Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we investigated the scaling limit of heavy-tailed unstable cumulative INAR($\infty$) processes. These processes exhibit a power law tail of the form $n^{-(1+\alpha)}$, with $\alpha \i...

In the present paper, we obtain limit theorems for a catogary of Hull-White models with Hawkes jumps including law of large numbers, central limit theorem, and large deviations. In the field of inte...

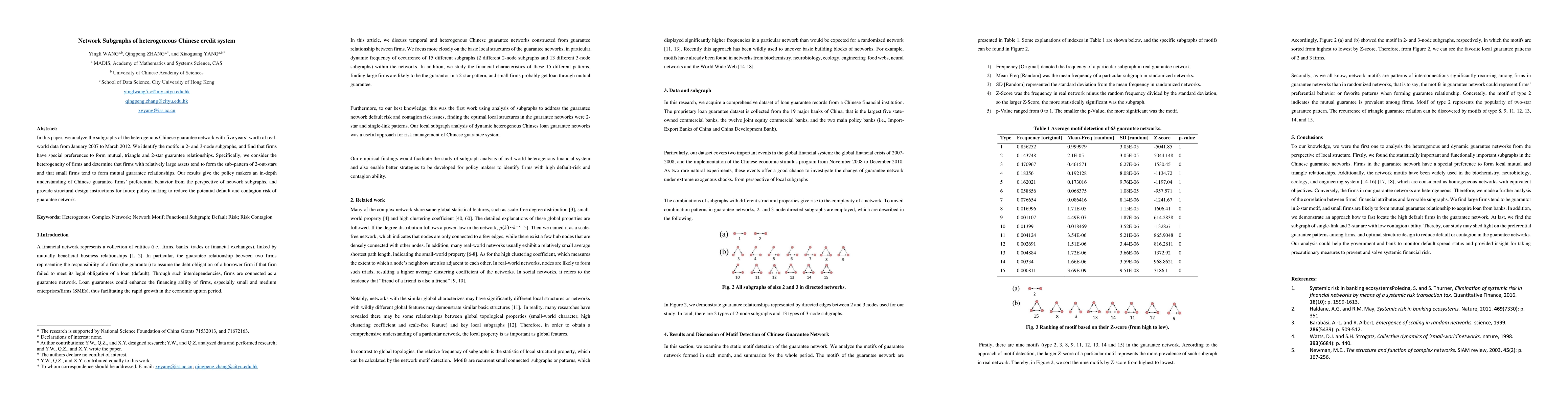

In this study, we investigate the evolution of Chinese guarantee networks from the angle of sub-patterns. First, we find that the mutual, 2-out-stars and triangle sub-patterns are motifs in 2- and 3...

We consider the estimation of the parameters $s = (\nu, \alpha_1, \alpha_2, \cdots, \alpha_T)$ of a cumulative INAR($\infty$) process based on finite observations under the assumption $\sum_{k=1}^T \a...

This paper establishes a novel link between nearly unstable heavy-tailed integer-valued autoregressive (INAR) processes and the rough Heston model via discrete scaling limits. We prove that a sequence...

The problem of sampling a target probability distribution on a constrained domain arises in many applications including machine learning. For constrained sampling, various Langevin algorithms such as ...

We present GLM-4.5, an open-source Mixture-of-Experts (MoE) large language model with 355B total parameters and 32B activated parameters, featuring a hybrid reasoning method that supports both thinkin...

Langevin Monte Carlo (LMC) algorithms are popular Markov Chain Monte Carlo (MCMC) methods to sample a target probability distribution, which arises in many applications in machine learning. Inspired b...

The construction industry faces significant challenges regarding material waste and sustainable practices, necessitating innovative solutions that integrate automation, traceability, and decentralised...

We study the problem of sampling from a target distribution $π(q)\propto e^{-U(q)}$ on $\mathbb{R}^d$, where $U$ can be non-convex, via the Hessian-free high-resolution (HFHR) dynamics, which is a sec...

We study the leading-order fluctuation of stochastic gradient Euler-Maruyama estimators for generalized non-reversible Langevin dynamics. Under structural assumptions tailored to the small-stepsize ce...