Academic Profile

Statistics

Similar Authors

Papers on arXiv

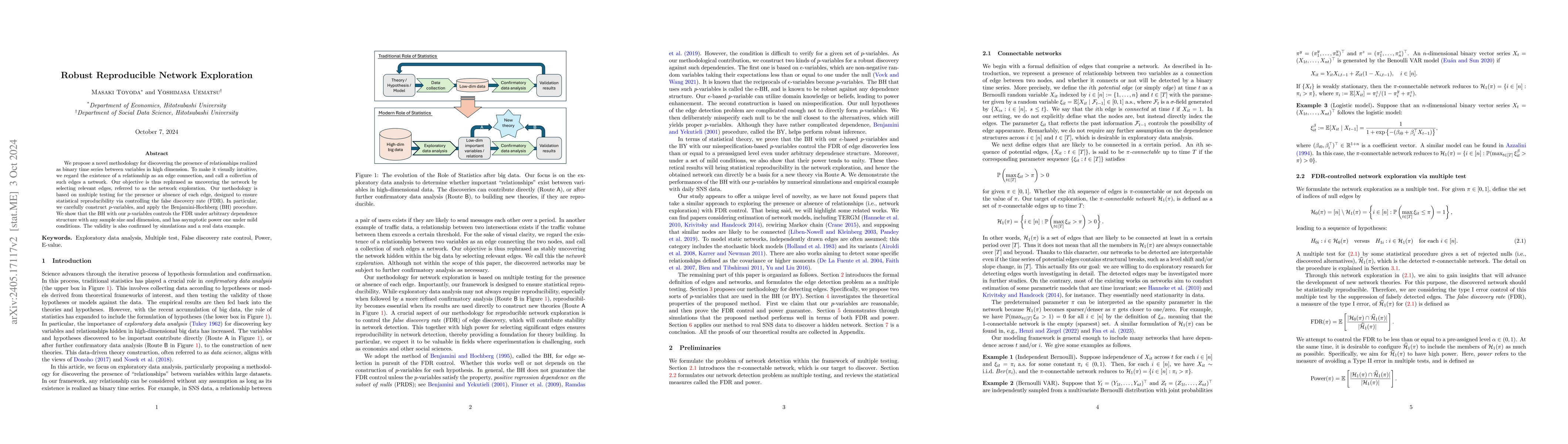

We propose a novel method of network detection that is robust against any complex dependence structure. Our goal is to conduct exploratory network detection, meaning that we attempt to detect a netw...

This study proposes a novel method for estimation and hypothesis testing in high-dimensional single-index models. We address a common scenario where the sample size and the dimension of regression c...

It is well-known that the approximate factor models have the rotation indeterminacy. It has been considered that the principal component (PC) estimators estimate some rotations of the true factors a...

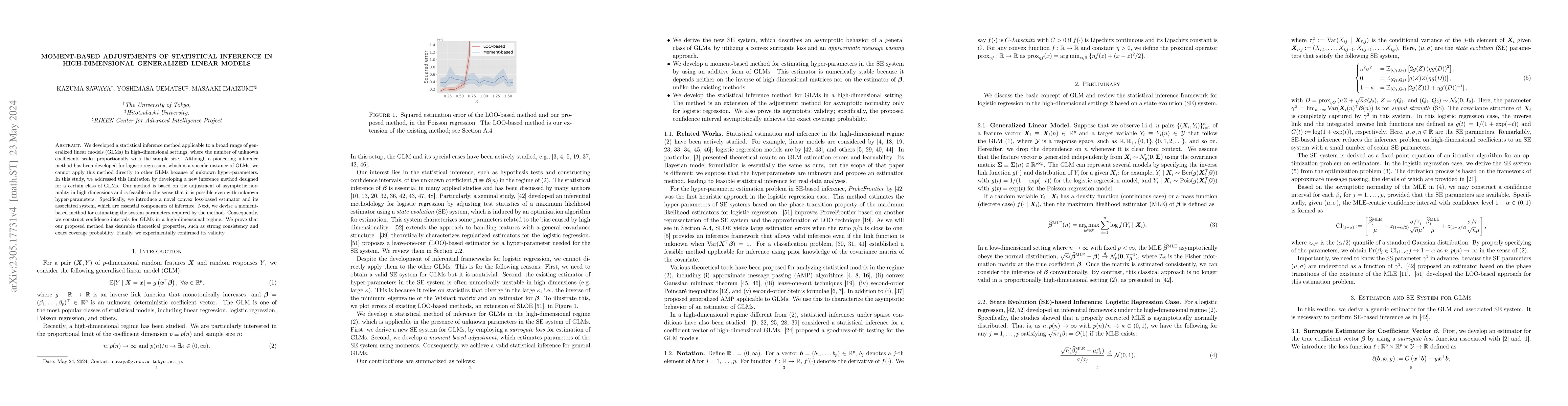

We developed a statistical inference method applicable to a broad range of generalized linear models (GLMs) in high-dimensional settings, where the number of unknown coefficients scales proportional...

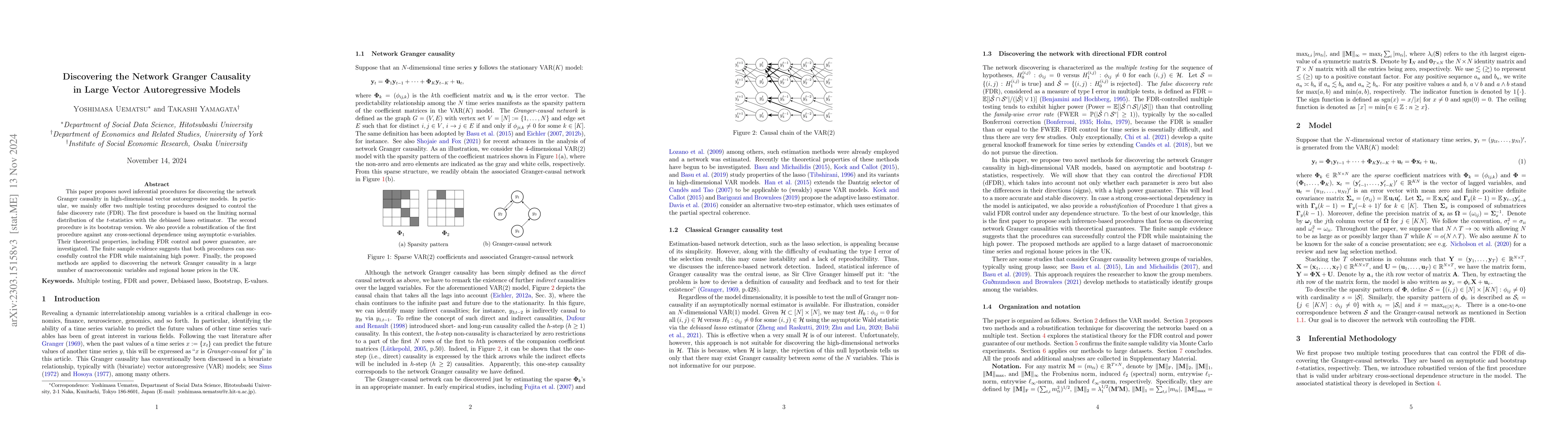

This paper proposes novel inferential procedures for discovering the network Granger causality in high-dimensional vector autoregressive models. In particular, we mainly offer two multiple testing p...

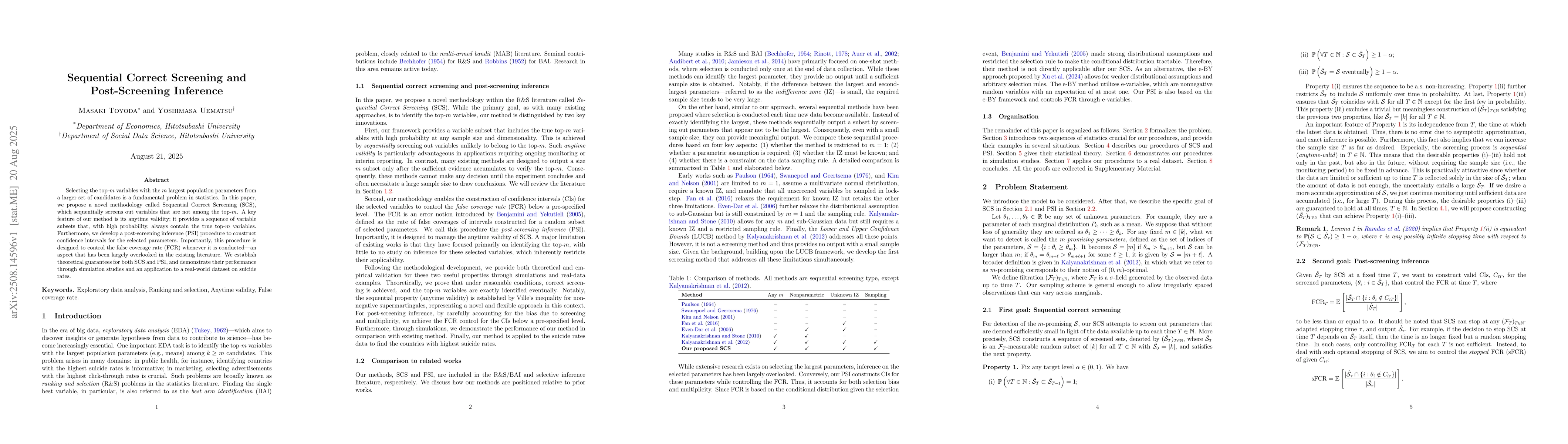

Selecting the top-$m$ variables with the $m$ largest population parameters from a larger set of candidates is a fundamental problem in statistics. In this paper, we propose a novel methodology called ...

In this paper, we study the asymptotic bias of the factor-augmented regression estimator and its reduction, which is augmented by the $r$ factors extracted from a large number of $N$ variables with $T...

We propose a conditional independence (CI) test based on a new measure, the \emph{spectral generalized covariance measure} (SGCM). The SGCM is constructed by approximating the basis expansion of the s...

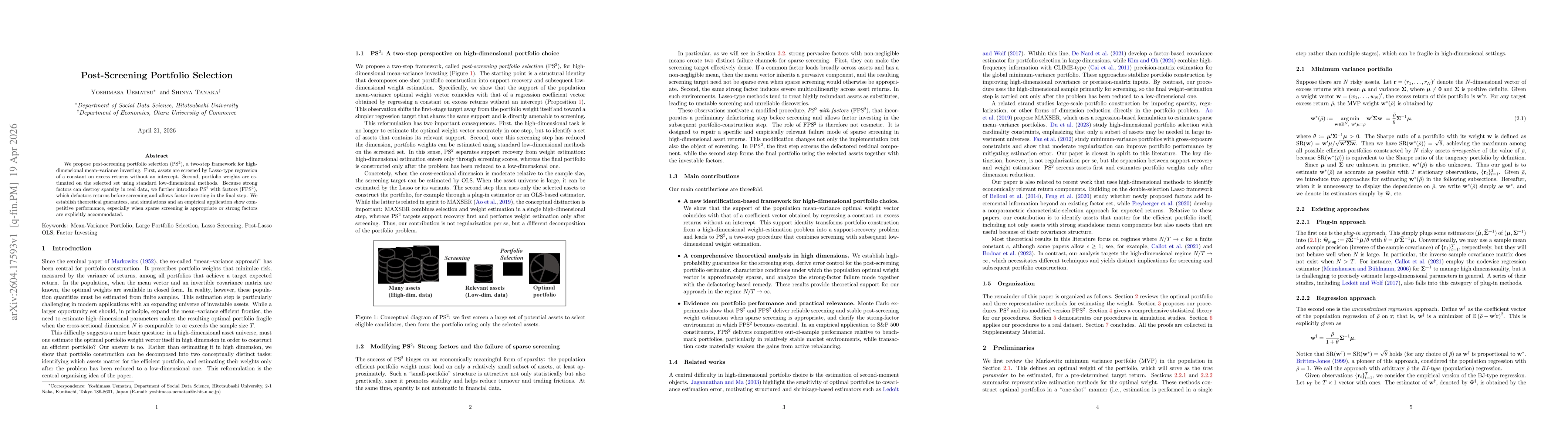

We propose post-screening portfolio selection (PS$^2$), a two-step framework for high-dimensional mean--variance investing. First, assets are screened by Lasso-type regression of a constant on excess ...