Academic Profile

Statistics

Similar Authors

Papers on arXiv

Risk averse decision making under uncertainty in partially observable domains is a fundamental problem in AI and essential for reliable autonomous agents. In our case, the problem is modeled using p...

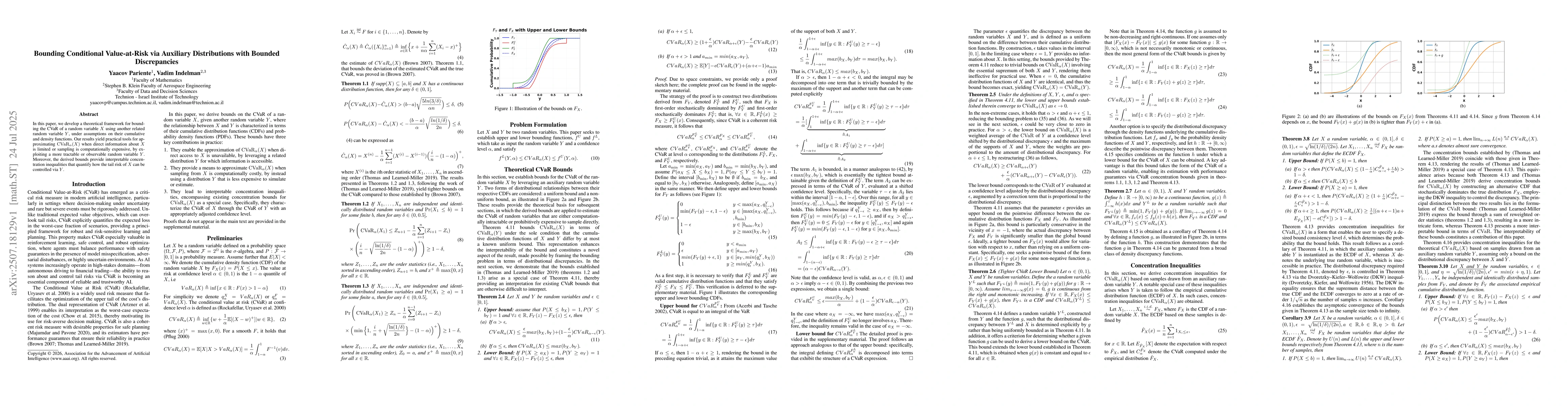

In this paper, we develop a theoretical framework for bounding the CVaR of a random variable $X$ using another related random variable $Y$, under assumptions on their cumulative and density functions....

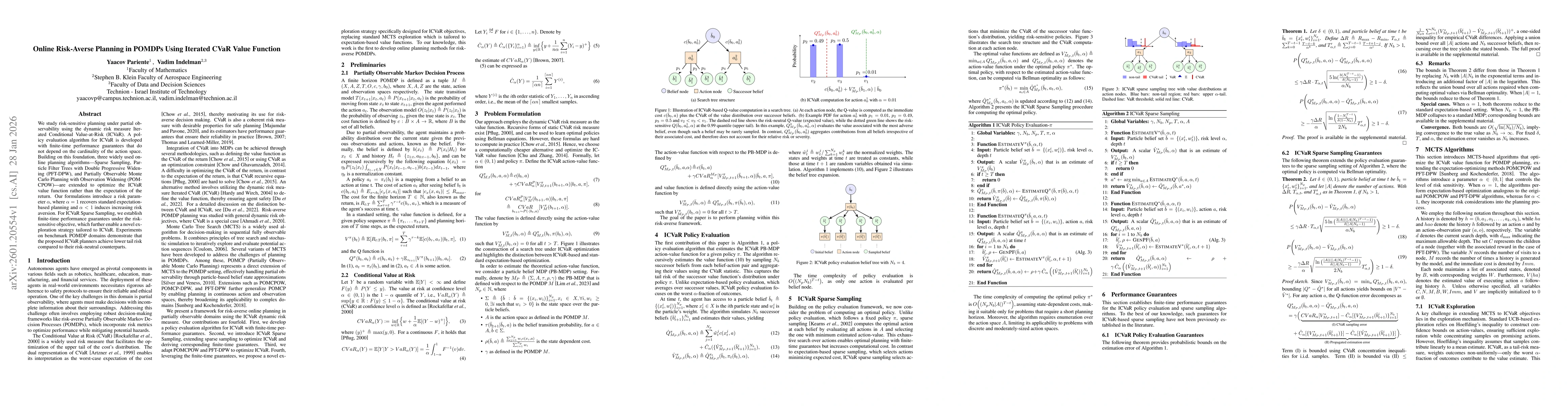

We study risk-sensitive planning under partial observability using the dynamic risk measure Iterated Conditional Value-at-Risk (ICVaR). A policy evaluation algorithm for ICVaR is developed with finite...

We present POMDPPlanners, an open-source Python package for empirical evaluation of Partially Observable Markov Decision Process (POMDP) planning algorithms. The package integrates state-of-the-art pl...

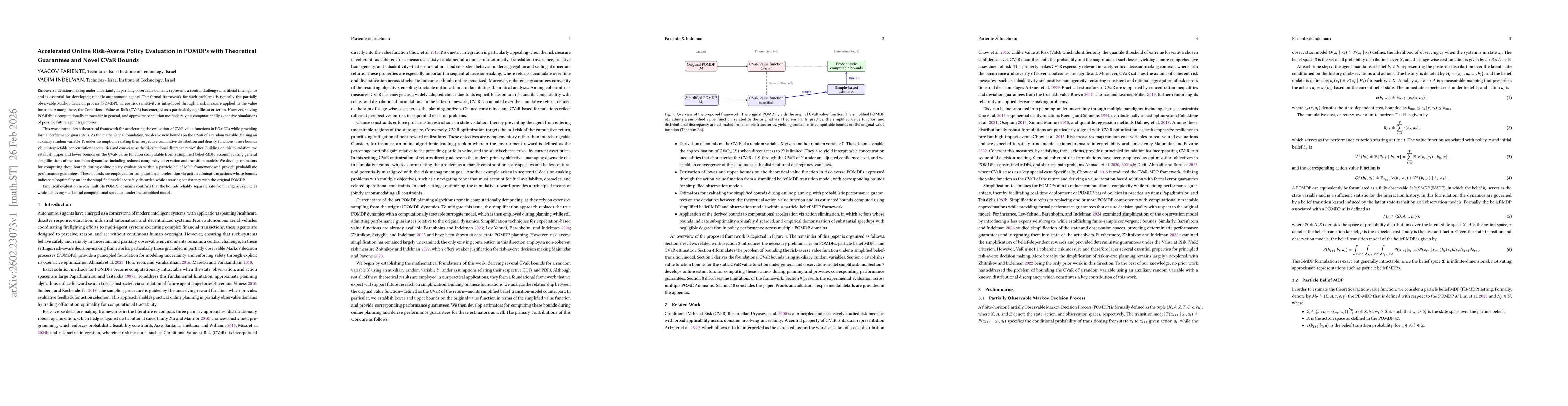

Risk-averse decision-making under uncertainty in partially observable domains is a central challenge in artificial intelligence and is essential for developing reliable autonomous agents. The formal f...