Statistics

Similar Authors

Papers on arXiv

An option market maker incurs funding costs when carrying and hedging inventory. To hedge a net long delta inventory, for example, she pays a fee to borrow stock from the securities lending market. ...

This article presents FVA and CVA of a bilateral derivative in a coherent manner, based on recent developments in fair value accounting and ISDA standards. We argue that a derivative liability, afte...

This article prices OTC derivatives with either an exogenously determined initial margin profile or endogenously approximated initial margin. In the former case, margin valuation adjustment (MVA) is...

An uncollateralized swap hedged back-to-back by a CCP swap is used to introduce FVA. The open IR01 of FVA, however, is a sure sign of risk not being fully hedged, a theoretical no-arbitrage pricing ...

A repurchase agreement lets investors borrow cash to buy securities. Financier only lends to securities' market value after a haircut and charges interest. Repo pricing is characterized with its puz...

Securities borrowing and lending are critical to proper functioning of securities markets. To alleviate securities owners' exposure to borrower default risk, overcollateralization and indemnificatio...

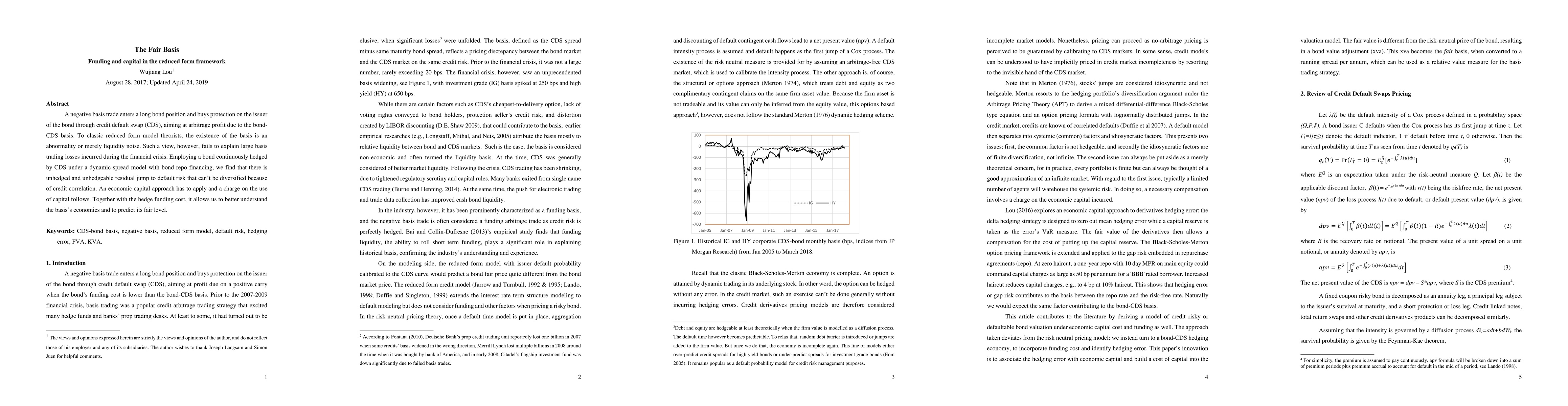

Derivative pricing is about cash flow discounting at the riskfree rate. This teaching has lost its meaning post the financial crisis, due to the addition of extra value adjustments (XVA), which also...

A negative basis trade enters a long bond position and buys protection on the issuer of the bond through credit default swap (CDS), aiming at arbitrage profit due to the bond-CDS basis. To classic r...

Haircutting non-cash collateral has become a key element of the post-crisis reform of the shadow banking system and OTC derivatives markets. This article develops a parametric haircut model by expan...