Academic Profile

Statistics

Similar Authors

Papers on arXiv

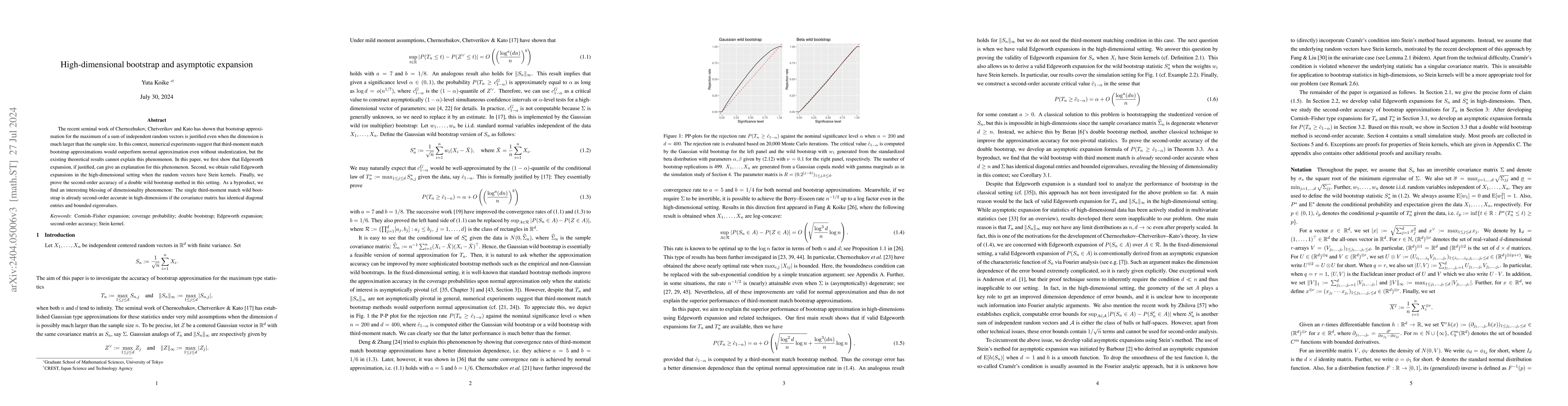

The recent seminal work of Chernozhukov, Chetverikov and Kato has shown that bootstrap approximation for the maximum of a sum of independent random vectors is justified even when the dimension is mu...

Motivated by statistical analysis of latent factor models for high-frequency financial data, we develop sharp upper bounds for the spectral norm of the realized covariance matrix of a high-dimension...

In the literature of high-dimensional central limit theorems, there is a gap between results for general limiting correlation matrix $\Sigma$ and the strongly non-degenerate case. For the general ca...

Let $X_1,\dots,X_n$ be i.i.d. log-concave random vectors in $\mathbb R^d$ with mean 0 and covariance matrix $\Sigma$. We study the problem of quantifying the normal approximation error for $W=n^{-1/...

In this paper, we develop a general theory for adaptive nonparametric estimation of the mean function of a non-stationary and nonlinear time series model using deep neural networks (DNNs). We first ...

We use a new method via $p$-Wasserstein bounds to prove Cram\'er-type moderate deviations in (multivariate) normal approximations. In the classical setting that $W$ is a standardized sum of $n$ inde...

This article reviews recent progress in high-dimensional bootstrap. We first review high-dimensional central limit theorems for distributions of sample mean vectors over the rectangles, bootstrap co...

Recently, many studies have shed light on the high adaptivity of deep neural network methods in nonparametric regression models, and their superior performance has been established for various funct...

We obtain explicit error bounds for the $d$-dimensional normal approximation on hyperrectangles for a random vector that has a Stein kernel, or admits an exchangeable pair coupling, or is a non-line...

This paper deals with the Gaussian and bootstrap approximations to the distribution of the max statistic in high dimensions. This statistic takes the form of the maximum over components of the sum o...

Let $X_1,\dots,X_n$ be independent centered random vectors in $\mathbb{R}^d$. This paper shows that, even when $d$ may grow with $n$, the probability $P(n^{-1/2}\sum_{i=1}^nX_i\in A)$ can be approxi...

This paper develops a new statistical inference theory for the precision matrix of high-frequency data in a high-dimensional setting. The focus is not only on point estimation but also on interval e...

This paper develops a quantitative version of de Jong's central limit theorem for homogeneous sums in a high-dimensional setting. More precisely, under appropriate moment assumptions, we establish a...

Motivated by small bandwidth asymptotics for kernel-based semiparametric estimators in econometrics, this paper establishes Gaussian approximation results for high-dimensional fixed-order $U$-statisti...

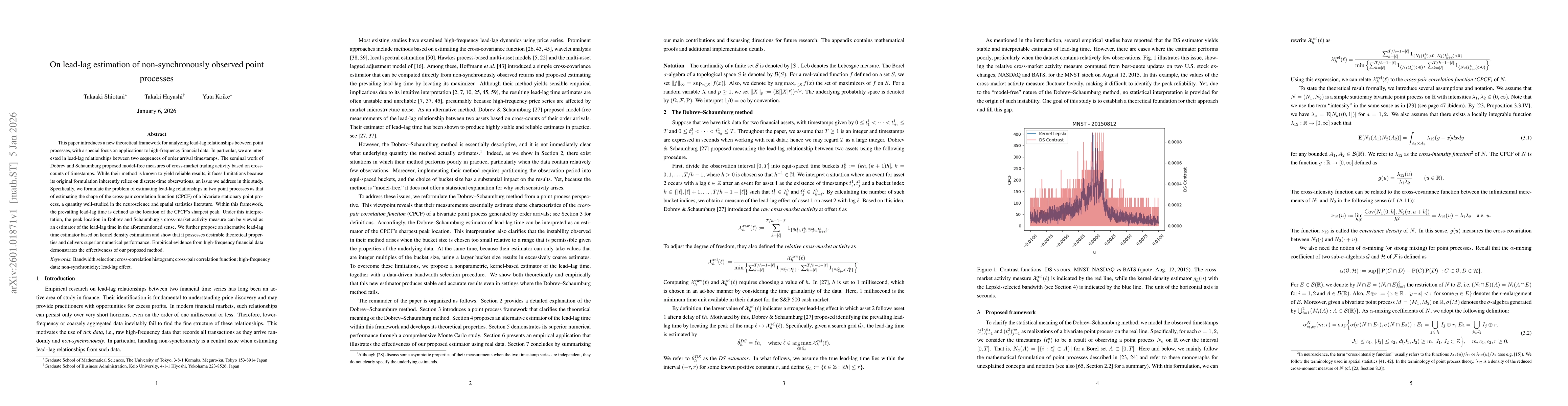

This paper introduces a new theoretical framework for analyzing lead-lag relationships between point processes, with a special focus on applications to high-frequency financial data. In particular, we...

This paper studies sampling error bounds for denoising diffusion probabilistic models (DDPMs) in the 2-Wasserstein distance. Our contributions are threefold. (i) Under general Lipschitz-type condition...

The Föllmer process is a Brownian motion conditioned to have a pre-specified distribution at time 1. This process can be interpreted as an "augmented" time-compressed version of the reverse stochastic...