Academic Profile

Statistics

Similar Authors

Papers on arXiv

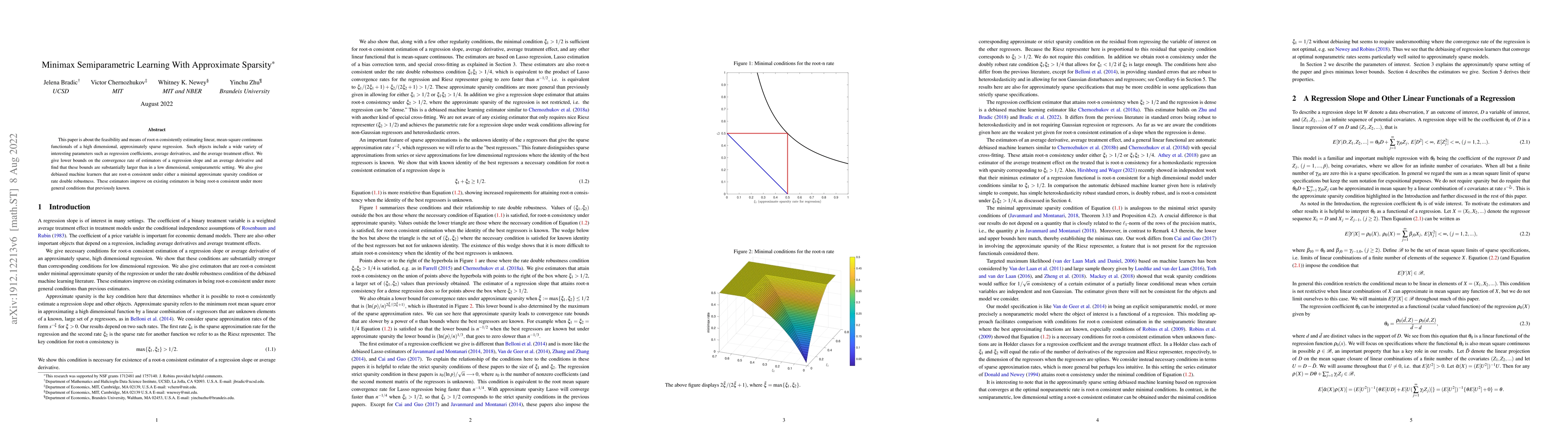

We consider median regression and, more generally, a possibly infinite collection of quantile regressions in high-dimensional sparse models. In these models the overall number of regressors $p$ is v...

In parametric, nonlinear structural models a classical sufficient condition for local identification, like Fisher (1966) and Rothenberg (1971), is that the vector of moment conditions is differentia...

Shape restrictions have played a central role in economics as both testable implications of theory and sufficient conditions for obtaining informative counterfactual predictions. In this paper we pr...

In this paper, we derive non-asymptotic error bounds for the Lasso estimator when the penalty parameter for the estimator is chosen using $K$-fold cross-validation. Our bounds imply that the cross-v...

Many economic and causal parameters depend on nonparametric or high dimensional first steps. We give a general construction of locally robust/orthogonal moment functions for GMM, where moment condit...

Extremal quantile regression, i.e. quantile regression applied to the tails of the conditional distribution, counts with an increasing number of economic and financial applications such as value-at-...

We propose an instrumental variable framework for identifying and estimating average and quantile effects of discrete and continuous treatments with binary instruments. The basis of our approach is ...

An introduction to the emerging fusion of machine learning and causal inference. The book presents ideas from classical structural equation models (SEMs) and their modern AI equivalent, directed acy...

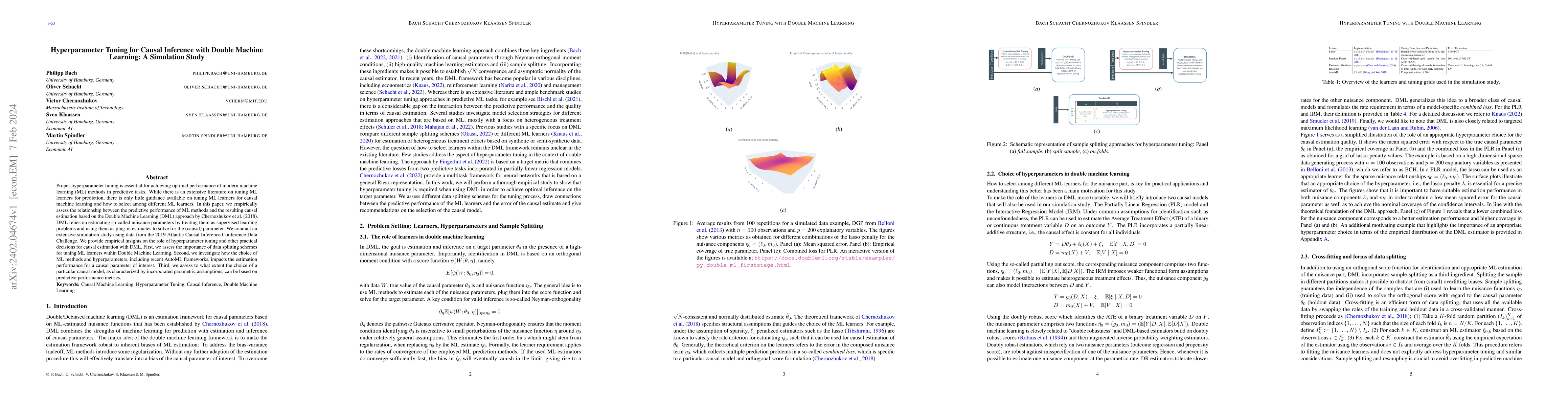

Proper hyperparameter tuning is essential for achieving optimal performance of modern machine learning (ML) methods in predictive tasks. While there is an extensive literature on tuning ML learners ...

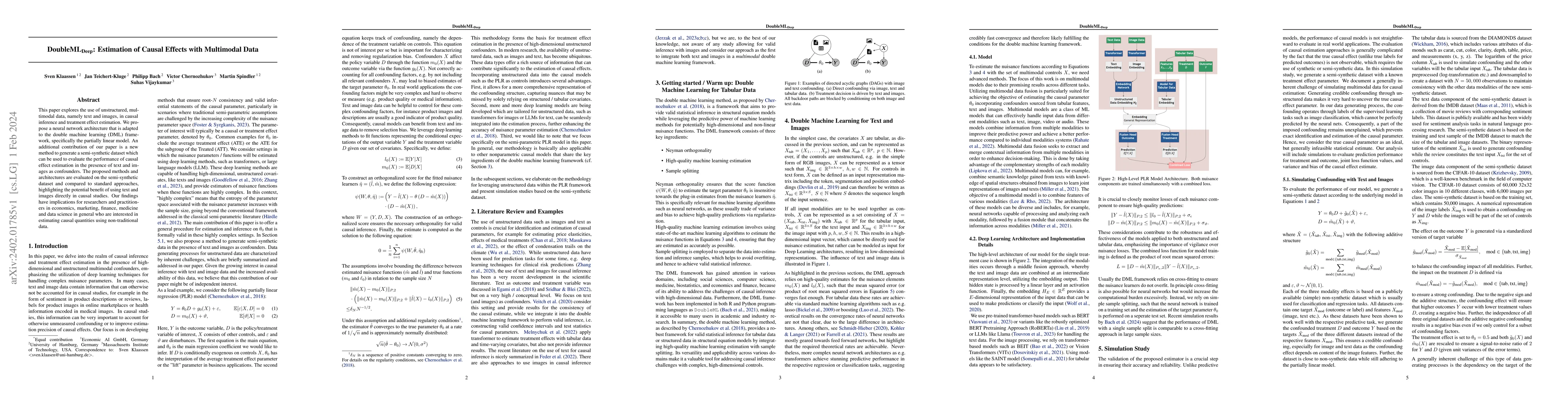

This paper explores the use of unstructured, multimodal data, namely text and images, in causal inference and treatment effect estimation. We propose a neural network architecture that is adapted to...

The Arellano-Bond estimator is a fundamental method for dynamic panel data models, widely used in practice. However, the estimator is severely biased when the data's time series dimension $T$ is lon...

In this paper we address the problem of bias in machine learning of parameters following covariate shifts. Covariate shift occurs when the distribution of input features change between the training ...

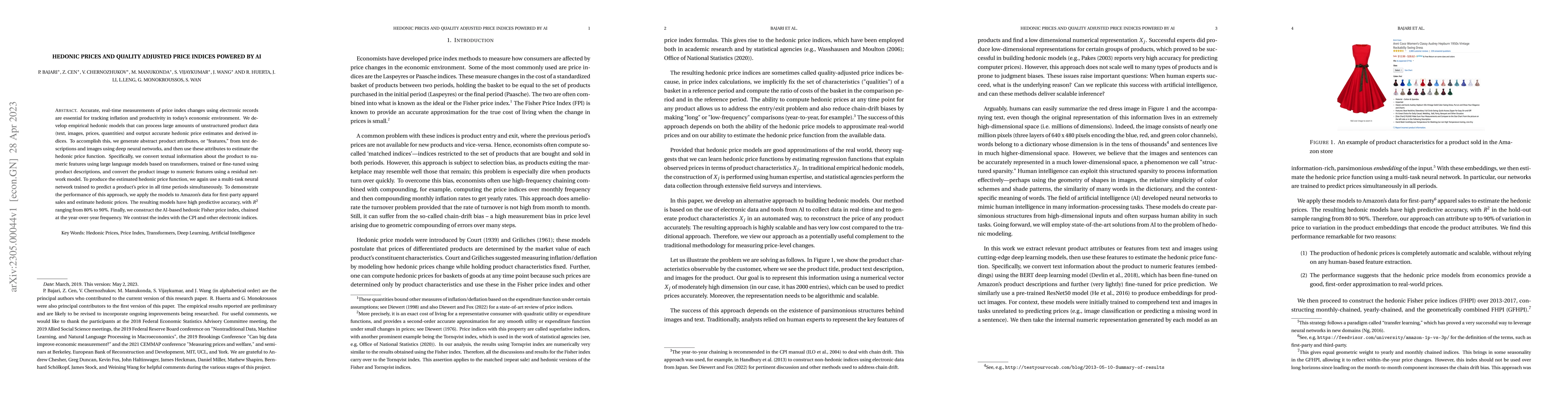

Accurate, real-time measurements of price index changes using electronic records are essential for tracking inflation and productivity in today's economic environment. We develop empirical hedonic m...

This paper studies computationally and theoretically attractive estimators called the Laplace type estimators (LTE), which include means and quantiles of Quasi-posterior distributions defined as tra...

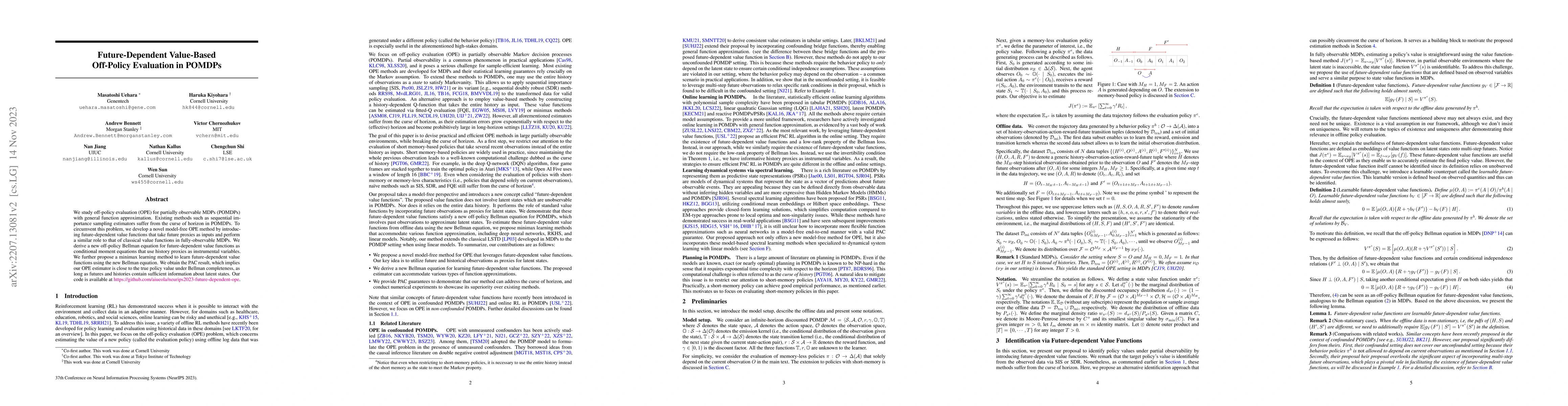

We study off-policy evaluation (OPE) for partially observable MDPs (POMDPs) with general function approximation. Existing methods such as sequential importance sampling estimators and fitted-Q evalu...

This article reviews recent progress in high-dimensional bootstrap. We first review high-dimensional central limit theorems for distributions of sample mean vectors over the rectangles, bootstrap co...

We extend the idea of automated debiased machine learning to the dynamic treatment regime and more generally to nested functionals. We show that the multiply robust formula for the dynamic treatment...

We develop a general theory of omitted variable bias for a wide range of common causal parameters, including (but not limited to) averages of potential outcomes, average treatment effects, average c...

Recently, Phillippe Lemoine posted a critique of our paper "Causal Impact of Masks, Policies, Behavior on Early Covid-19 Pandemic in the U.S." [arXiv:2005.14168] at his post titled "Lockdowns, econo...

Many causal and policy effects of interest are defined by linear functionals of high-dimensional or non-parametric regression functions. $\sqrt{n}$-consistent and asymptotically normal estimation of...

This paper studies inference in linear models with a high-dimensional parameter matrix that can be well-approximated by a ``spiked low-rank matrix.'' A spiked low-rank matrix has rank that grows slo...

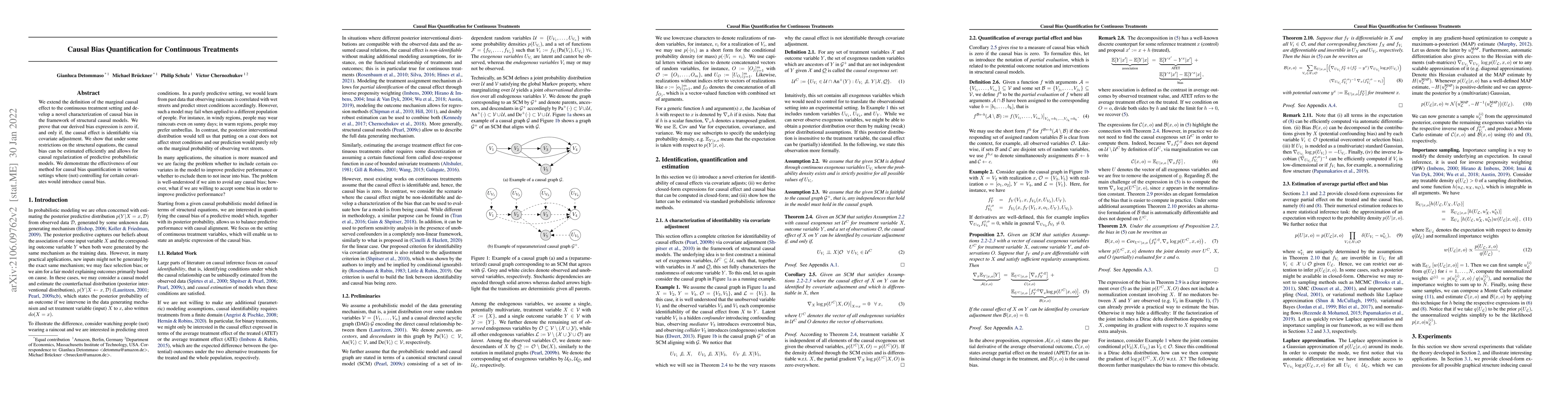

We extend the definition of the marginal causal effect to the continuous treatment setting and develop a novel characterization of causal bias in the framework of structural causal models. We prove ...

Debiased machine learning is a meta algorithm based on bias correction and sample splitting to calculate confidence intervals for functionals, i.e. scalar summaries, of machine learning algorithms. ...

We propose employing a debiased-regularized, high-dimensional generalized method of moments (GMM) framework to perform inference on large-scale spatial panel networks. In particular, network structu...

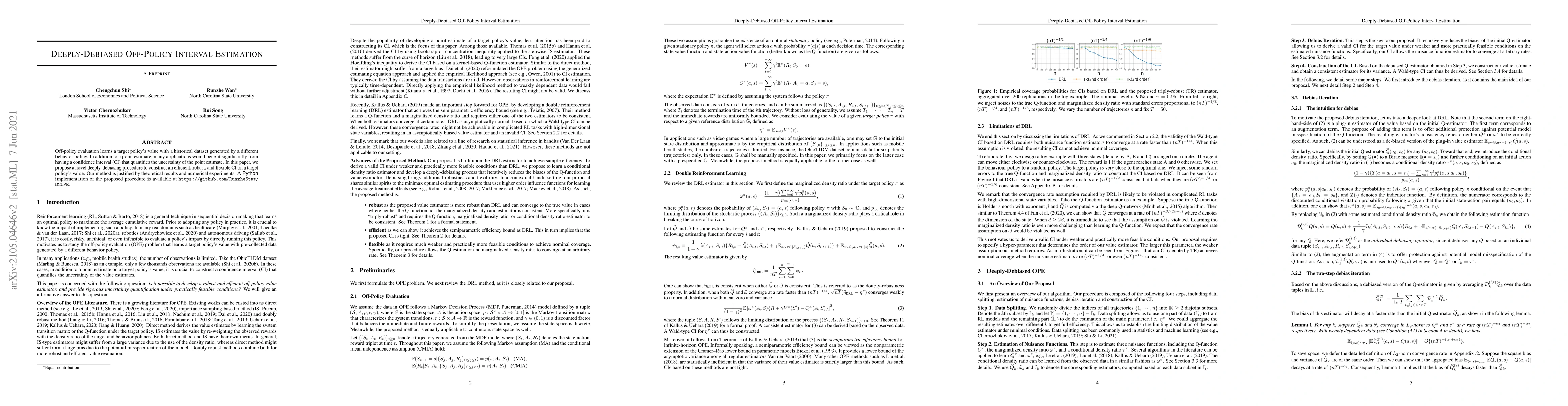

Off-policy evaluation learns a target policy's value with a historical dataset generated by a different behavior policy. In addition to a point estimate, many applications would benefit significantl...

A variety of interesting parameters may depend on high dimensional regressions. Machine learning can be used to estimate such parameters. However estimators based on machine learners can be severely...

DoubleML is an open-source Python library implementing the double machine learning framework of Chernozhukov et al. (2018) for a variety of causal models. It contains functionalities for valid stati...

The R package DoubleML implements the double/debiased machine learning framework of Chernozhukov et al. (2018). It provides functionalities to estimate parameters in causal models based on machine l...

In this paper, we first revisit the Koenker and Bassett variational approach to (univariate) quantile regression, emphasizing its link with latent factor representations and correlation maximization...

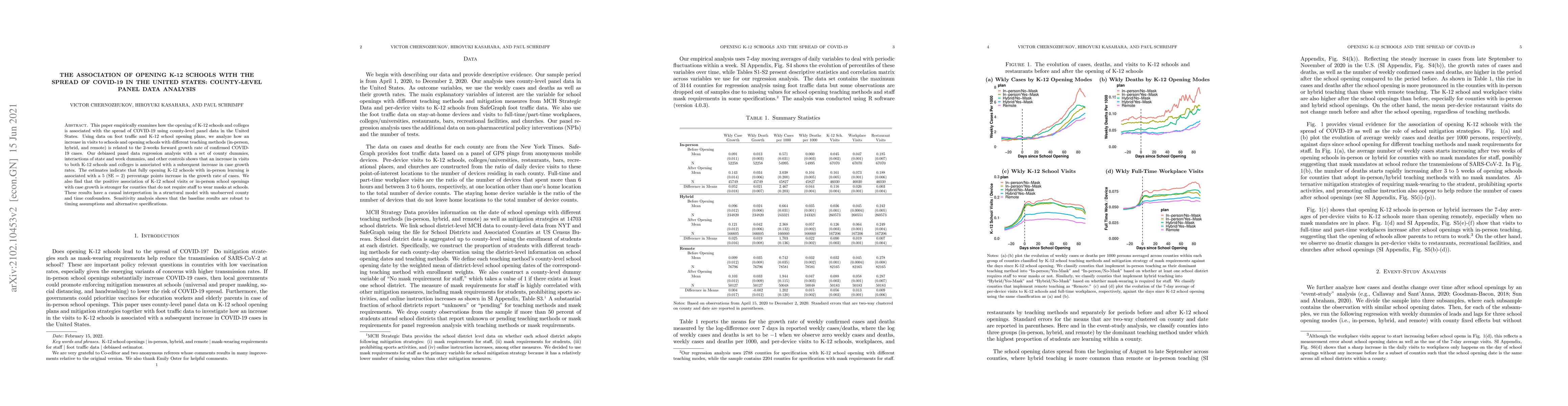

This paper empirically examines how the opening of K-12 schools and colleges is associated with the spread of COVID-19 using county-level panel data in the United States. Using data on foot traffic ...

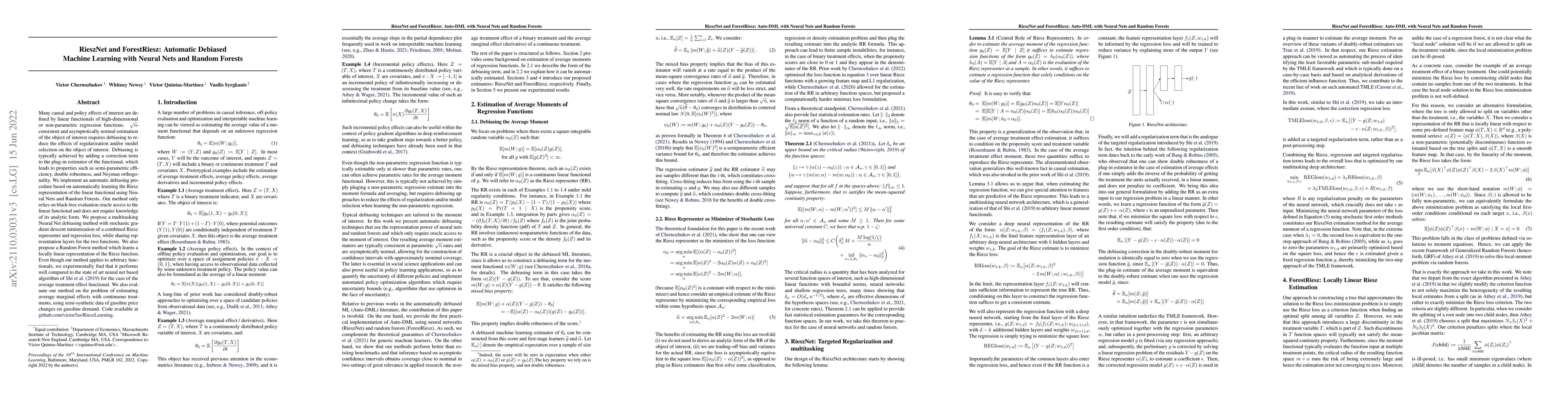

Many causal parameters are linear functionals of an underlying regression. The Riesz representer is a key component in the asymptotic variance of a semiparametrically estimated linear functional. We...

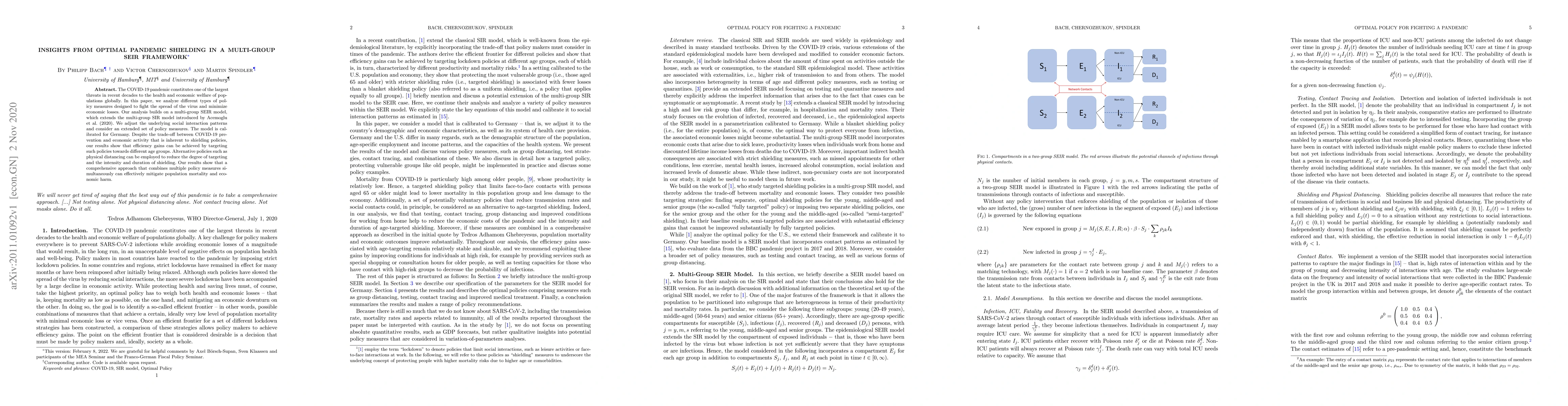

The COVID-19 pandemic constitutes one of the largest threats in recent decades to the health and economic welfare of populations globally. In this paper, we analyze different types of policy measure...

This chapter reviews the instrumental variable quantile regression model of Chernozhukov and Hansen (2005). We discuss the key conditions used for identification of structural quantile effects withi...

This paper is about the feasibility and means of root-n consistently estimating linear, mean-square continuous functionals of a high dimensional, approximately sparse regression. Such objects includ...

This paper deals with the Gaussian and bootstrap approximations to the distribution of the max statistic in high dimensions. This statistic takes the form of the maximum over components of the sum o...

We propose a robust method for constructing conditionally valid prediction intervals based on models for conditional distributions such as quantile and distribution regression. Our approach can be a...

The widespread use of quantile regression methods depends crucially on the existence of fast algorithms. Despite numerous algorithmic improvements, the computation time is still non-negligible becau...

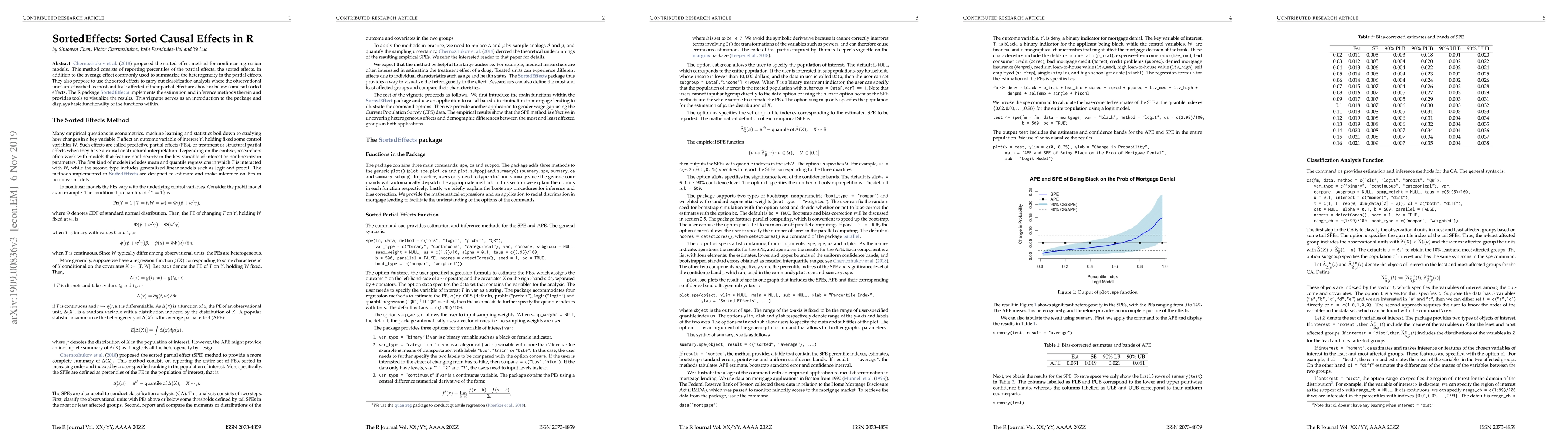

Chernozhukov et al. (2018) proposed the sorted effect method for nonlinear regression models. This method consists of reporting percentiles of the partial effects in addition to the average commonly...

We consider off-policy evaluation and optimization with continuous action spaces. We focus on observational data where the data collection policy is unknown and needs to be estimated. We take a semi...

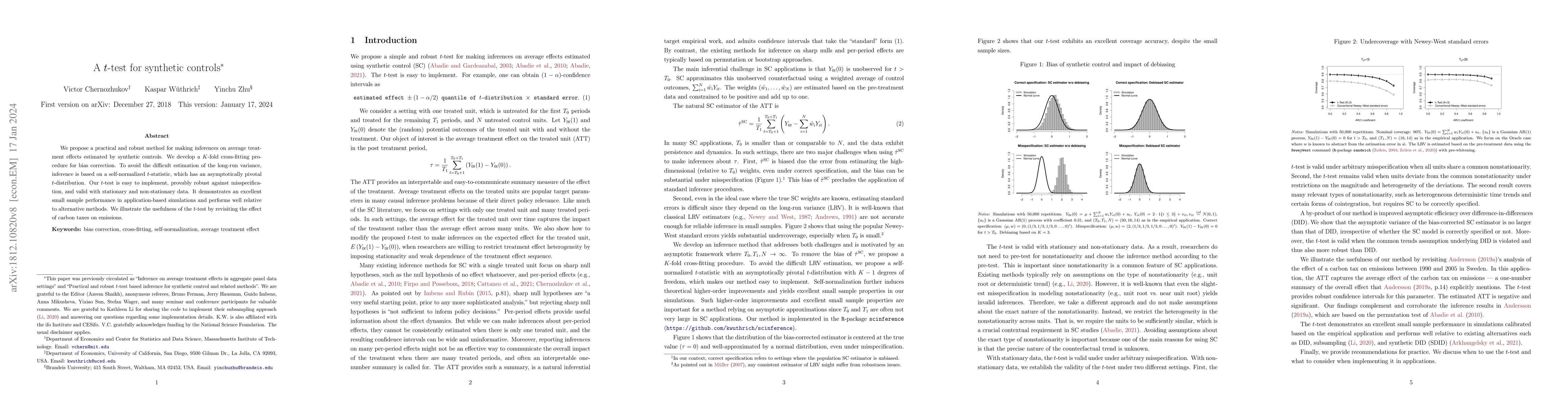

We propose a practical and robust method for making inferences on average treatment effects estimated by synthetic controls. We develop a $K$-fold cross-fitting procedure for bias correction. To avo...

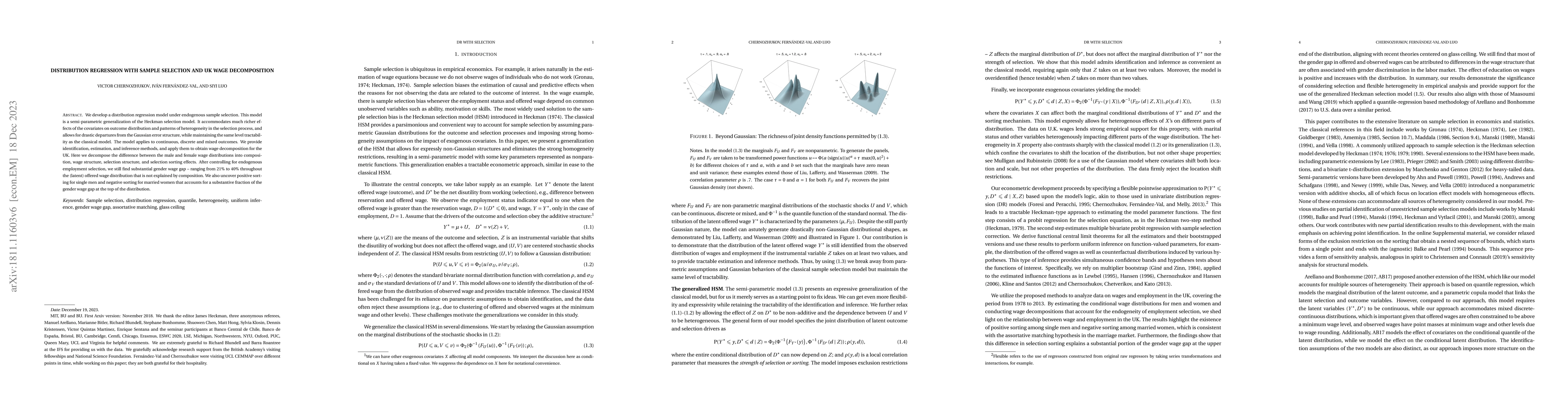

We develop a distribution regression model under endogenous sample selection. This model is a semi-parametric generalization of the Heckman selection model. It accommodates much richer effects of th...

Many causal and structural effects depend on regressions. Examples include policy effects, average derivatives, regression decompositions, average treatment effects, causal mediation, and parameters...

A common problem in econometrics, statistics, and machine learning is to estimate and make inference on functions that satisfy shape restrictions. For example, distribution functions are nondecreasi...

We consider the estimation and inference in a system of high-dimensional regression equations allowing for temporal and cross-sectional dependency in covariates and error processes, covering rather ...

This paper provides a method to construct simultaneous confidence bands for quantile functions and quantile effects in nonlinear network and panel models with unobserved two-way effects, strictly ex...

We provide adaptive inference methods, based on $\ell_1$ regularization, for regular (semi-parametric) and non-regular (nonparametric) linear functionals of the conditional expectation function. Exa...

Many applications involve a censored dependent variable and an endogenous independent variable. Chernozhukov et al. (2015) introduced a censored quantile instrumental variable estimator (CQIV) for u...

This paper provides estimation and inference methods for a conditional average treatment effects (CATE) characterized by a high-dimensional parameter in both homogeneous cross-sectional and unit-het...

We introduce new inference procedures for counterfactual and synthetic control methods for policy evaluation. We recast the causal inference problem as a counterfactual prediction and a structural b...

We propose strategies to estimate and make inference on key features of heterogeneous effects in randomized experiments. These key features include best linear predictors of the effects using machin...

This paper proposes the automatic Doubly Robust Random Forest (DRRF) algorithm for estimating the conditional expectation of a moment functional in the presence of high-dimensional nuisance functions....

Rank-rank regressions are widely used in economic research to evaluate phenomena such as intergenerational income persistence or mobility. However, when covariates are incorporated to capture between-...

There are many nonparametric objects of interest that are a function of a conditional distribution. One important example is an average treatment effect conditional on a subset of covariates. Many of ...

This paper advances empirical demand analysis by integrating multimodal product representations derived from artificial intelligence (AI). Using a detailed dataset of toy cars on \textit{Amazon.com}, ...

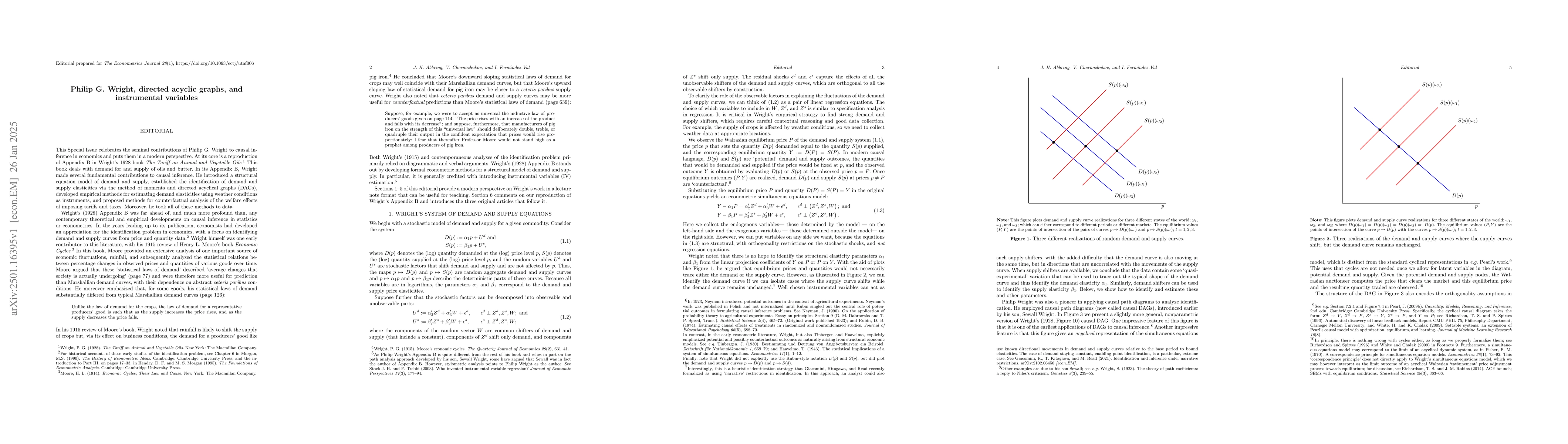

Wright (1928) deals with demand and supply of oils and butter. In Appendix B of this book, Philip Wright made several fundamental contributions to causal inference. He introduced a structural equation...

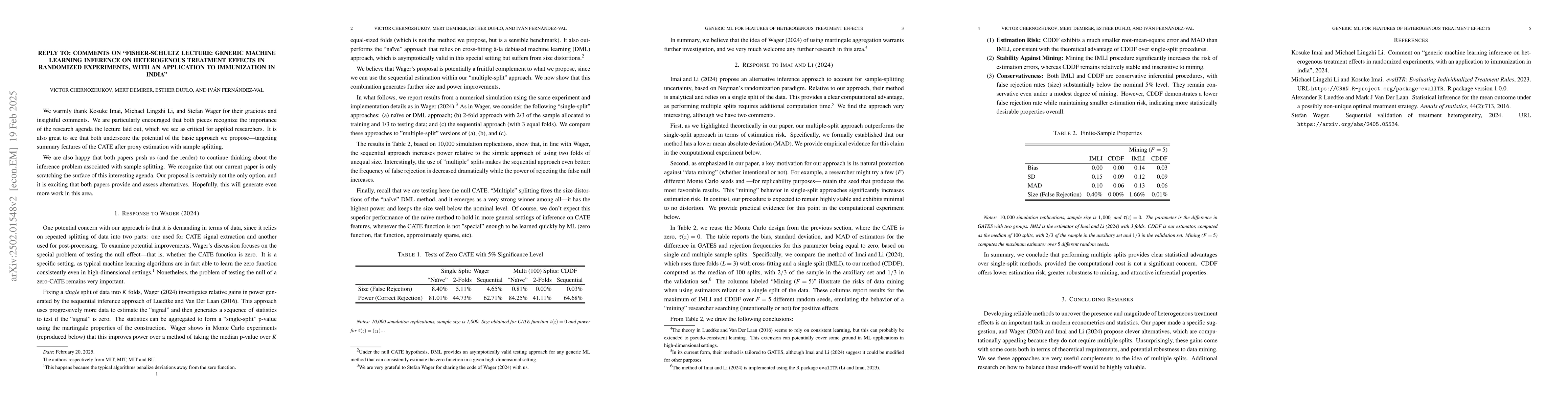

We warmly thank Kosuke Imai, Michael Lingzhi Li, and Stefan Wager for their gracious and insightful comments. We are particularly encouraged that both pieces recognize the importance of the research a...

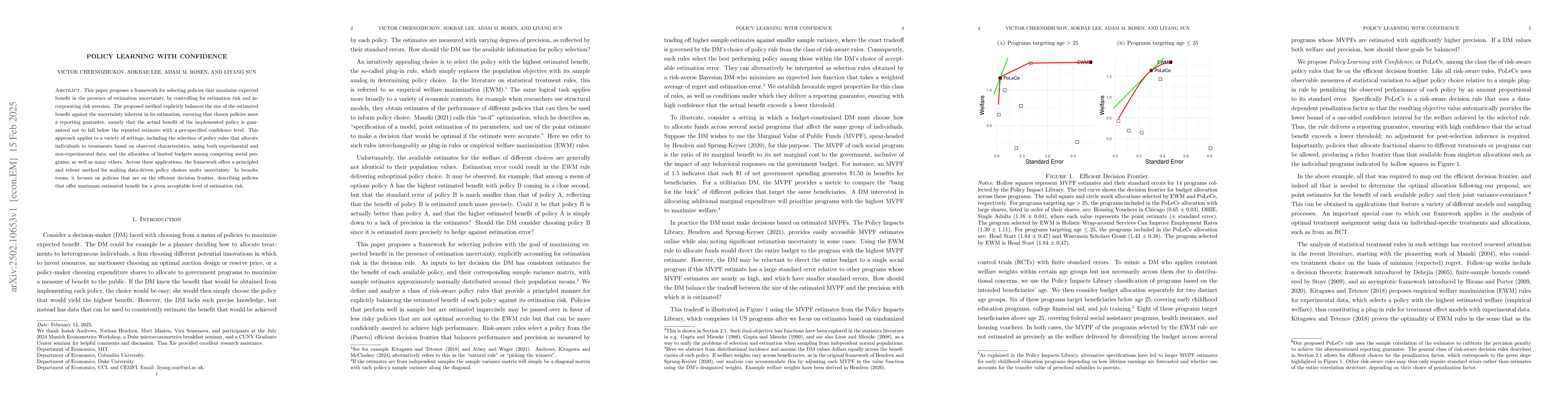

This paper proposes a framework for selecting policies that maximize expected benefit in the presence of estimation uncertainty, by controlling for estimation risk and incorporating risk aversion. The...

This paper provides a practical introduction to Double/Debiased Machine Learning (DML). DML provides a general approach to performing inference about a target parameter in the presence of nuisance par...

Structural estimation in economics often makes use of models formulated in terms of moment conditions. While these moment conditions are generally well-motivated, it is often unknown whether the momen...

We employ distribution regression (DR) to estimate the joint distribution of two outcome variables conditional on chosen covariates. While Bivariate Distribution Regression (BDR) is useful in a variet...

Causal Machine Learning has emerged as a powerful tool for flexibly estimating causal effects from observational data in both industry and academia. However, causal inference from observational data r...

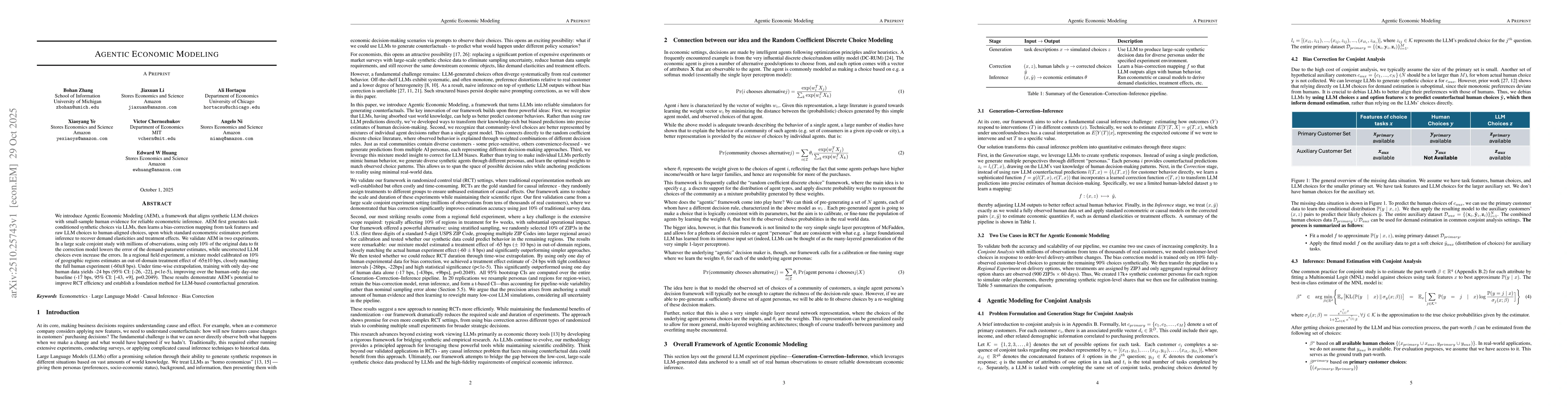

We introduce Agentic Economic Modeling (AEM), a framework that aligns synthetic LLM choices with small-sample human evidence for reliable econometric inference. AEM first generates task-conditioned sy...

In this paper, we extend the Riesz representation framework to causal inference under sample selection, where both treatment assignment and outcome observability are non-random. Formulating the proble...