Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper considers both the least squares and quasi-maximum likelihood estimation for the recently proposed scalable ARMA model, a parametric infinite-order vector AR model, and their asymptotic n...

This paper develops a flexible and computationally efficient multivariate volatility model, which allows for dynamic conditional correlations and volatility spillover effects among financial assets....

This paper introduces a robust and computationally efficient estimation framework for high-dimensional volatility models in the BEKK-ARCH class. The proposed approach employs data truncation to ensure...

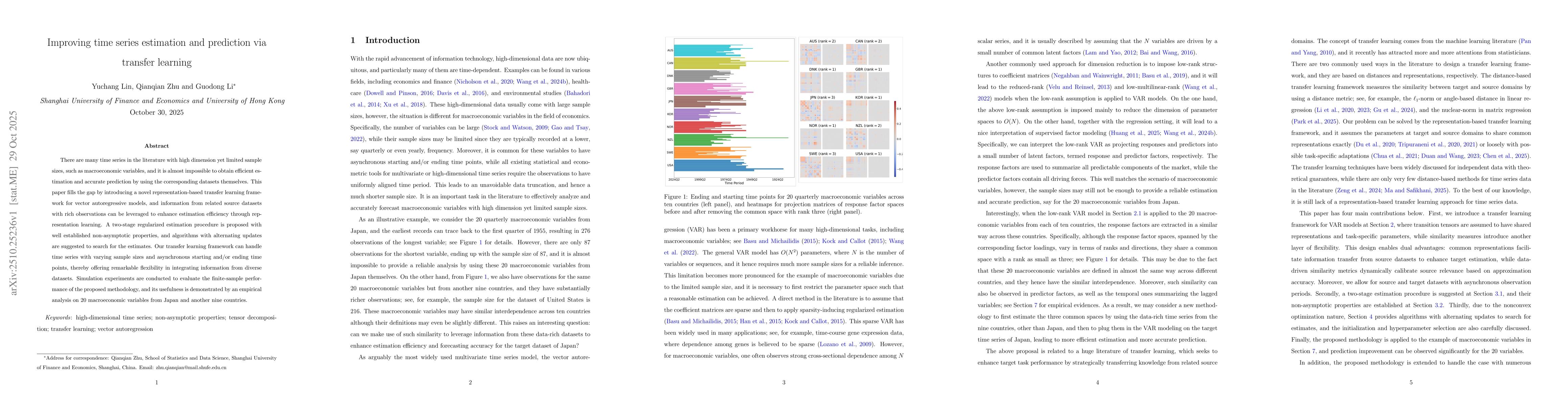

There are many time series in the literature with high dimension yet limited sample sizes, such as macroeconomic variables, and it is almost impossible to obtain efficient estimation and accurate pred...