Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper we analyze the product of bi-dimensional VAR(1) model components. For the introduced time series we derive general formulas for the autocovariance function and study its properties for...

In this paper we study the distribution of a product of two continuous random variables. We derive formulas for the probability density functions and moments of the products of the Gaussian, log-nor...

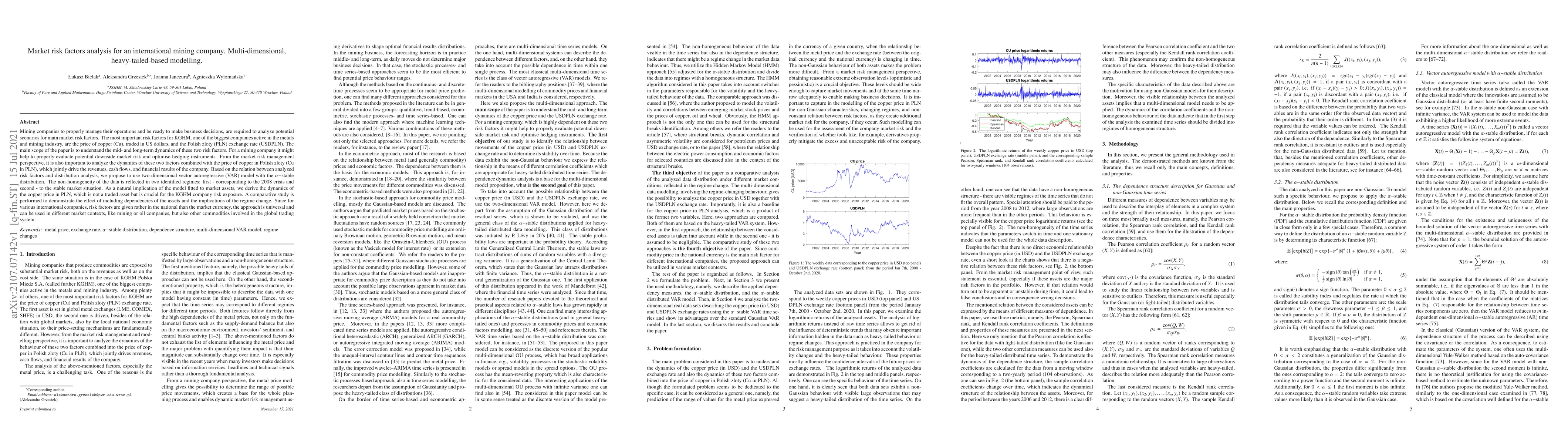

Mining companies to properly manage their operations and be ready to make business decisions, are required to analyze potential scenarios for main market risk factors. The most important risk factor...