Academic Profile

Statistics

Similar Authors

Papers on arXiv

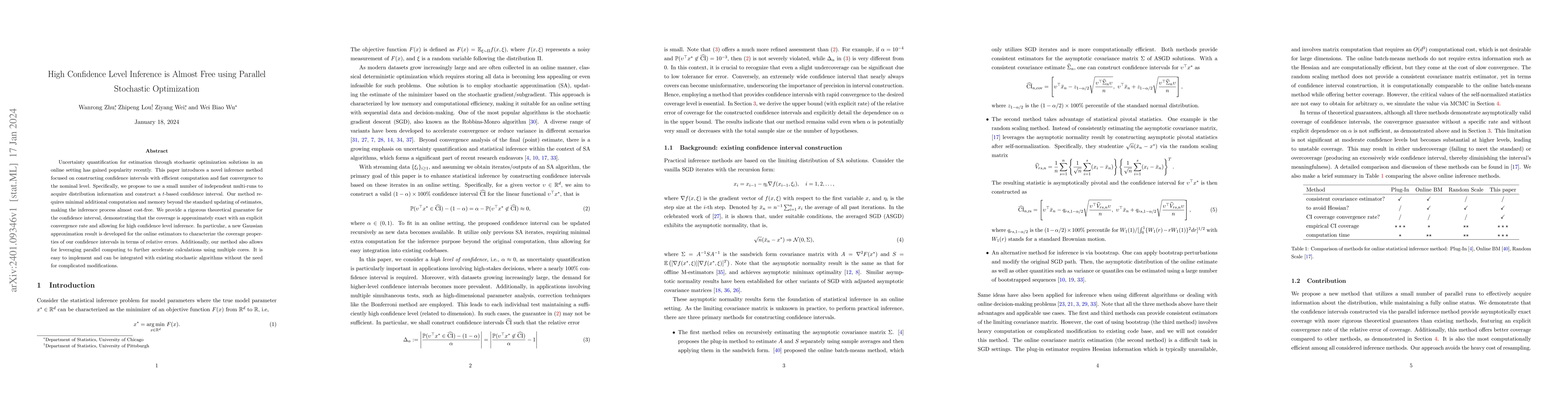

Uncertainty quantification for estimation through stochastic optimization solutions in an online setting has gained popularity recently. This paper introduces a novel inference method focused on con...

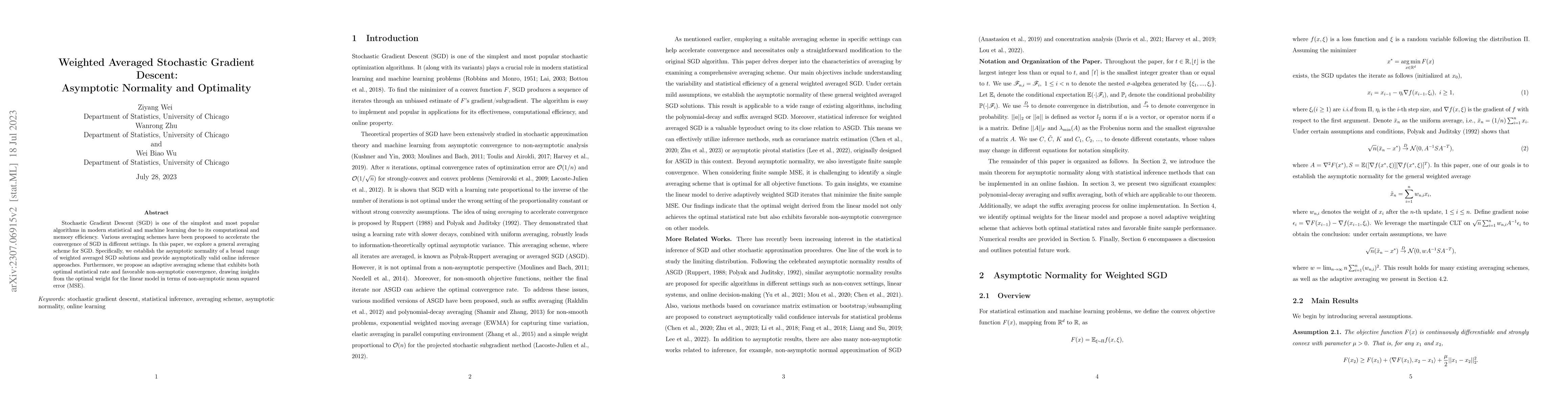

Stochastic Gradient Descent (SGD) is one of the simplest and most popular algorithms in modern statistical and machine learning due to its computational and memory efficiency. Various averaging sche...

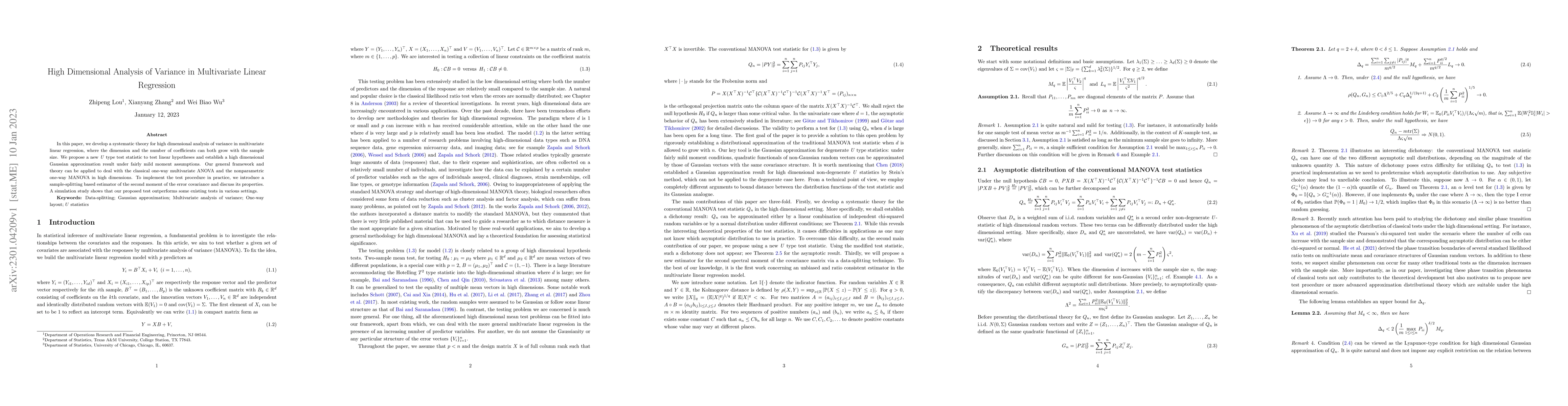

In this paper, we develop a systematic theory for high dimensional analysis of variance in multivariate linear regression, where the dimension and the number of coefficients can both grow with the s...

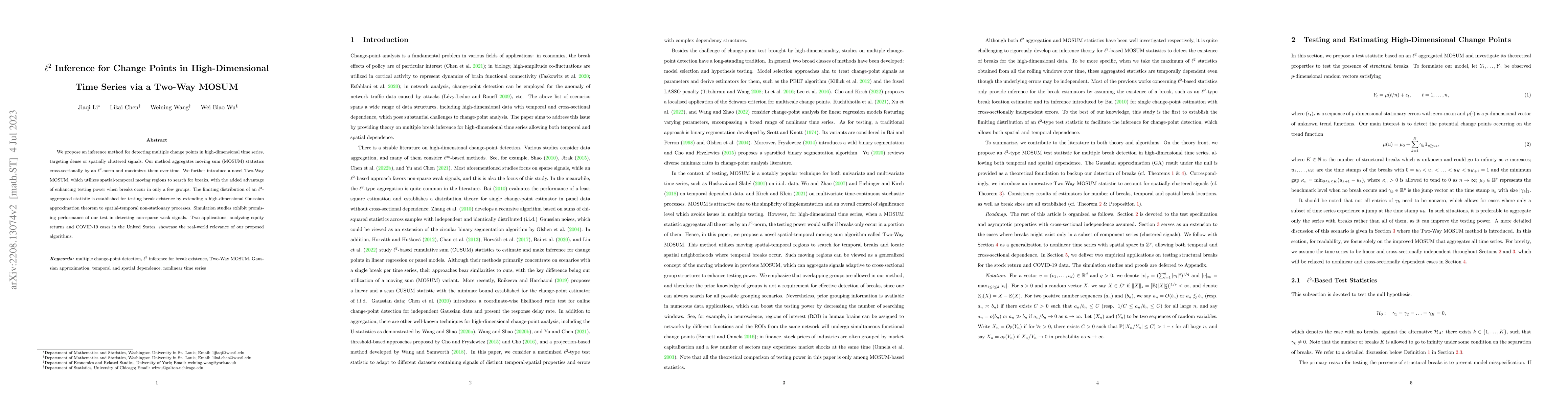

We propose an inference method for detecting multiple change points in high-dimensional time series, targeting dense or spatially clustered signals. Our method aggregates moving sum (MOSUM) statisti...

After obtaining an accurate approximation for $ARL_0$, we first consider the optimal design of weight parameter for a multivariate EWMA chart that minimizes the stationary average delay detection ti...

In this paper, we consider a wide class of time-varying multivariate causal processes which nests many classic and new examples as special cases. We first prove the existence of a weakly dependent s...

We propose a change-point detection method for large scale multiple testing problems with data having clustered signals. Unlike the classic change-point setup, the signals can vary in size within a ...

Accurate forecasting is one of the fundamental focus in the literature of econometric time-series. Often practitioners and policy makers want to predict outcomes of an entire time horizon in the fut...

A general class of time-varying regression models is considered in this paper. We estimate the regression coefficients by using local linear M-estimation. For these estimators, weak Bahadur represen...

Given a weakly dependent stationary process, we describe the transition between a Berry-Esseen bound and a second order Edgeworth expansion in terms of the Berry-Esseen characteristic. This characte...

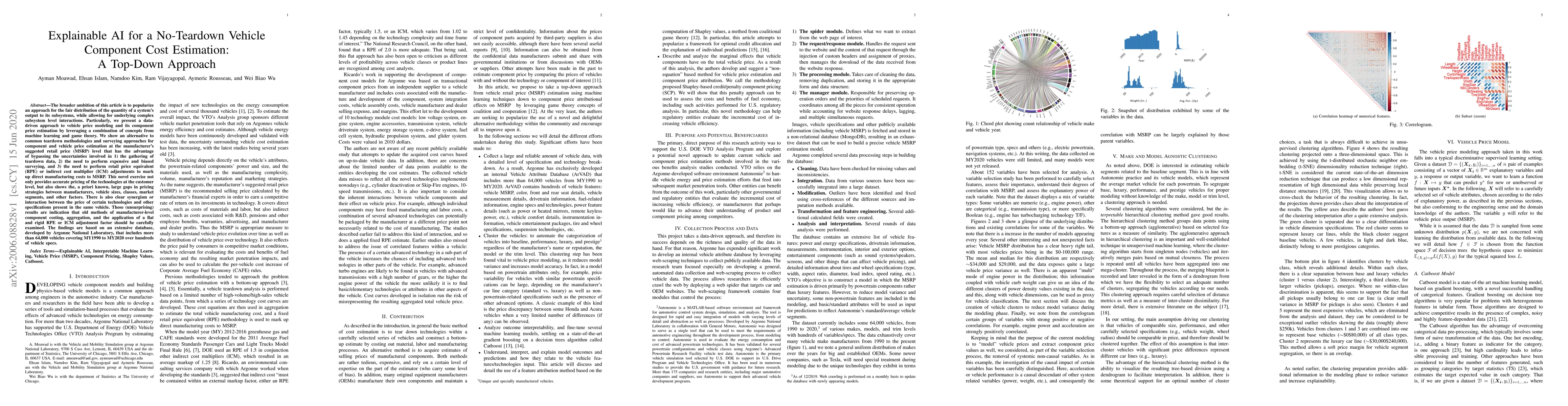

The broader ambition of this article is to popularize an approach for the fair distribution of the quantity of a system's output to its subsystems, while allowing for underlying complex subsystem le...

We construct long-term prediction intervals for time-aggregated future values of univariate economic time series. We propose computational adjustments of the existing methods to improve coverage pro...

The stochastic gradient descent (SGD) algorithm is widely used for parameter estimation, especially for huge data sets and online learning. While this recursive algorithm is popular for computation ...

We obtain an optimal bound for a Gaussian approximation of a large class of vector-valued random processes. Our results provide a substantial generalization of earlier results that assume independen...

This paper proposes an asymptotic theory for online inference of the stochastic gradient descent (SGD) iterates with dropout regularization in linear regression. Specifically, we establish the geometr...

This paper considers the problem of testing and estimation of change point where signals after the change point can be highly irregular, which departs from the existing literature that assumes signals...

Statistical inference for time series such as curve estimation for time-varying models or testing for existence of change-point have garnered significant attention. However, these works are generally ...

This paper proposes an online inference method of the stochastic gradient descent (SGD) with a constant learning rate for quantile loss functions with theoretical guarantees. Since the quantile loss f...

Constrained stochastic nonlinear optimization problems have attracted significant attention for their ability to model complex real-world scenarios in physics, economics, and biology. As datasets cont...

This paper considers the estimation of quantiles via a smoothed version of the stochastic gradient descent (SGD) algorithm. By smoothing the score function in the conventional SGD quantile algorithm, ...

Federated Learning has gained traction in privacy-sensitive collaborative environments, with local SGD emerging as a key optimization method in decentralized settings. While its convergence properties...

This study evaluates three probabilistic forecasting strategies using LightGBM: global pooling, cluster-level pooling, and station-level modeling across a range of scenarios, from fully homogeneous si...

Seismic data contain complex temporal information that arrives at high speed and has a large, even potentially unbounded volume. The explosion of temporally correlated streaming data from advanced sei...

Stochastic Gradient Descent (SGD) and its Ruppert-Polyak averaged variant (ASGD) lie at the heart of modern large-scale learning, yet their theoretical properties in high-dimensional settings are rare...

High-dimensional vector autoregressive (VAR) models have numerous applications in fields such as econometrics, biology, climatology, among others. While prior research has mainly focused on linear VAR...

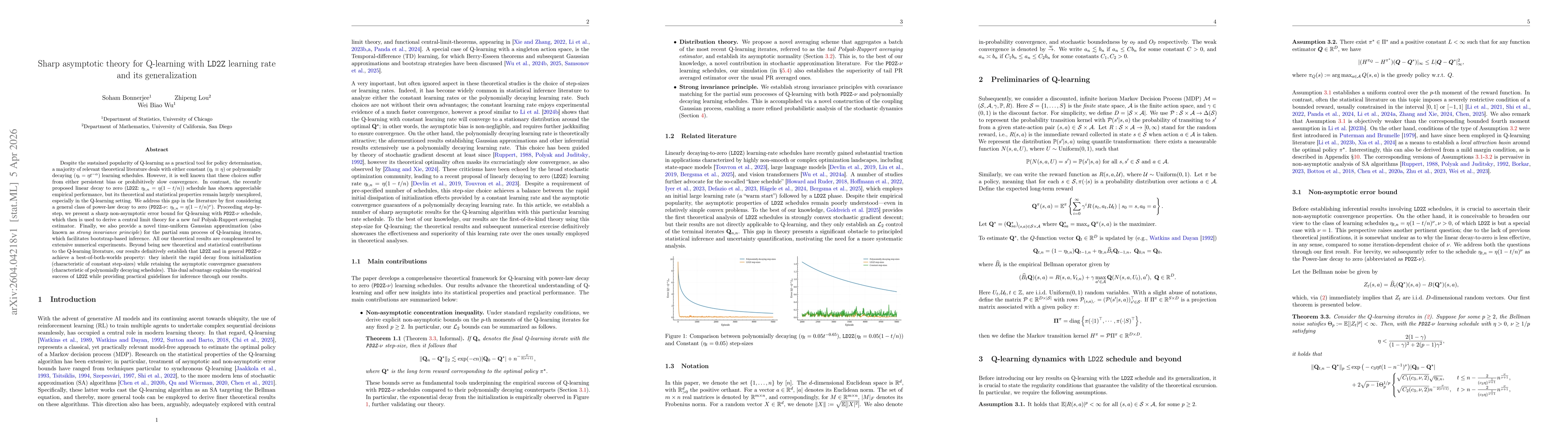

Despite the sustained popularity of Q-learning as a practical tool for policy determination, a majority of relevant theoretical literature deals with either constant ($η_{t}\equiv η$) or polynomially ...

For time series with long-range temporal dependence, inference for covariance and precision matrices is non-trivial. We propose a Berry-Esseen type Gaussian approximation result that gives a finite-sa...

We study online inference and asymptotic covariance estimation for the stochastic gradient descent (SGD) algorithm. While classical methods (such as plug-in and batch-means estimators) are available, ...

While algorithmic stability is a central tool for understanding generalization of learning algorithms, existing high-probability guarantees typically rely on uniform boundedness or sub-Gaussian/sub-We...