Academic Profile

Statistics

Similar Authors

Papers on arXiv

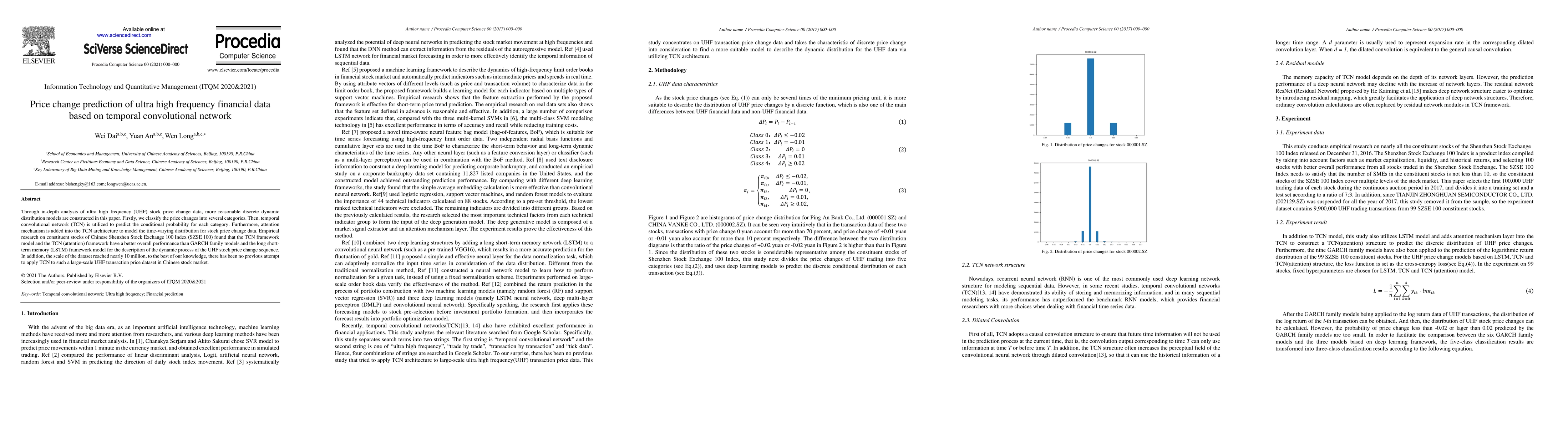

Through in-depth analysis of ultra high frequency (UHF) stock price change data, more reasonable discrete dynamic distribution models are constructed in this paper. Firstly, we classify the price ch...

The Gaussian Process with a deep kernel is an extension of the classic GP regression model and this extended model usually constructs a new kernel function by deploying deep learning techniques like...

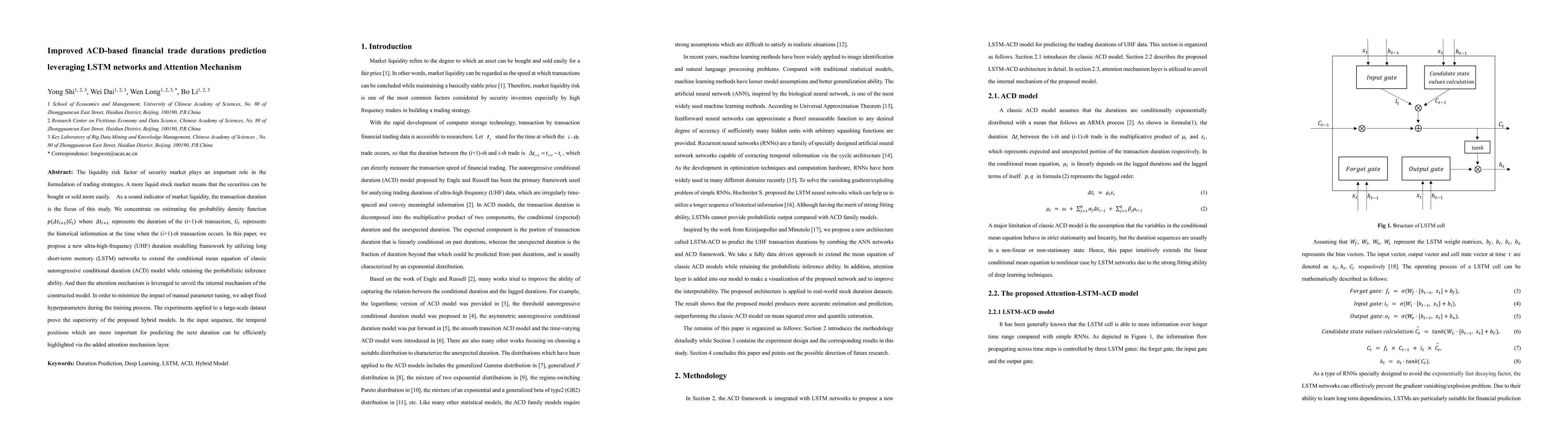

The liquidity risk factor of security market plays an important role in the formulation of trading strategies. A more liquid stock market means that the securities can be bought or sold more easily....

There are various types of pyramid schemes which have inflicted or are inflicting losses on many people in the world. We propose a pyramid scheme model which has the principal characters of many pyr...

AIOps algorithms play a crucial role in the maintenance of microservice systems. Many previous benchmarks' performance leaderboard provides valuable guidance for selecting appropriate algorithms. Howe...