Academic Profile

Statistics

Papers on arXiv

We are interested in solving the Asymmetric Eigenvalue Complementarity Problem (AEiCP) by accelerated Difference-of-Convex (DC) algorithms. Two novel hybrid accelerated DCA: the Hybrid DCA with Line...

In this paper, we are interested in developing an accelerated Difference-of-Convex (DC) programming algorithm based on the exact line search for efficiently solving the Symmetric Eigenvalue Compleme...

In this paper, we propose a clean and general proof framework to establish the convergence analysis of the Difference-of-Convex (DC) programming algorithm (DCA) for both standard DC program and conv...

In this paper, we consider a composite difference-of-convex (DC) program, whose objective function is the sum of a smooth convex function with Lipschitz continuous gradient, a proper closed and conv...

This paper proposes a novel Difference-of-Convex (DC) decomposition for polynomials using a power-sum representation, achieved by solving a sparse linear system. We introduce the Boosted DCA with Ex...

In this paper we consider the difference-of-convex (DC) programming problems, whose objective function is the difference of two convex functions. The classical DC Algorithm (DCA) is well-known for s...

We prove the nonsingularity of a class of integer matrices V(n,d), namely power-product matrix, for positive integers n and d. Some technical proofs are mainly based on linear algebra and enumerativ...

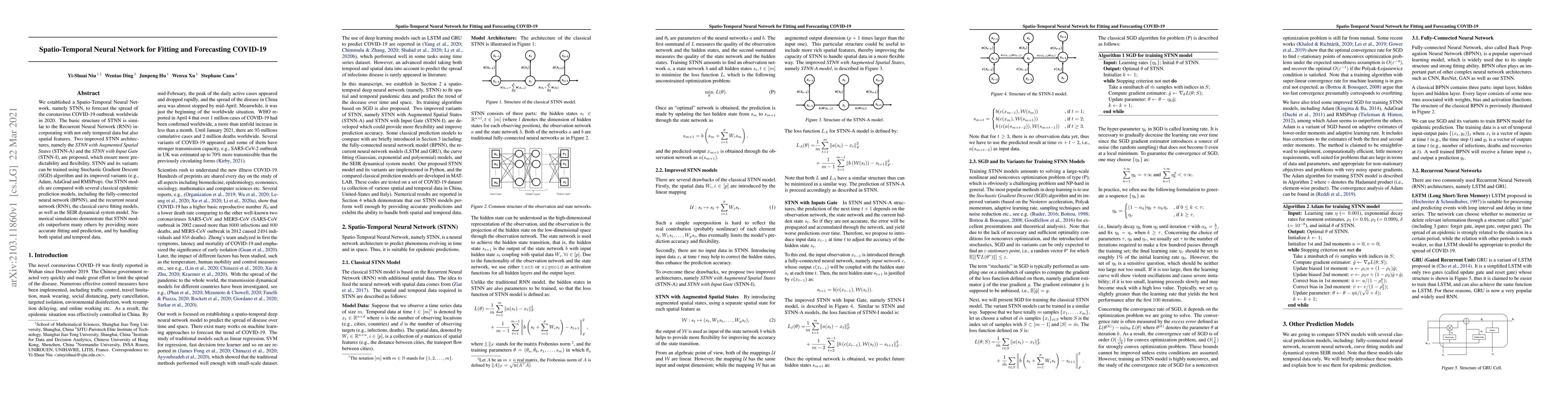

We established a Spatio-Temporal Neural Network, namely STNN, to forecast the spread of the coronavirus COVID-19 outbreak worldwide in 2020. The basic structure of STNN is similar to the Recurrent N...

In this paper, we propose a cutting plane algorithm based on DC (Difference-of-Convex) programming and DC cut for globally solving Mixed-Binary Linear Program (MBLP). We first use a classical DC pro...

In this article, we discuss the numerical solution of Boolean polynomial programs by algorithms borrowing from numerical methods for differential equations, namely the Houbolt scheme, the Lie scheme...

The Mean-Variance-Skewness-Kurtosis (MVSK) portfolio optimization model is a quartic nonconvex polynomial minimization problem over a polytope, which can be formulated as a Difference-of-Convex (DC)...

In this article, we are interested in developing polynomial decomposition techniques based on sums-of-squares (SOS), namely the difference-of-sums-of-squares (D-SOS) and the difference-of-convex-sum...

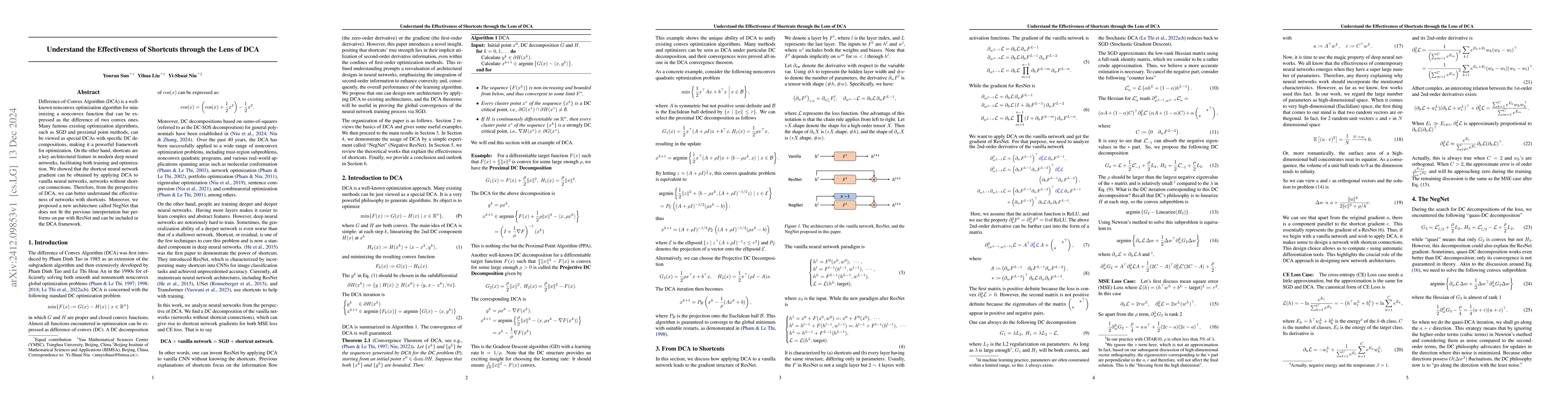

Difference-of-Convex Algorithm (DCA) is a well-known nonconvex optimization algorithm for minimizing a nonconvex function that can be expressed as the difference of two convex ones. Many famous existi...

Nonlinear state estimation under noisy observations is rapidly intractable as system dimension increases. We introduce an improved Yau-Yau filtering framework that breaks the curse of dimensionality a...

We propose Yau's Affine Normal Descent (YAND), a geometric framework for smooth unconstrained optimization in which search directions are defined by the equi-affine normal of level-set hypersurfaces. ...

Affine normal directions provide intrinsic affine-invariant descent directions derived from the geometry of level sets. Their practical use, however, has long been hindered by the need to evaluate thi...

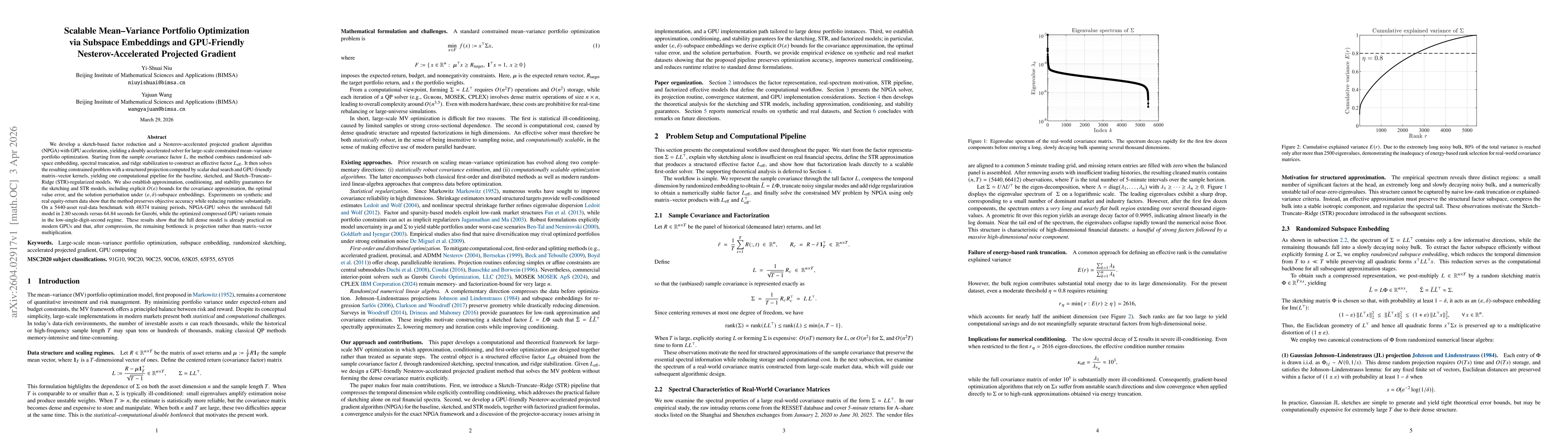

We develop a sketch-based factor reduction and a Nesterov-accelerated projected gradient algorithm (NPGA) with GPU acceleration, yielding a doubly accelerated solver for large-scale constrained mean-v...

Polylab is a MATLAB toolbox for multivariate polynomial scalars and polynomial matrices with a unified symbolic-numeric interface across CPU and GPU-oriented backends. The software exposes three align...

We study the continuous-time structure of the difference-of-convex algorithm (DCA) for smooth DC decompositions with a strongly convex component. In dual coordinates, classical DCA is exactly the full...

Unrestricted mean-variance-skewness-kurtosis portfolio optimization can capture asymmetry and tail risk, but sample-moment formulations become computationally impractical when the asset universe is la...

We study nonsmooth difference-of-convex programs whose subtracted convex term is a finite maximum of smooth convex functions. In this setting, standard DCA iterations may converge to critical points t...