Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider a strictly stationary random field on the two-dimensional integer lattice with regularly varying marginal and finite-dimensional distributions. Exploiting the regular variation, we defin...

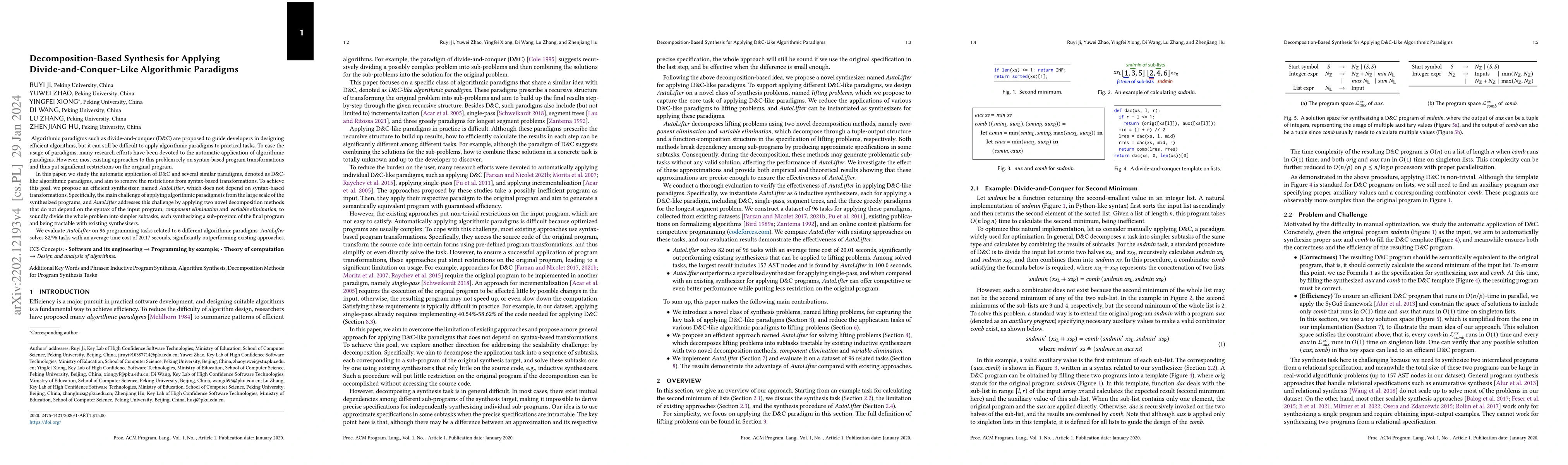

Algorithmic paradigms such as divide-and-conquer (D&C) are proposed to guide developers in designing efficient algorithms, but it can still be difficult to apply algorithmic paradigms to practical t...

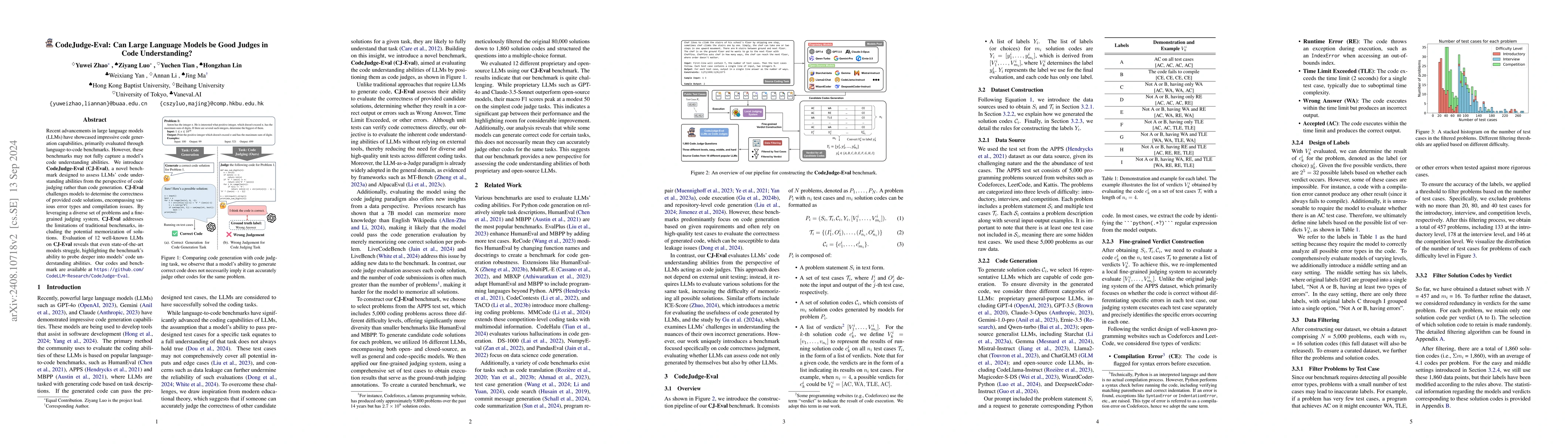

Recent advancements in large language models (LLMs) have showcased impressive code generation capabilities, primarily evaluated through language-to-code benchmarks. However, these benchmarks may not f...

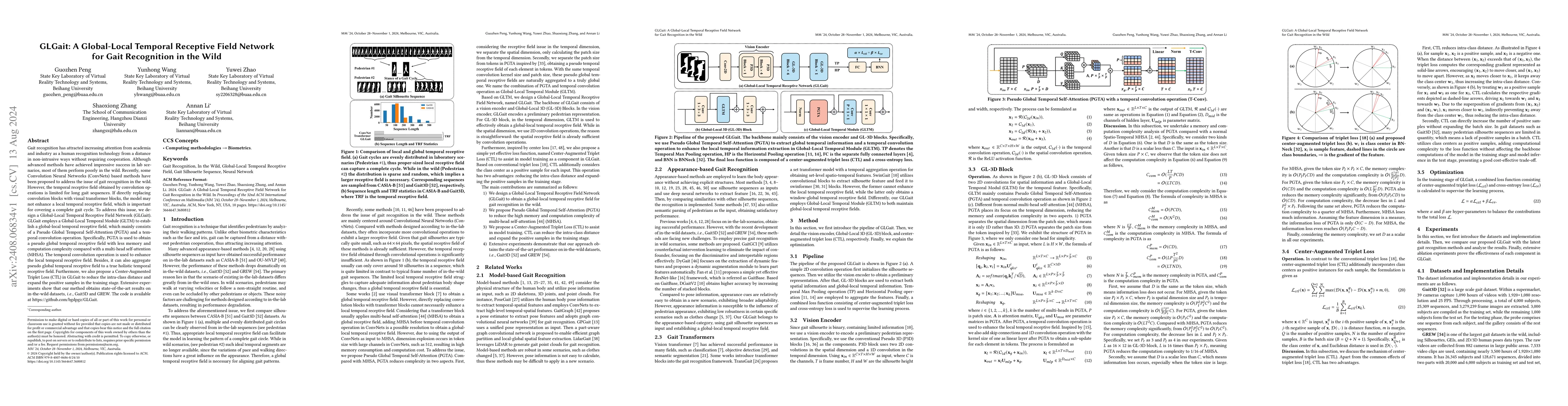

Gait recognition has attracted increasing attention from academia and industry as a human recognition technology from a distance in non-intrusive ways without requiring cooperation. Although advanced ...

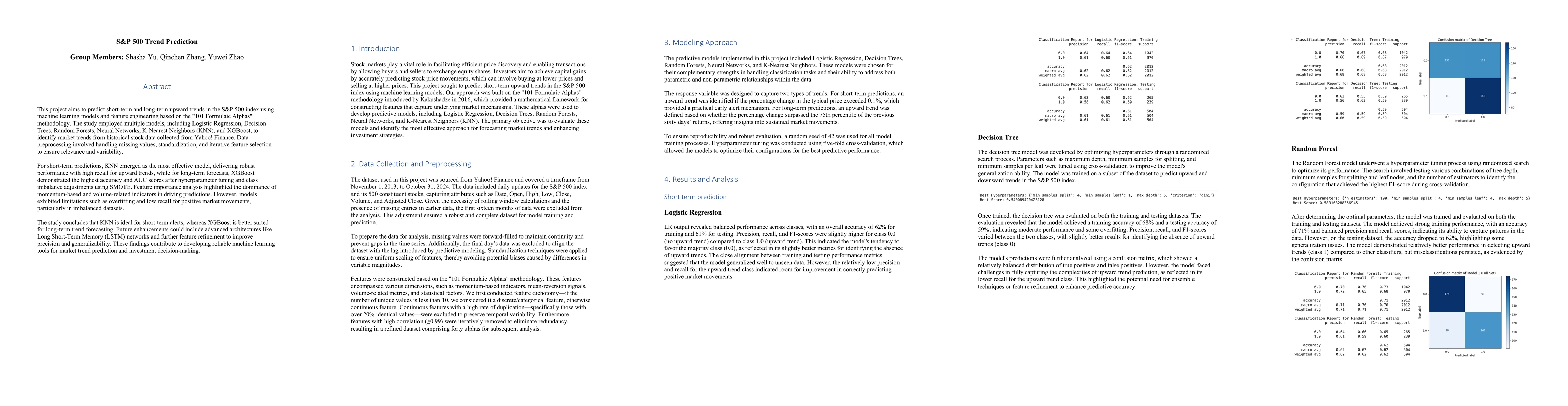

This project aims to predict short-term and long-term upward trends in the S&P 500 index using machine learning models and feature engineering based on the "101 Formulaic Alphas" methodology. The stud...

Marginal expected shortfall (MES) is an important measure when assessing and quantifying the contribution of the financial institution to a systemic crisis. In this paper, we propose time-lagged margi...

Recent advances in data collection technologies have led to the widespread availability of functional data observed over time, often exhibiting strong temporal dependence. However, existing methodolog...

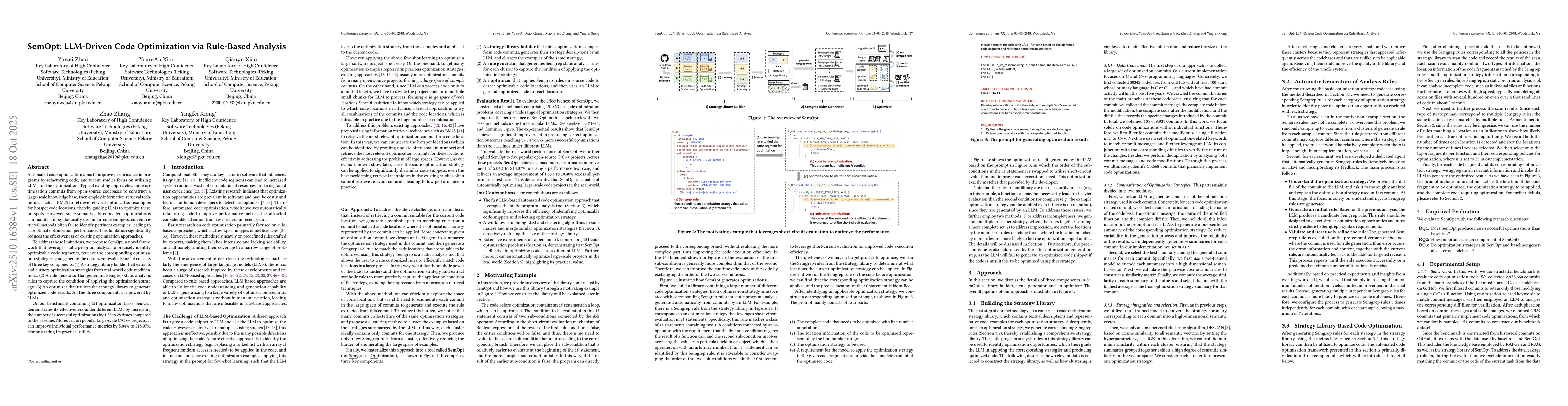

Automated code optimization aims to improve performance in programs by refactoring code, and recent studies focus on utilizing LLMs for the optimization. Typical existing approaches mine optimization ...

We develop goodness-of-fit tests for max-stable random fields, which are used to model heavy-tailed spatial data. The test statistics are constructed based on the Fourier transforms of the indicators ...