Academic Profile

Statistics

Similar Authors

Papers on arXiv

Intra-day price variations in financial markets are driven by the sequence of orders, called the order flow, that is submitted at high frequency by traders. This paper introduces a novel application...

In this paper we propose a deep recurrent model based on the order flow for the stationary modelling of the high-frequency directional prices movements. The order flow is the microsecond stream of o...

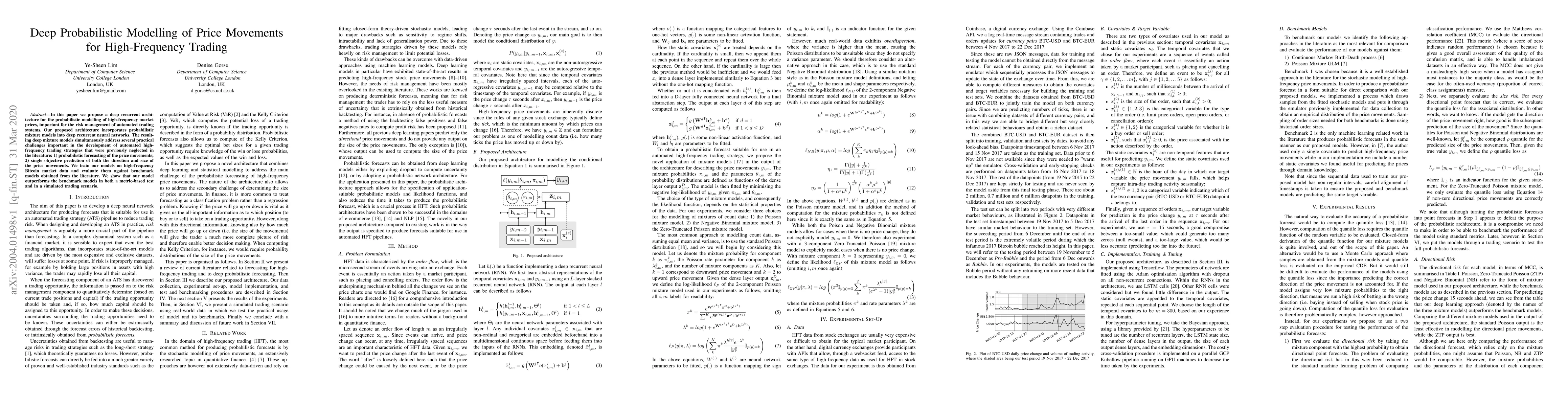

In this paper we propose a deep recurrent architecture for the probabilistic modelling of high-frequency market prices, important for the risk management of automated trading systems. Our proposed a...

At Expedia, learning-to-rank (LTR) models plays a key role on our website in sorting and presenting information more relevant to users, such as search filters, property rooms, amenities, and images. A...