Academic Profile

Statistics

Similar Authors

Papers on arXiv

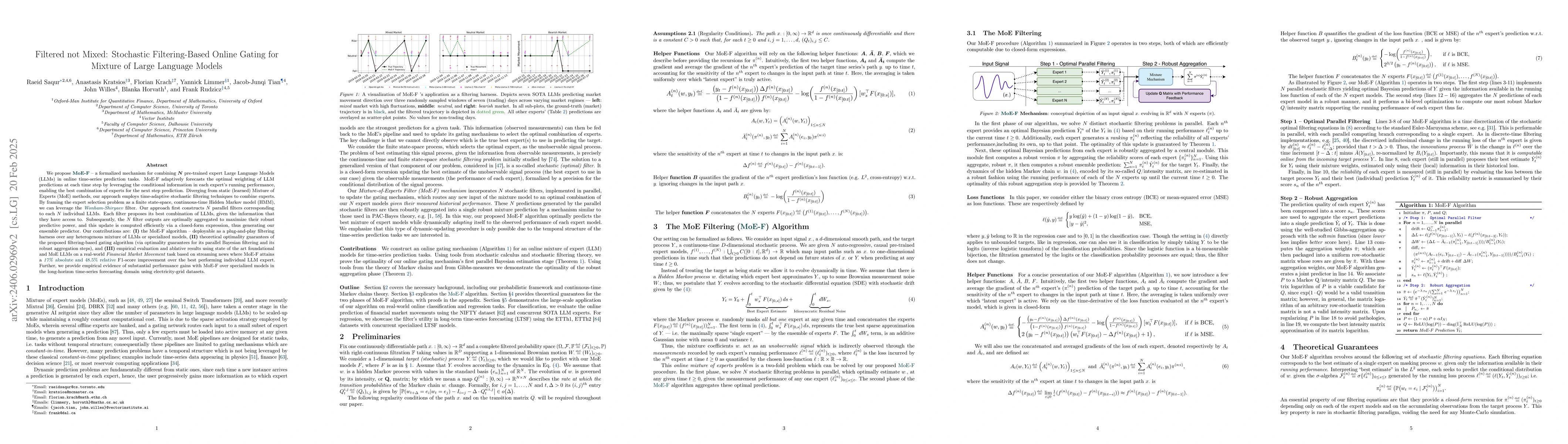

We propose MoE-F -- a formalised mechanism for combining $N$ pre-trained expert Large Language Models (LLMs) in online time-series prediction tasks by adaptively forecasting the best weighting of LL...

One of the inherent challenges in deploying transformers on time series is that \emph{reality only happens once}; namely, one typically only has access to a single trajectory of the data-generating ...

Deep Kalman filters (DKFs) are a class of neural network models that generate Gaussian probability measures from sequential data. Though DKFs are inspired by the Kalman filter, they lack concrete th...

The availability of deep hedging has opened new horizons for solving hedging problems under a large variety of realistic market conditions. At the same time, any model - be it a traditional stochast...

The objective is to develop a general stochastic approach to delays on financial markets. We suggest such a concept in the context of large platonic markets, which allow infinitely many assets and i...

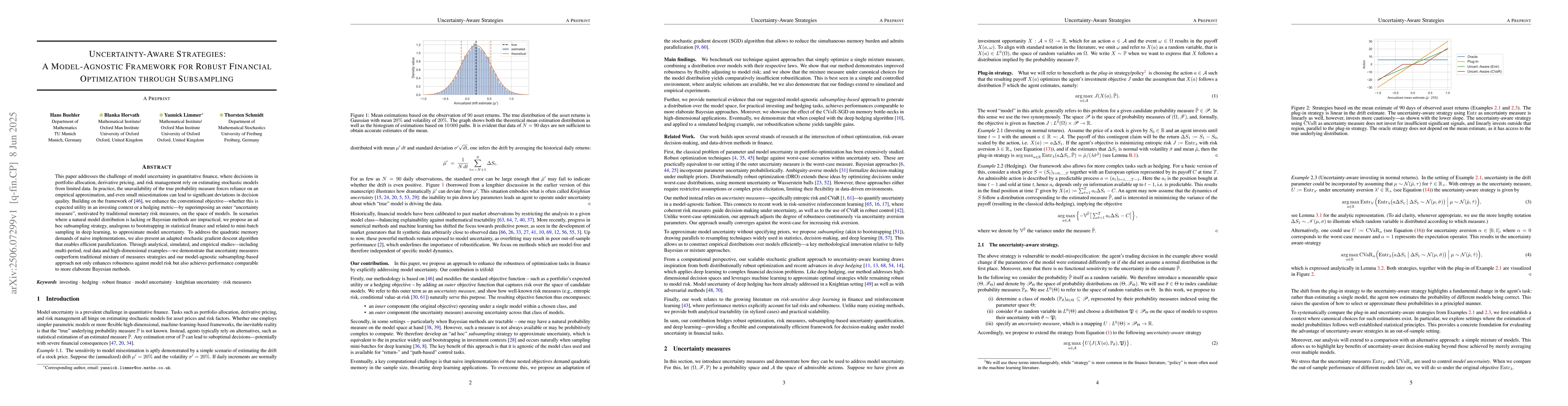

This paper addresses the challenge of model uncertainty in quantitative finance, where decisions in portfolio allocation, derivative pricing, and risk management rely on estimating stochastic models f...

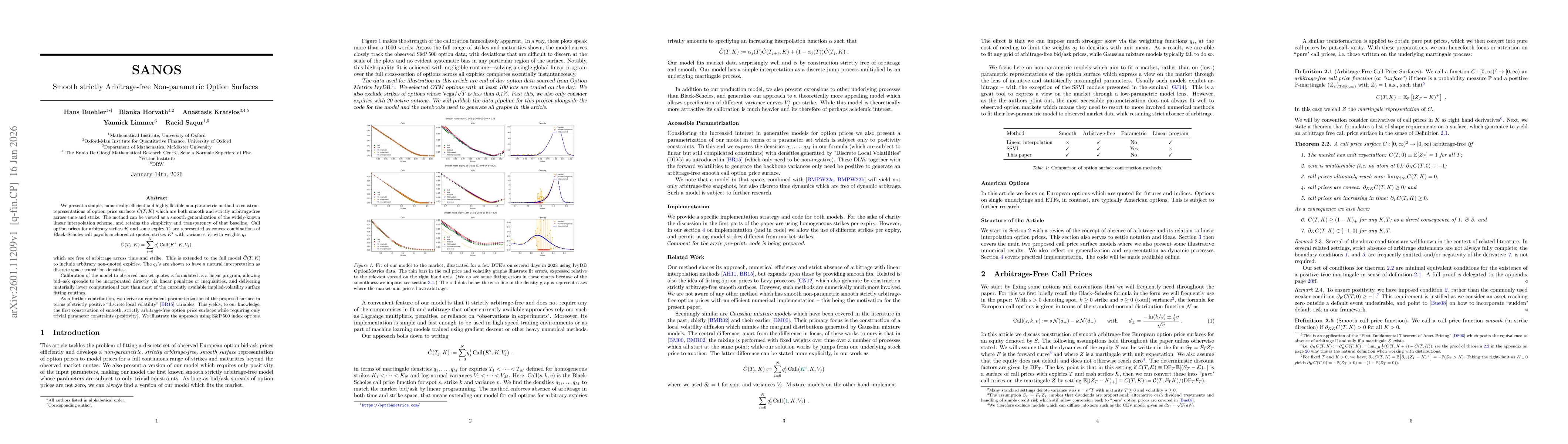

We present a simple, numerically efficient but highly flexible non-parametric method to construct representations of option price surfaces which are both smooth and strictly arbitrage-free across time...

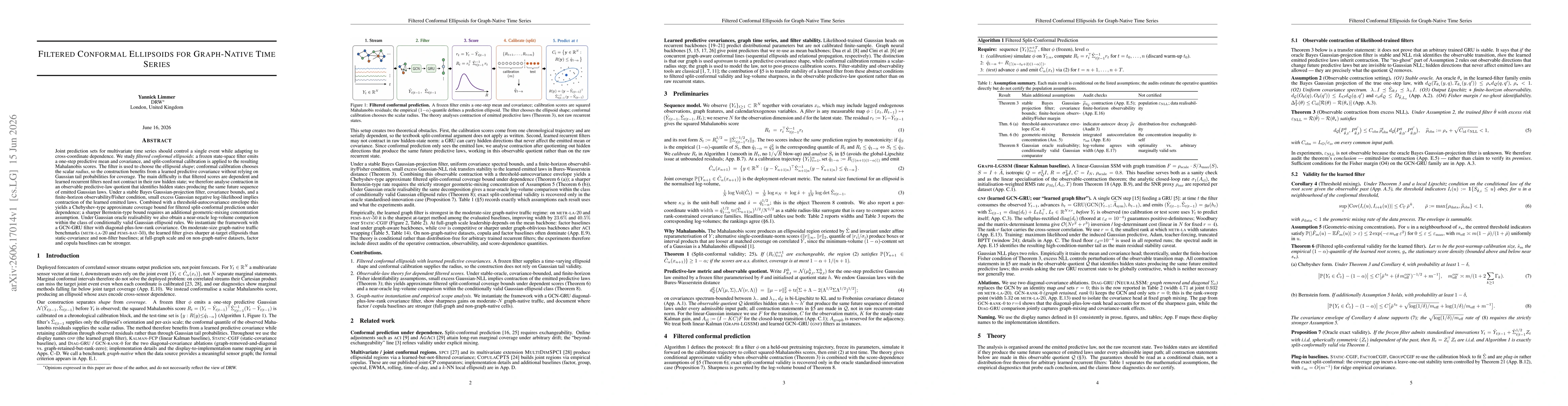

Joint prediction sets for multivariate time series should control a single event while adapting to cross-coordinate dependence. We study filtered conformal ellipsoids: a frozen state-space filter emit...

Modern option-learning systems operate in two coordinates: price space, where markets quote and no-arbitrage constraints are most naturally enforced, and implied volatility (IV) space, where volatilit...