Academic Profile

Statistics

Similar Authors

Papers on arXiv

For refracted spectrally negative L\'evy processes, we identify expressions of several quantities related to Laplace transforms on their weighted occupation times until first exit times. Such quanti...

We consider a class of stochastic control problems which has been widely used in optimal foraging theory. The state processes have two distinct dynamics, characterized by two pairs of drift and diff...

We study the explosion phenomenon of nonlinear continuous-state branching processes (nonlinear CSBPs). First an explicit integral test for explosion is designed when the rate function does not incre...

In this paper we propose a skew Brownian motion with a two-valued drift as a risk model with endogenous regime switching. We solve its two-sided exit problem and consider an optimal control problem ...

We study quasi-stationary distribution of the continuous-state branching process with competition introduced in Berestycki, Fittipaldi and Fontbona\ (Probab. Theory Relat. Fields, 2018). This proces...

Applying excursion theory, we re-express several well studied fluctuation quantities associated to Parisian ruin problem for L\'evy risk processes in terms of integrals with respect to excursion mea...

We study the ergodic property of a continuous-state branching process with immigration and competition. The exponential ergodicity in a weighted total variation distance is proved under natural assu...

For a probability-measure-valued neutral Fleming-Viot process $Z_t$ with L\'evy mutation and resampling mechanism associated to a general $\Lambda$-coalescent with multiple collisions, we prove the ...

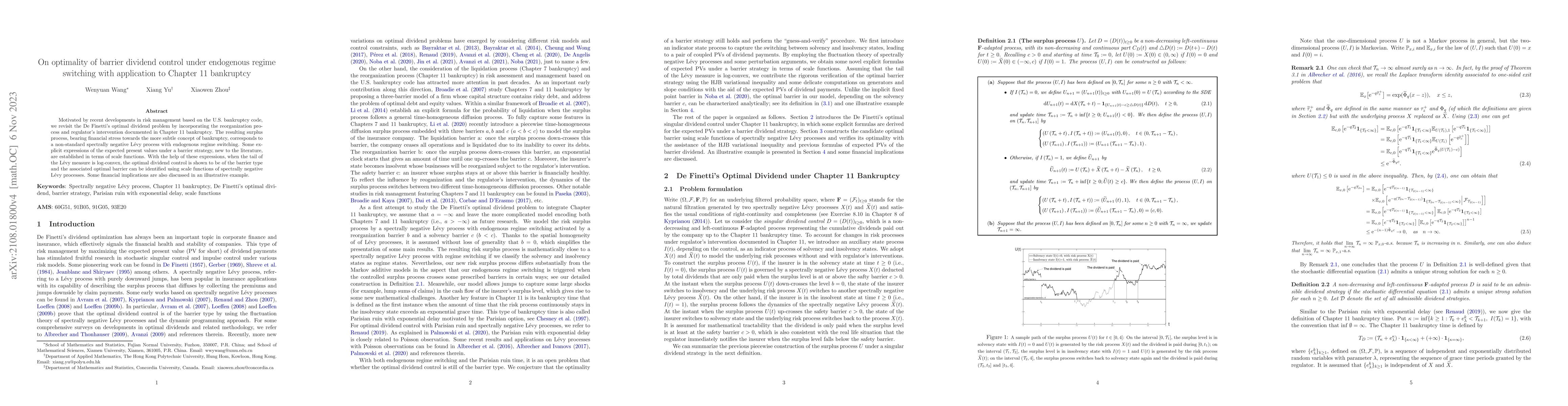

Motivated by recent developments in risk management based on the U.S. bankruptcy code, we revisit the De Finetti's optimal dividend problem by incorporating the reorganization process and regulator'...

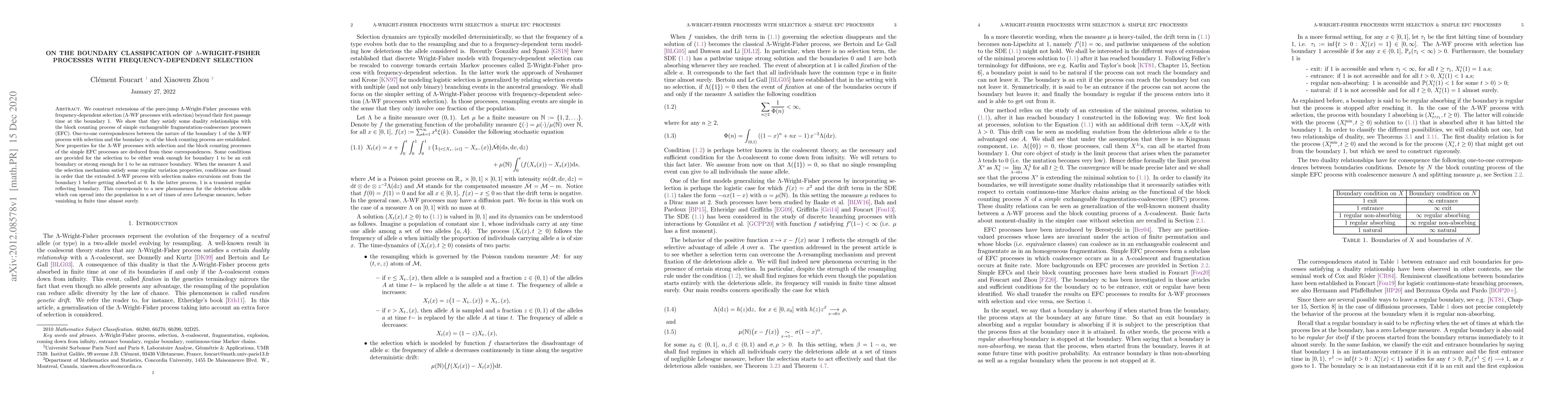

We construct extensions of the pure-jump $\Lambda$-Wright-Fisher processes with frequency-dependent selection ($\Lambda$-WF processes with selection) beyond their first passage time at the boundary ...

Using Foster-Lyapunov techniques we establish new conditions on non-extinction, non-explosion, coming down from infinity and staying infinite, respectively, for the general continuous-state nonlinea...

This paper discusses Parisian ruin problem with capital injection for Levy insurance risk process. Capital injection takes place at the draw-down time of the surplus process when it drops below a pr...

Consider a non-explosive positive Feller process with no negative jumps. It is shown in this note that when infinity is an entrance boundary, in the sense that the entrance times of the process rema...

We study a two-dimensional process $(X, Y)$ arising as the unique nonnegative solution to a pair of stochastic differential equations driven by independent Brownian motions and compensated spectrall...

We find necessary and sufficient conditions for almost sure finiteness of integral functionals of spectrally positive L\'evy processes. Via Lamperti type transforms, these results can be applied to ...

We consider a system of two stochastic differential equations (SDEs) with negative two-way interactions driven by Brownian motions and spectrally positive $\alpha$-stable random measures. Such a SDE s...

For skew Brownian motion with two-valued drift, adopting a perturbation approach we find expressions of its potential densities. As applications, we recover its transition density and study its long-t...

In this paper, we examine a modified version of de Finetti's optimal dividend problem, incorporating fixed transaction costs and altering the surplus process by introducing two-valued drift and two-va...

For a critical simple exchangeable fragmentation-coagulation in slow regime where the coagulation rate and fragmentation rate are of the same order, we show that there exist phase transitions for its ...

The $\Lambda$-Fleming-Viot process is a probability measure-valued process that is dual to a $\Lambda$-coalescent that allows multiple collisions. In this paper, we consider a class of $\Lambda$-Flemi...

We propose threshold diffusion processes as unique solutions to stochastic differential equations with step-function coefficients, and obtain explicit expressions for the conditional Laplace transform...

For a class of time-inhomogeneous SDEs with jumps, we establish criteria for the existence and uniqueness of the nonnegative solutions, and examine the extinction, the explosion together with the cont...

In this paper, we study a two-dimensional process arising as the unique nonnegative solution to a system of two stochastic differential equations (SDEs) with mutually enhancing two-way interactions dr...

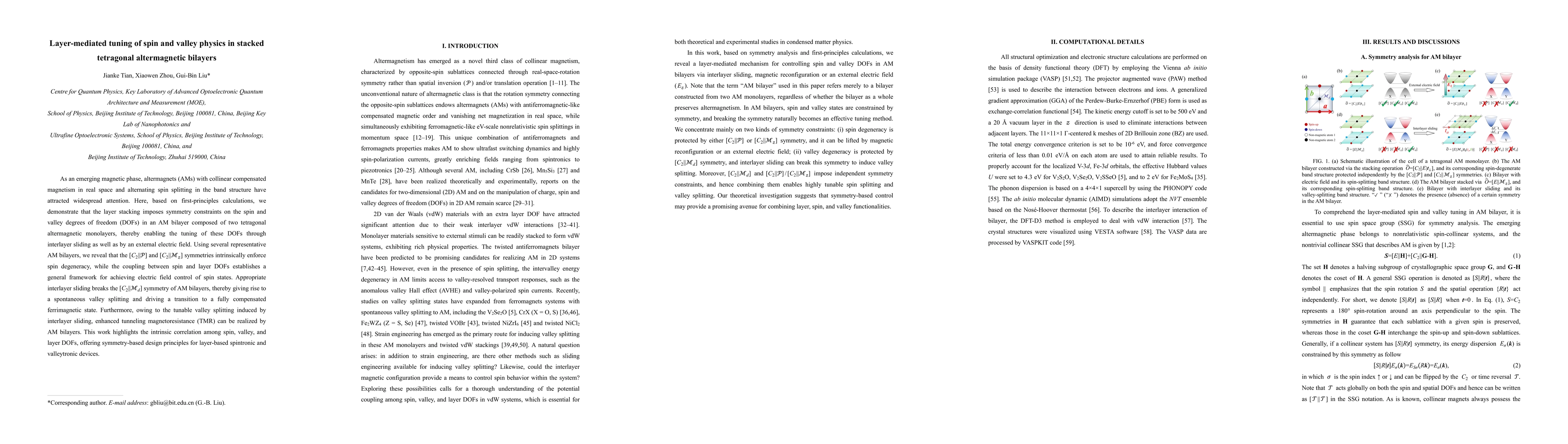

As an emerging magnetic phase, altermagnets (AMs) with collinear compensated magnetism in real space and alternating spin splitting in the band structure have attracted widespread attention. Here, bas...

In this paper, we investigate the asymptotic behavior of continuous-state branching processes in a Brownian random environment (CBBRE) conditioned on non-extinction. For the subcritical case, we prove...

Discrete-time affine processes are widely used in finance and economics and encompass count, positive, and nonnegative-valued processes. This paper develops near-unit-root asymptotic theory for this c...

We study the spatial propagation of super-Brownian motion on $\mathbb{R}^d$ with general critical or subcritical branching mechanisms. Under a Keller-Osserman type integrability condition on the spati...

We study the strong Feller property and irreducibility for continuous-state nonlinear branching processes defined as solutions to stochastic differential equations with jumps. Due to boundary degenera...