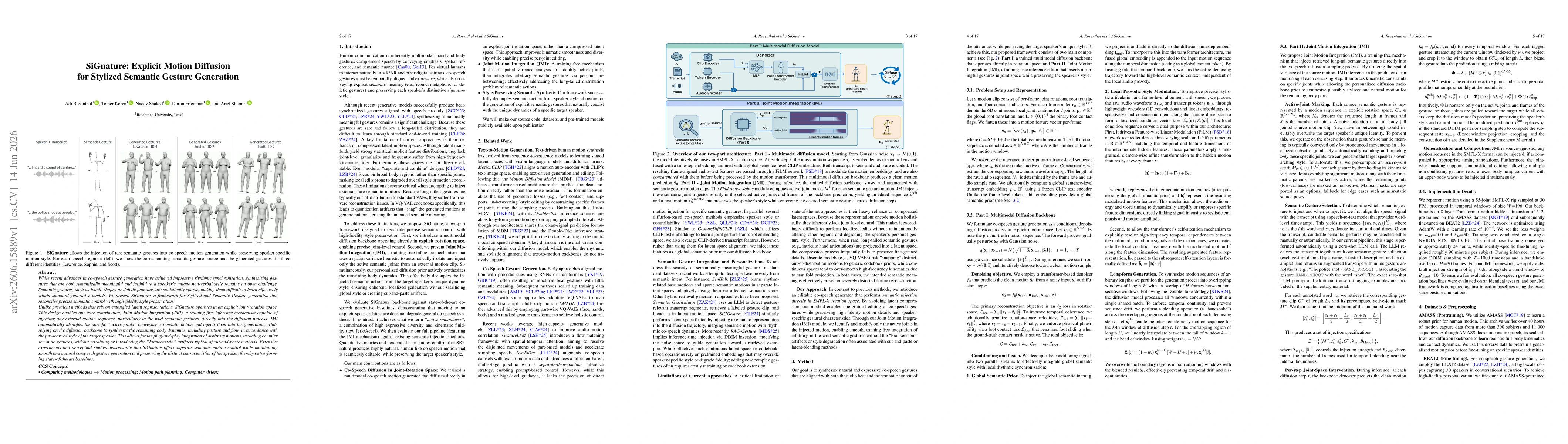

Papers on arXiv

We revisit the classical problem of multiclass classification with bandit feedback (Kakade, Shalev-Shwartz and Tewari, 2008), where each input classifies to one of $K$ possible labels and feedback is ...

We study multiclass PAC learning with bandit feedback, where inputs are classified into one of $K$ possible labels and feedback is limited to whether or not the predicted labels are correct. Our main ...

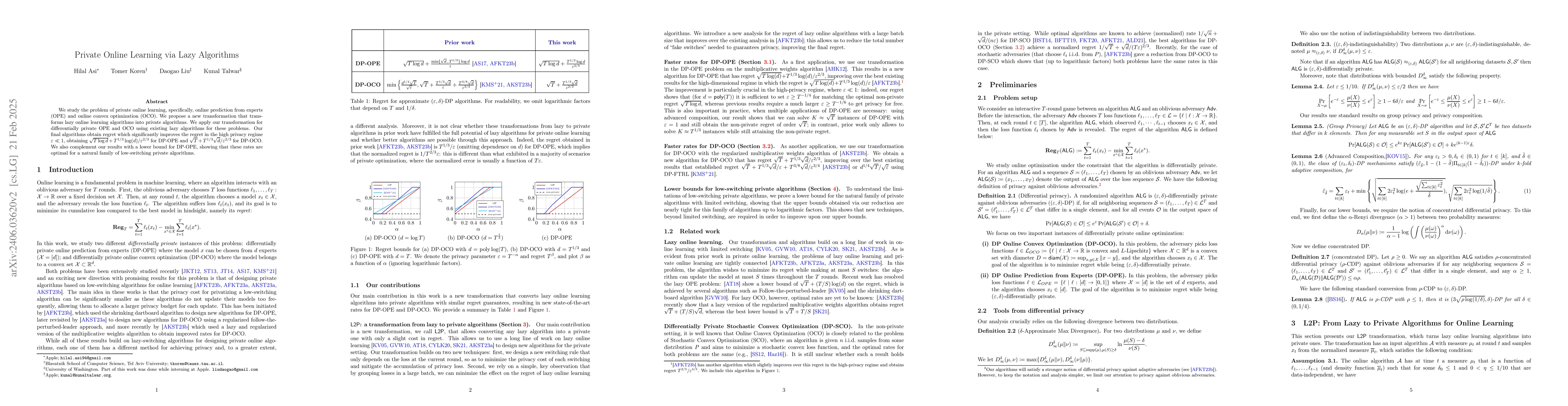

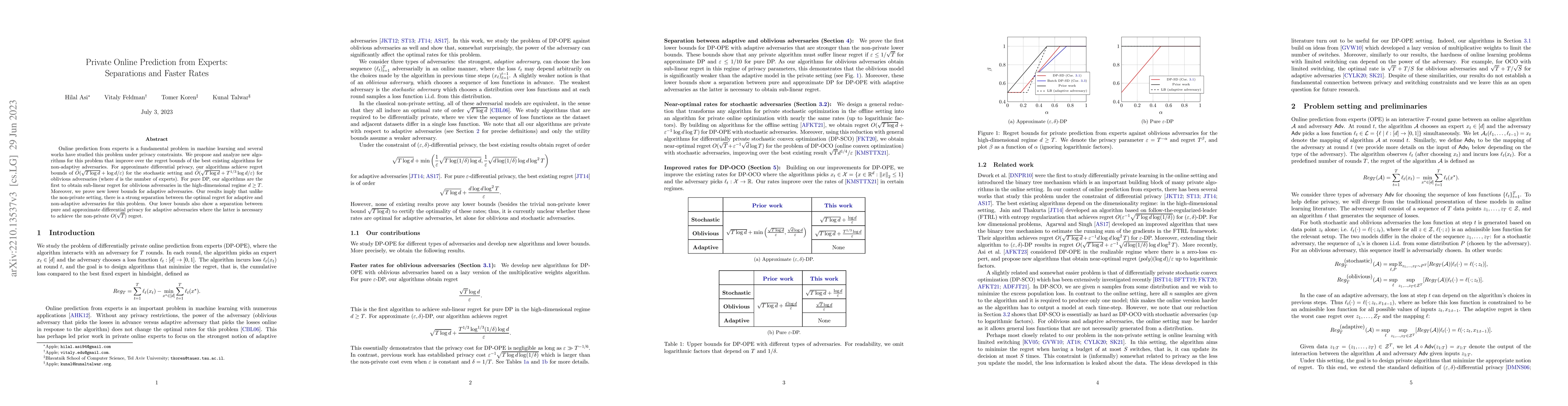

We study the problem of private online learning, specifically, online prediction from experts (OPE) and online convex optimization (OCO). We propose a new transformation that transforms lazy online ...

This short note describes a simple technique for analyzing probabilistic algorithms that rely on a light-tailed (but not necessarily bounded) source of randomization. We show that the analysis of su...

We study the problem of parameter-free stochastic optimization, inquiring whether, and under what conditions, do fully parameter-free methods exist: these are methods that achieve convergence rates ...

We study the generalization performance of gradient methods in the fundamental stochastic convex optimization setting, focusing on its dimension dependence. First, for full-batch gradient descent (G...

We address the problem of convex optimization with preference feedback, where the goal is to minimize a convex function given a weaker form of comparison queries. Each query consists of two points a...

We introduce a novel dynamic learning-rate scheduling scheme grounded in theory with the goal of simplifying the manual and time-consuming tuning of schedules in practice. Our approach is based on e...

We study regret minimization in online episodic linear Markov Decision Processes, and obtain rate-optimal $\widetilde O (\sqrt K)$ regret where $K$ denotes the number of episodes. Our work is the fi...

We study the generalization properties of unregularized gradient methods applied to separable linear classification -- a setting that has received considerable attention since the pioneering work of...

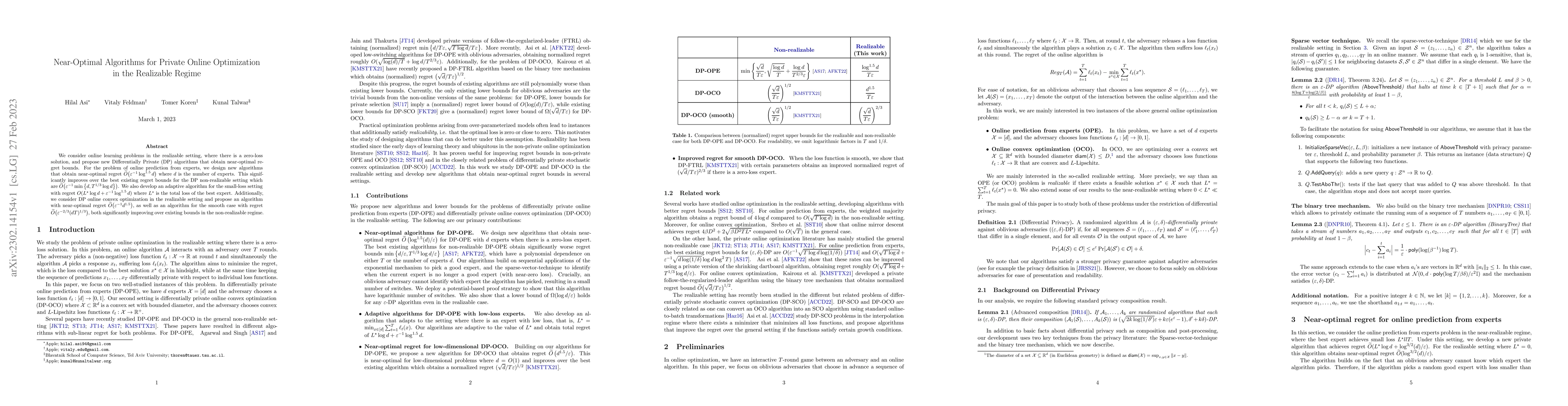

We consider online learning problems in the realizable setting, where there is a zero-loss solution, and propose new Differentially Private (DP) algorithms that obtain near-optimal regret bounds. Fo...

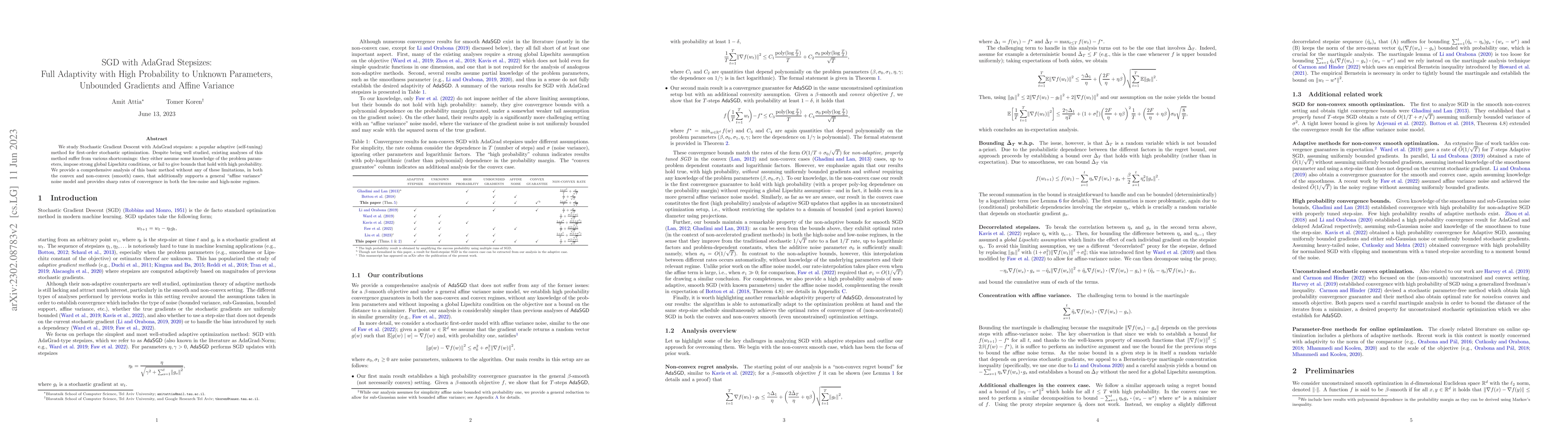

We study Stochastic Gradient Descent with AdaGrad stepsizes: a popular adaptive (self-tuning) method for first-order stochastic optimization. Despite being well studied, existing analyses of this me...

We study reinforcement learning with linear function approximation and adversarially changing cost functions, a setup that has mostly been considered under simplifying assumptions such as full infor...

Online prediction from experts is a fundamental problem in machine learning and several works have studied this problem under privacy constraints. We propose and analyze new algorithms for this prob...

We address the problem of \emph{convex optimization with dueling feedback}, where the goal is to minimize a convex function given a weaker form of \emph{dueling} feedback. Each query consists of two...

An abundance of recent impossibility results establish that regret minimization in Markov games with adversarial opponents is both statistically and computationally intractable. Nevertheless, none o...

We consider the problem of designing uniformly stable first-order optimization algorithms for empirical risk minimization. Uniform stability is often used to obtain generalization error bounds for o...

We study best-of-both-worlds algorithms for bandits with switching cost, recently addressed by Rouyer, Seldin and Cesa-Bianchi, 2021. We introduce a surprisingly simple and effective algorithm that ...

We consider the problem of controlling an unknown linear dynamical system under adversarially changing convex costs and full feedback of both the state and cost function. We present the first comput...

We consider the problem of controlling an unknown linear dynamical system under a stochastic convex cost and full feedback of both the state and cost function. We present a computationally efficient...

An influential line of recent work has focused on the generalization properties of unregularized gradient-based learning procedures applied to separable linear classification with exponentially-tail...

We study to what extent may stochastic gradient descent (SGD) be understood as a "conventional" learning rule that achieves generalization performance by obtaining a good fit to training data. We co...

We study the online learning with feedback graphs framework introduced by Mannor and Shamir (2011), in which the feedback received by the online learner is specified by a graph $G$ over the availabl...

We study the generalization performance of $\text{full-batch}$ optimization algorithms for stochastic convex optimization: these are first-order methods that only access the exact gradient of the em...

We study online convex optimization in the random order model, recently proposed by \citet{garber2020online}, where the loss functions may be chosen by an adversary, but are then presented to the on...

We consider stochastic optimization with delayed gradients where, at each time step $t$, the algorithm makes an update using a stale stochastic gradient from step $t - d_t$ for some arbitrary delay ...

We study the stochastic Multi-Armed Bandit (MAB) problem with random delays in the feedback received by the algorithm. We consider two settings: the reward-dependent delay setting, where realized de...

Stochastic convex optimization over an $\ell_1$-bounded domain is ubiquitous in machine learning applications such as LASSO but remains poorly understood when learning with differential privacy. We ...

We consider the task of learning to control a linear dynamical system under fixed quadratic costs, known as the Linear Quadratic Regulator (LQR) problem. While model-free approaches are often favora...

Neural networks are widespread due to their powerful performance. However, they degrade in the presence of noisy labels at training time. Inspired by the setting of learning with expert advice, wher...

We study a variant of online convex optimization where the player is permitted to switch decisions at most $S$ times in expectation throughout $T$ rounds. Similar problems have been addressed in pri...

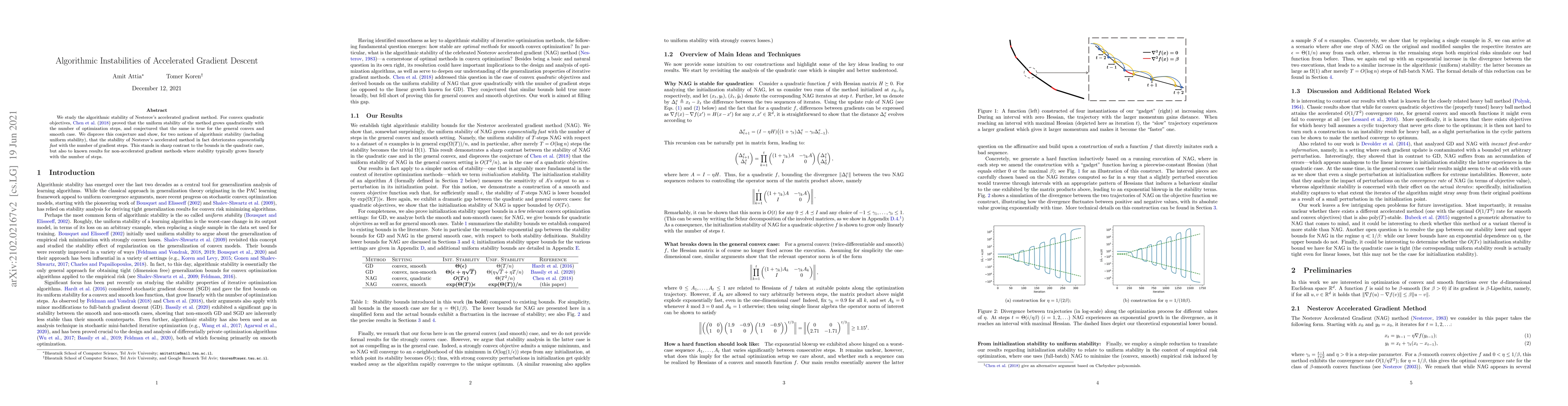

We study the algorithmic stability of Nesterov's accelerated gradient method. For convex quadratic objectives, Chen et al. (2018) proved that the uniform stability of the method grows quadratically ...

We give a new separation result between the generalization performance of stochastic gradient descent (SGD) and of full-batch gradient descent (GD) in the fundamental stochastic convex optimization ...

We study a novel variant of online finite-horizon Markov Decision Processes with adversarially changing loss functions and initially unknown dynamics. In each episode, the learner suffers the loss a...

We introduce the problem of regret minimization in Adversarial Dueling Bandits. As in classic Dueling Bandits, the learner has to repeatedly choose a pair of items and observe only a relative binary...

State-of-the-art optimization is steadily shifting towards massively parallel pipelines with extremely large batch sizes. As a consequence, CPU-bound preprocessing and disk/memory/network operations...

This work presents a new distributed Byzantine tolerant federated learning algorithm, HoldOut SGD, for Stochastic Gradient Descent (SGD) optimization. HoldOut SGD uses the well known machine learnin...

We consider the problem of controlling a known linear dynamical system under stochastic noise, adversarially chosen costs, and bandit feedback. Unlike the full feedback setting where the entire cost...

We study differentially private (DP) algorithms for stochastic convex optimization: the problem of minimizing the population loss given i.i.d. samples from a distribution over convex loss functions....

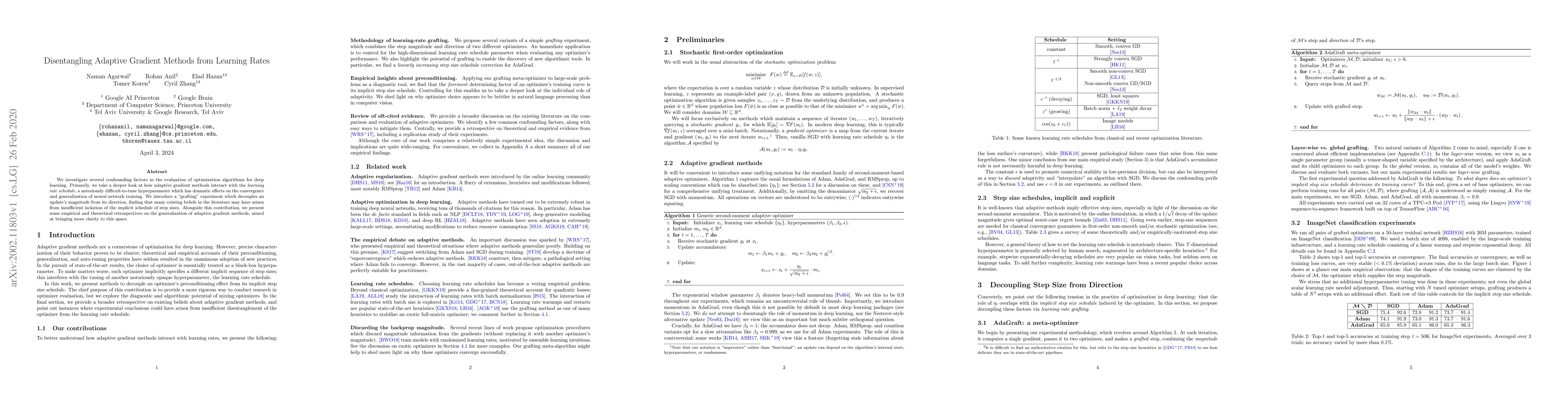

We investigate several confounding factors in the evaluation of optimization algorithms for deep learning. Primarily, we take a deeper look at how adaptive gradient methods interact with the learnin...

We revisit the fundamental problem of prediction with expert advice, in a setting where the environment is benign and generates losses stochastically, but the feedback observed by the learner is sub...

Optimization in machine learning, both theoretical and applied, is presently dominated by first-order gradient methods such as stochastic gradient descent. Second-order optimization methods, that in...

We consider the problem of learning in Linear Quadratic Control systems whose transition parameters are initially unknown. Recent results in this setting have demonstrated efficient learning algorit...

We introduce a temperature into the exponential function and replace the softmax output layer of neural nets by a high temperature generalization. Similarly, the logarithm in the log loss we use for...

We consider convex SGD updates with a block-cyclic structure, i.e. where each cycle consists of a small number of blocks, each with many samples from a possibly different, block-specific, distributi...

Adaptive gradient-based optimizers such as Adagrad and Adam are crucial for achieving state-of-the-art performance in machine translation and language modeling. However, these methods maintain secon...

We consider the problem of asynchronous stochastic optimization, where an optimization algorithm makes updates based on stale stochastic gradients of the objective that are subject to an arbitrary (po...

We study the problem of learning vector-valued linear predictors: these are prediction rules parameterized by a matrix that maps an $m$-dimensional feature vector to a $k$-dimensional target. We focus...

Modern policy optimization methods roughly follow the policy mirror descent (PMD) algorithmic template, for which there are by now numerous theoretical convergence results. However, most of these eith...

We study the problem of multiclass list classification with (semi-)bandit feedback, where input examples are mapped into subsets of size $m$ of a collection of $K$ possible labels, and the feedback co...

The learning rate in stochastic gradient methods is a critical hyperparameter that is notoriously costly to tune via standard grid search, especially for training modern large-scale models with billio...

We study the common continual learning setup where an overparameterized model is sequentially fitted to a set of jointly realizable tasks. We analyze the forgetting, i.e., loss on previously seen task...

We investigate Learning from Label Proportions (LLP), a partial information setting where examples in a training set are grouped into bags, and only aggregate label values in each bag are available. D...

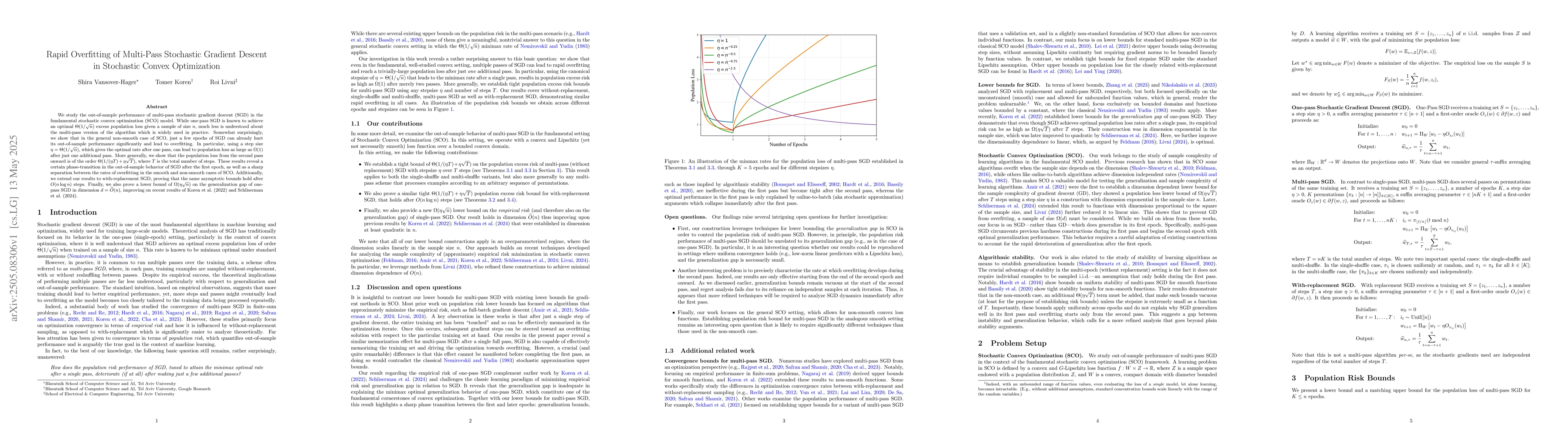

We study the out-of-sample performance of multi-pass stochastic gradient descent (SGD) in the fundamental stochastic convex optimization (SCO) model. While one-pass SGD is known to achieve an optimal ...

We study the generalization performance of unregularized gradient methods for separable linear classification. While previous work mostly deal with the binary case, we focus on the multiclass setting ...

We study realizable continual linear regression under random task orderings, a common setting for developing continual learning theory. In this setup, the worst-case expected loss after $k$ learning i...

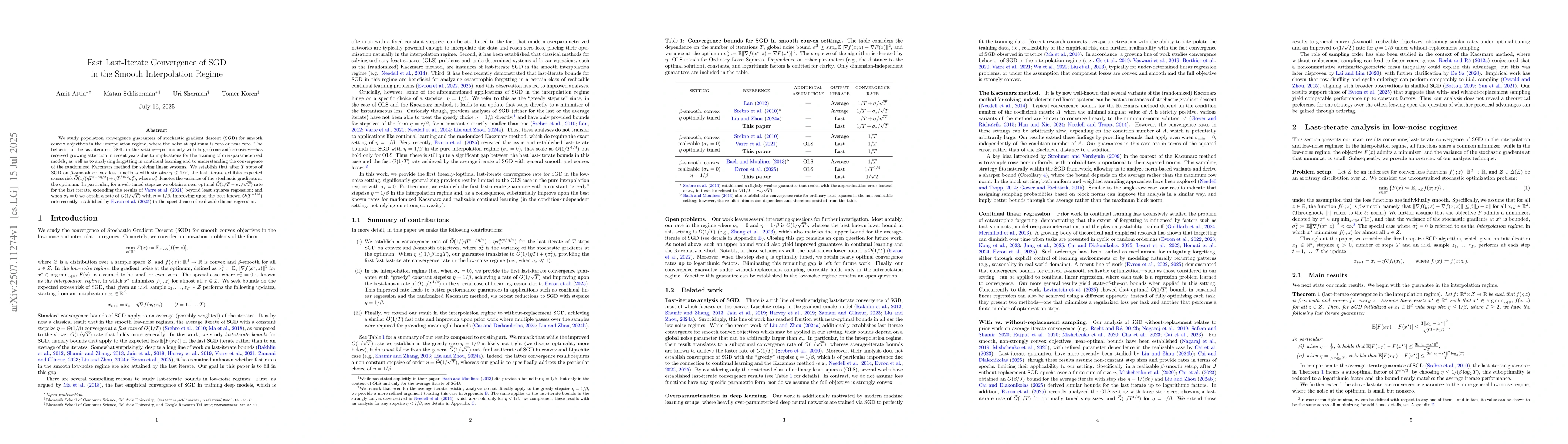

We study population convergence guarantees of stochastic gradient descent (SGD) for smooth convex objectives in the interpolation regime, where the noise at optimum is zero or near zero. The behavior ...

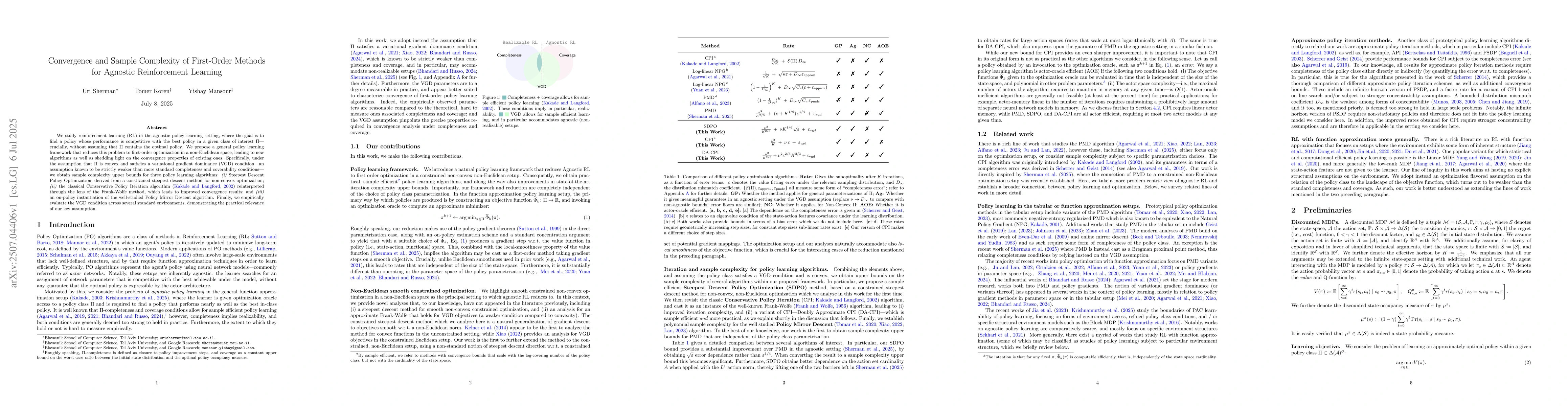

We study reinforcement learning (RL) in the agnostic policy learning setting, where the goal is to find a policy whose performance is competitive with the best policy in a given class of interest $\Pi...

Motivated by problems in online advertising, we address the task of Learning from Label Proportions (LLP). In this partially-supervised setting, training data consists of groups of examples, termed ba...

The fundamental theorem of statistical learning states that binary PAC learning is governed by a single parameter -- the Vapnik-Chervonenkis (VC) dimension -- which determines both learnability and sa...

Online mirror descent (OMD) is a fundamental algorithmic paradigm that underlies many algorithms in optimization, machine learning and sequential decision-making. The OMD iterates are defined as solut...

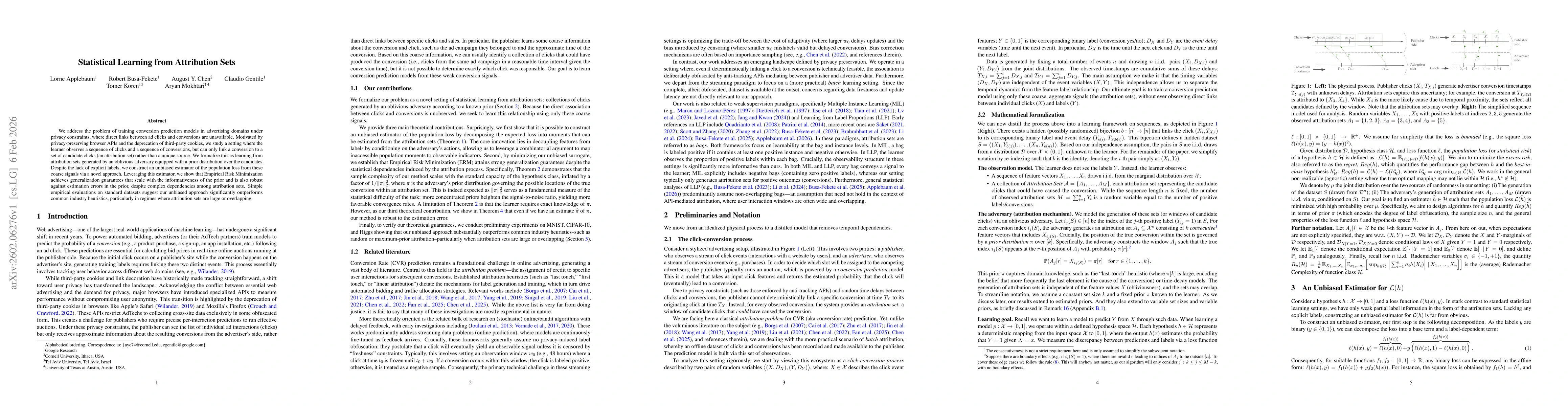

We address the problem of training conversion prediction models in advertising domains under privacy constraints, where direct links between ad clicks and conversions are unavailable. Motivated by pri...

Parameter-free stochastic optimization aims to design algorithms that are agnostic to the underlying problem parameters while still achieving convergence rates competitive with optimally tuned methods...

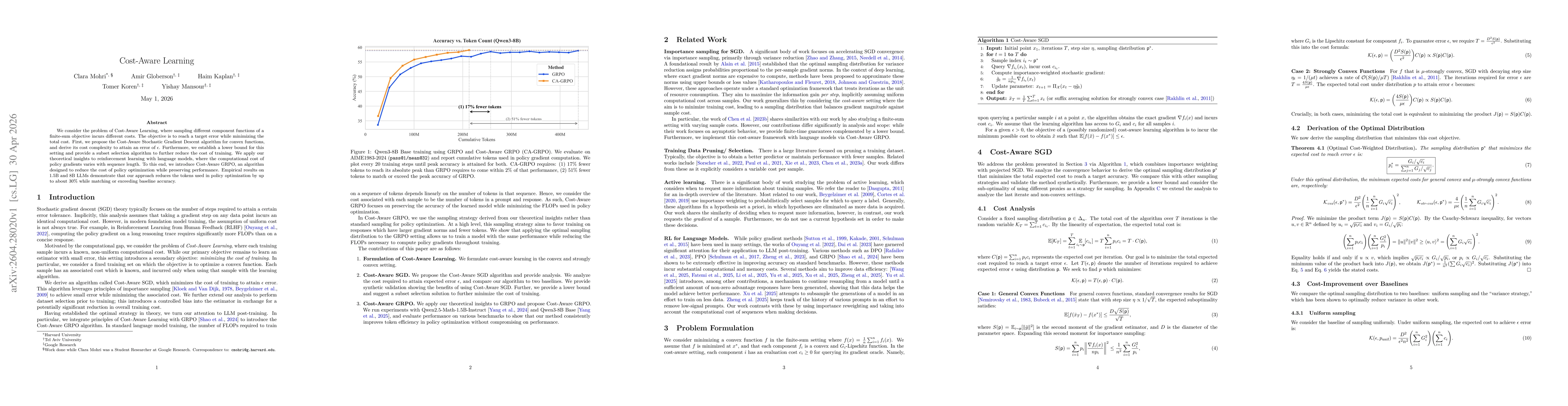

We consider the problem of Cost-Aware Learning, where sampling different component functions of a finite-sum objective incurs different costs. The objective is to reach a target error while minimizing...

Understanding the generalization behavior of learning algorithms is a central goal of learning theory. A recently emerging explanation is that learning algorithms are successful in practice because th...

We study contextual bandits in the stochastic i.i.d.\ setting, where a learner observes contexts drawn from an unknown distribution, selects actions from a finite set $A$, and aims to identify an appr...

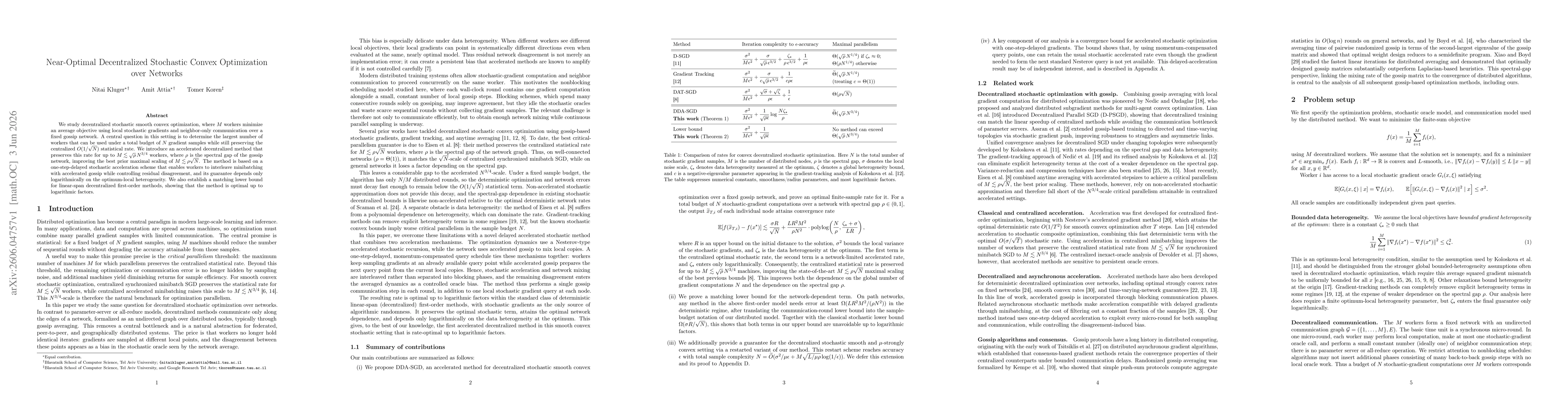

We study decentralized stochastic smooth convex optimization, where $M$ workers minimize an average objective using local stochastic gradients and neighbor-only communication over a fixed gossip netwo...

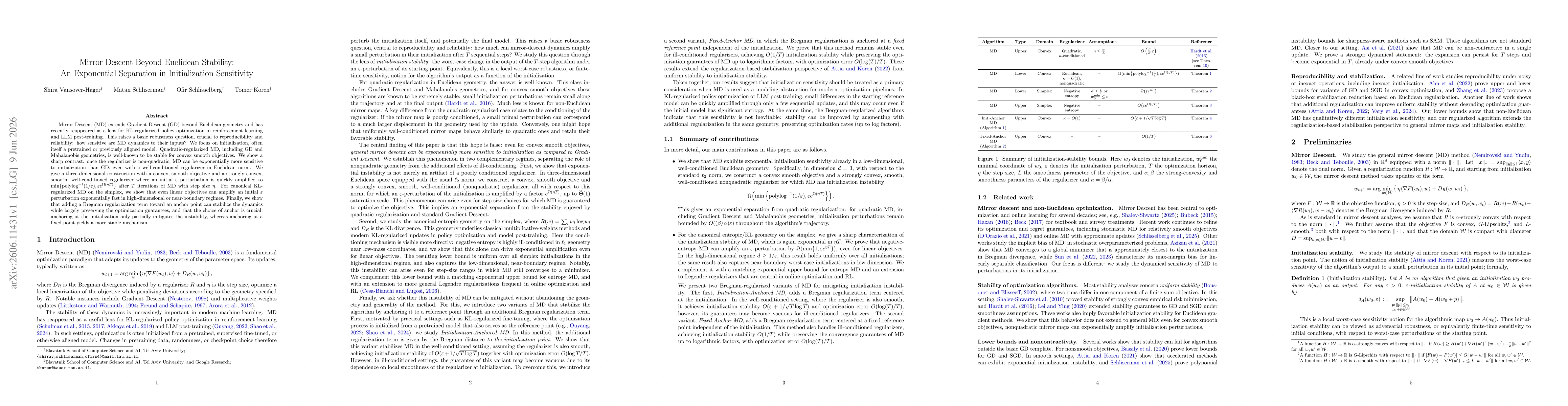

Mirror Descent (MD) extends Gradient Descent (GD) beyond Euclidean geometry and has recently reappeared as a lens for KL-regularized policy optimization in reinforcement learning and LLM post-training...

AdamW is a default optimizer for modern deep learning, but its first and second moment states add roughly two parameter-sized buffers to training memory. We propose Gefen, a memory-efficient optimizer...

While recent advances in co-speech gesture generation have achieved impressive rhythmic synchronization, synthesizing gestures that are both semantically meaningful and faithful to a speaker's unique ...