Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider a branching random walk on a multi($Q$)-type, supercritical Galton-Watson tree which satisfies Kesten-Stigum condition. We assume that the displacements associated with the particles of ...

We study a branching random walk with independent and identically distributed, heavy tailed displacements. The offspring law is supercritical and satisfies the Kesten-Stigum condition. We treat the ...

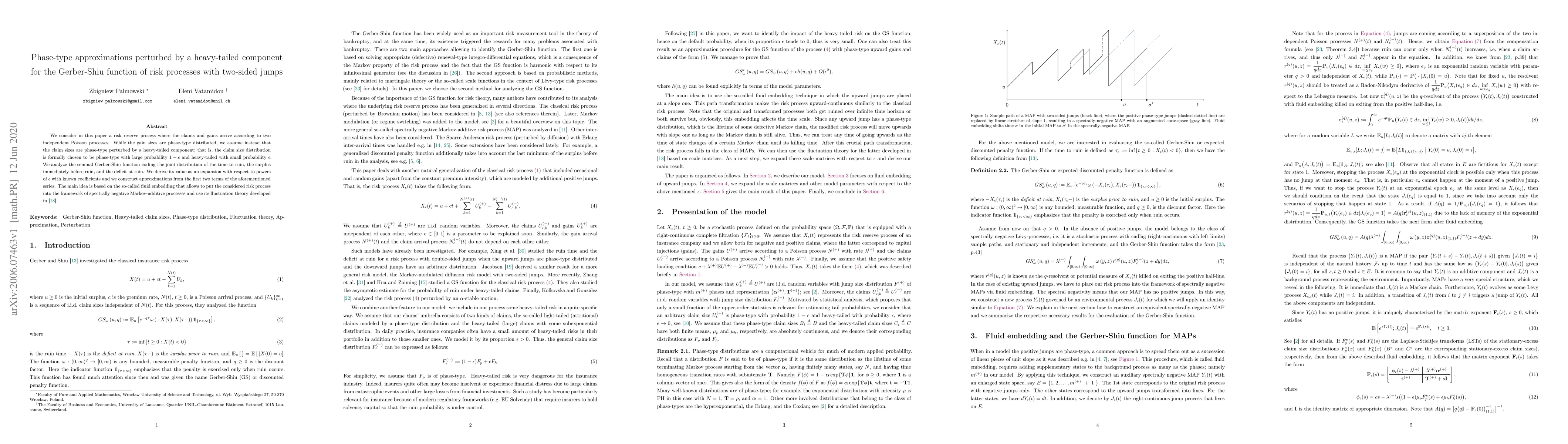

In this paper we determine bounds and exact asymptotics of the ruin probability for risk process with arrivals given by a linear marked Hawkes process. We consider the light-tailed and heavy-tailed ...

We find the asymptotics of the value function maximizing the expected utility of discounted dividend payments of an insurance company whose reserves are modeled as a classical Cram\'er risk process,...

In this paper, we generalise the results presented in the literature for the ruin probability for the insurer--reinsurer model under a pro-rata reinsurance contract. We consider claim amounts that a...

We perform the sensitivity analysis of a level-dependent QBD with a particular focus on applications in modelling healthcare systems.

We consider a neighbourhood random walk on a quadrant, $\{(X_1(t),X_2(t),\varphi(t)):t\geq 0\}$, with state space \begin{eqnarray*} \mathcal{S}&=&\{(n,m,i):n,m=0,1,2,\ldots;i=1,2,\ldots,k(n,m)\}. ...

We derive the explicit price of the perpetual American put option cancelled at the last passage time of the underlying above some fixed level. We assume the asset process is governed by a geometric ...

In this paper we develop the Gerber-Shiu theory for the classic and dual discrete risk processes in a Markovian (regime switching) environment. In particular, by expressing the Gerber-Shiu function ...

We study critical GI/G/1 queues under finite second moment assumptions. We show that the busy period distribution is regularly varying with index half. We also review previously known M/G/1/ and M/M...

We consider a discrete time parallel queue, which is two-queue network, where at each time-slot there is a the same batch arrival to both queues and at each queue there is a random service available...

In this paper we give few expressions and asymptotics of ruin probabilities for a Markov modulated risk process for various regimes of a time horizon, initial reserves and a claim size distribution....

The main objective of this paper is to present an algorithm of pricing perpetual American put options with asset-dependent discounting. The value function of such an instrument can be described as \...

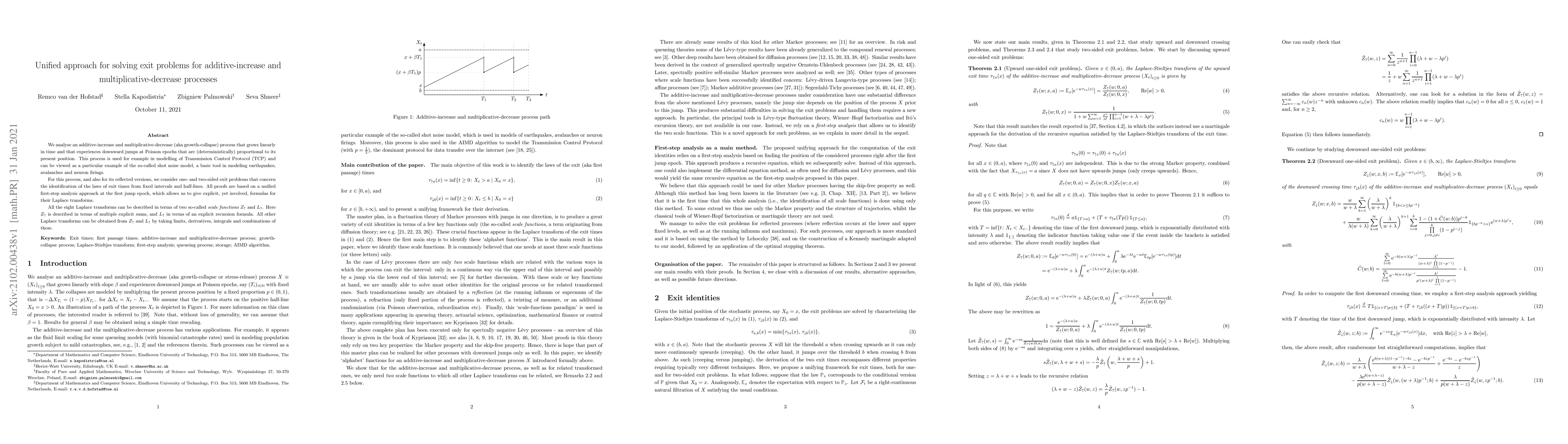

We analyse an additive-increase and multiplicative-decrease (aka growth-collapse) process that grows linearly in time and that experiences downward jumps at Poisson epochs that are (deterministicall...

In this article, we consider a Branching Random Walk on the real line. The genealogical structure is assumed to be given through a supercritical branching process in the i.i.d. environment and satis...

In this paper, we build on the techniques developed in Albrecher et al. (2013), to generate initial-boundary value problems for ruin probabilities of surplus-dependent premium risk processes, under ...

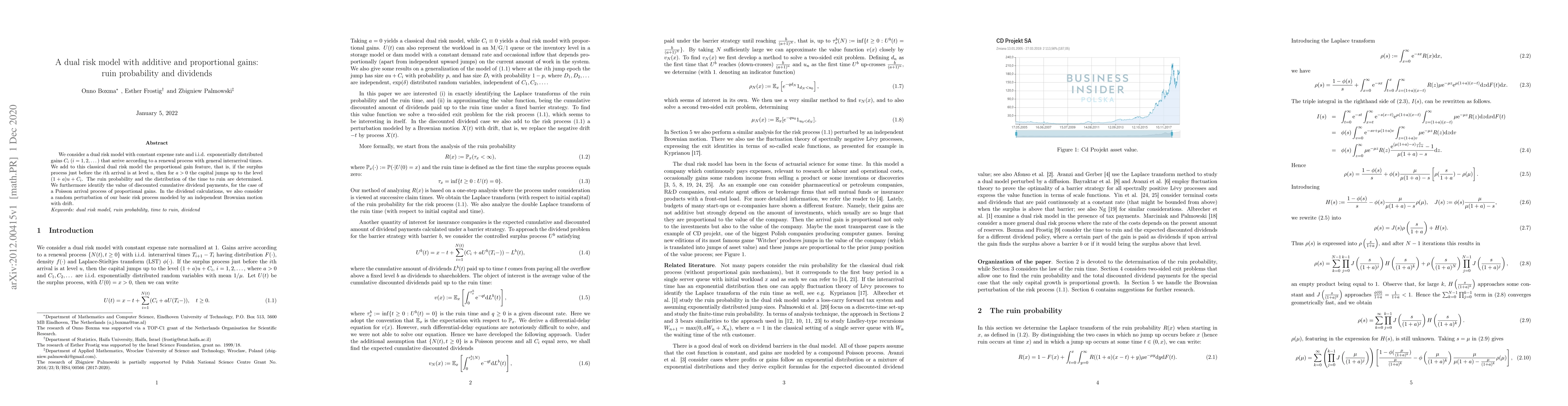

We consider a dual risk model with constant expense rate and i.i.d. exponentially distributed gains $C_i$ ($i=1,2,\dots$) that arrive according to a renewal process with general interarrival times. ...

In this paper we analyze the distributional properties of a busy period in an on-off fluid queue and the a first passage time in a fluid queue driven by a finite state Markov process. In particular,...

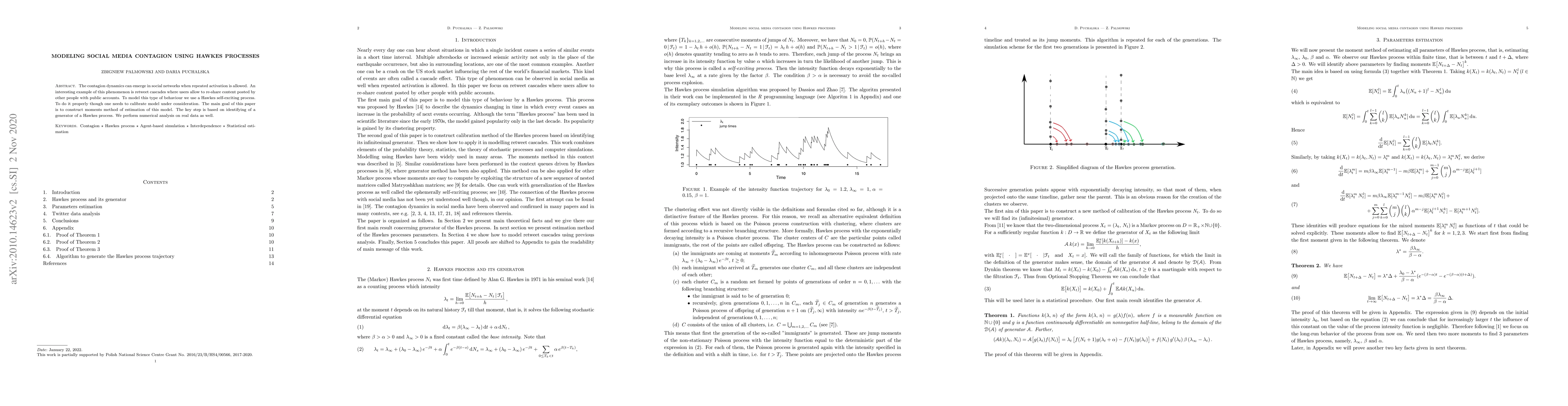

The contagion dynamics can emerge in social networks when repeated activation is allowed. An interesting example of this phenomenon is retweet cascades where users allow to re-share content posted b...

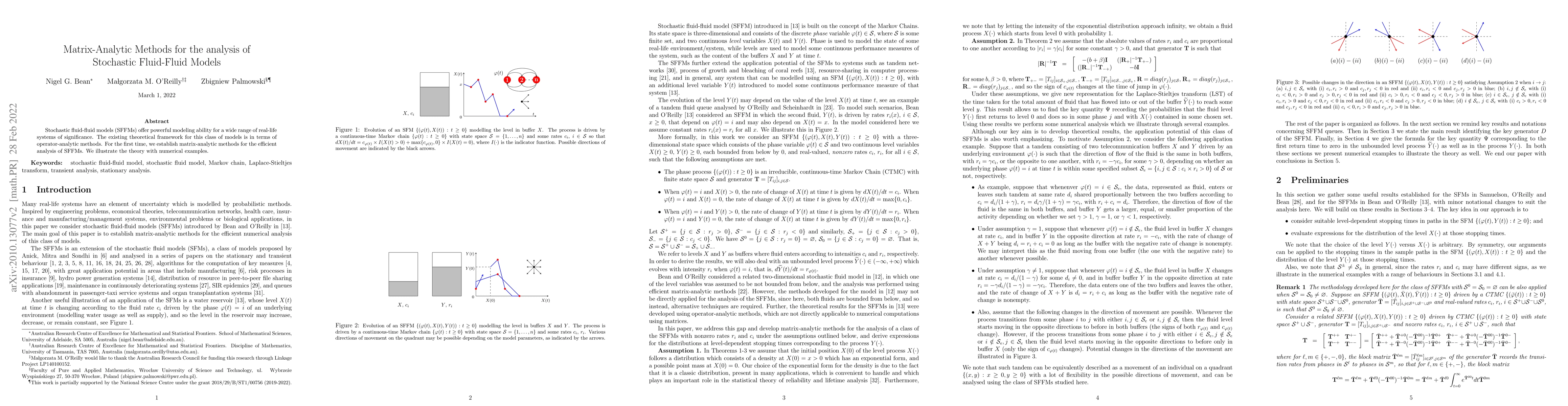

Stochastic fluid-fluid models (SFFMs) offer powerful modeling ability for a wide range of real-life systems of significance. The existing theoretical framework for this class of models is in terms o...

In this paper we consider (upward skip-free) discrete-time and discrete-space Markov additive chains (MACs) and develop the theory for the so-called $\tilde{W}$ and $\tilde{Z}$ scale matrices. which...

Motivated by a seminal paper of Kesten et al. (1975) we consider a branching process with a geometric offspring distribution with i.i.d. random environmental parameters $A_n$, $n\ge 1$ and size -1 i...

In this paper we consider the following optimal stopping problem $$V^{\omega}_{\rm A}(s) = \sup_{\tau\in\mathcal{T}} \mathbb{E}_{s}[e^{-\int_0^\tau \omega(S_w) dw} g(S_\tau)],$$ where the process $S...

We consider in this paper a risk reserve process where the claims and gains arrive according to two independent Poisson processes. While the gain sizes are phase-type distributed, we assume instead ...

We consider the distributional fixed-point equation: $$R \stackrel{\mathcal{D}}{=} Q \vee \left( \bigvee_{i=1}^N C_i R_i \right),$$ where the $\{R_i\}$ are i.i.d.~copies of $R$, independent of the v...

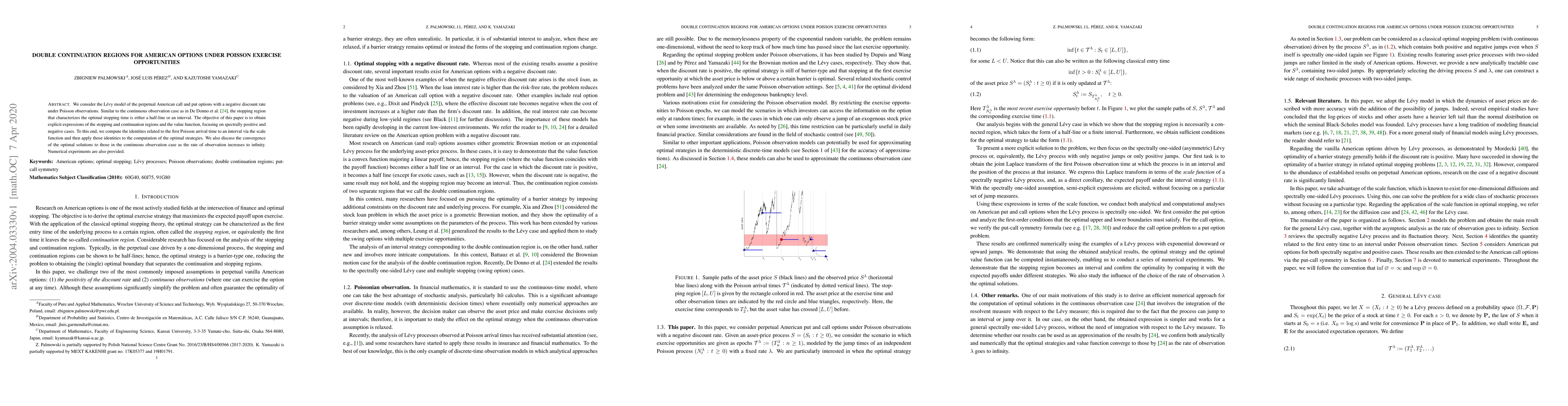

We consider the L\'evy model of the perpetual American call and put options with a negative discount rate under Poisson observations. Similar to the continuous observation case as in De Donno et al....

This paper presents an analysis of the stochastic recursion $W_{i+1} = [V_iW_i+Y_i]^+$ that can be interpreted as an autoregressive process of order 1, reflected at 0. We start our exposition by a d...

This paper considers an optimal dividend distribution problem for an insurance company where the dividends are paid in a foreign currency. In the absence of dividend payments, our risk process follo...

Let $X_t^\sharp$ be a multivariate process of the form $X_t =Y_t - Z_t$, $X_0=x$, killed at some terminal time $T$, where $Y_t$ is a Markov process having only jumps of the length smaller than $\del...

In this paper we provide the analysis of the limiting conditional distribution (Yaglom limit) for stochastic fluid models (SFMs), a key class of models in the theory of matrix-analytic methods. So f...

We consider the sample average of a centered random walk in $\mathbb{R}^d$ with regularly varying step size distribution. For the first exit time from a compact convex set $A$ not containing the ori...

In this paper we consider a multidimensional random walk killed on leaving a right circular cone with a distribution of increments belonging to the normal domain of attraction of an $\alpha$-stable an...

We study a $d$-dimensional stochastic process $\mathbf{X}$ which arises from a L\'evy process $\mathbf{Y}$ by partial resetting, that is the position of the process $\mathbf{X}$ at a Poisson moment eq...

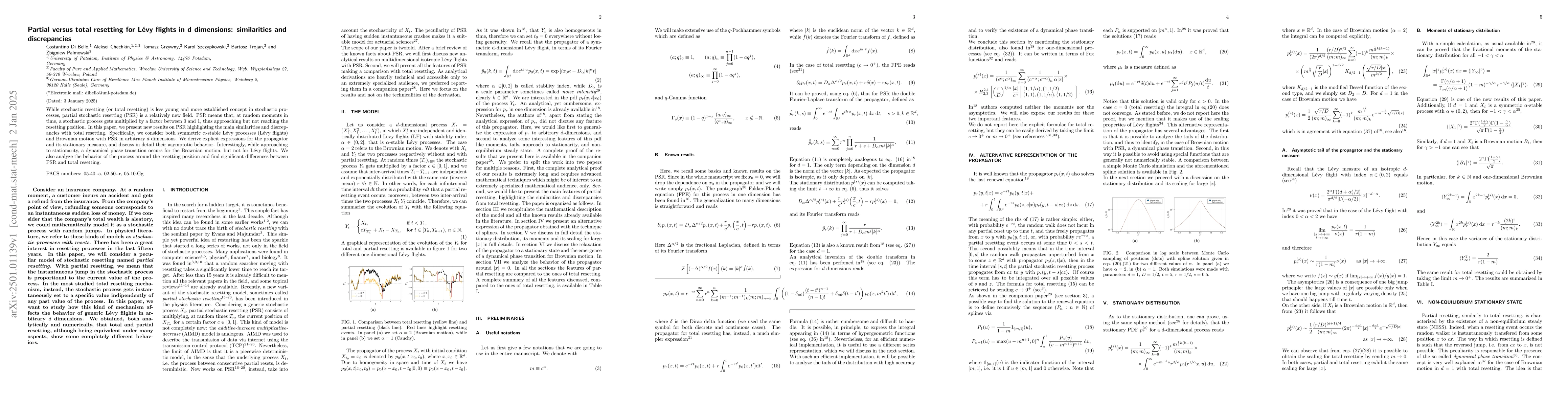

While stochastic resetting (or total resetting) is less young and more established concept in stochastic processes, partial stochastic resetting (PSR) is a relatively new field. PSR means that, at ran...

In this paper, we adopt the least squares Monte Carlo (LSMC) method to price time-capped American options. The aforementioned cap can be an independent random variable or dependent on asset price at r...

In this paper, we study finite-time ruin probabilities for the compound Markov binomial risk model - a discrete-time model where claim sizes are modulated by a finite-state ergodic Markov chain. In th...

This paper presents a derivation of the explicit price for the perpetual American put option in the Black-Scholes model, time-capped by the first drawdown epoch beyond a predefined level. We demonstra...

This paper presents a derivation of the explicit price for the perpetual American put option time-capped by the first drawdown epoch beyond a predefined level. We consider the market in which an asset...

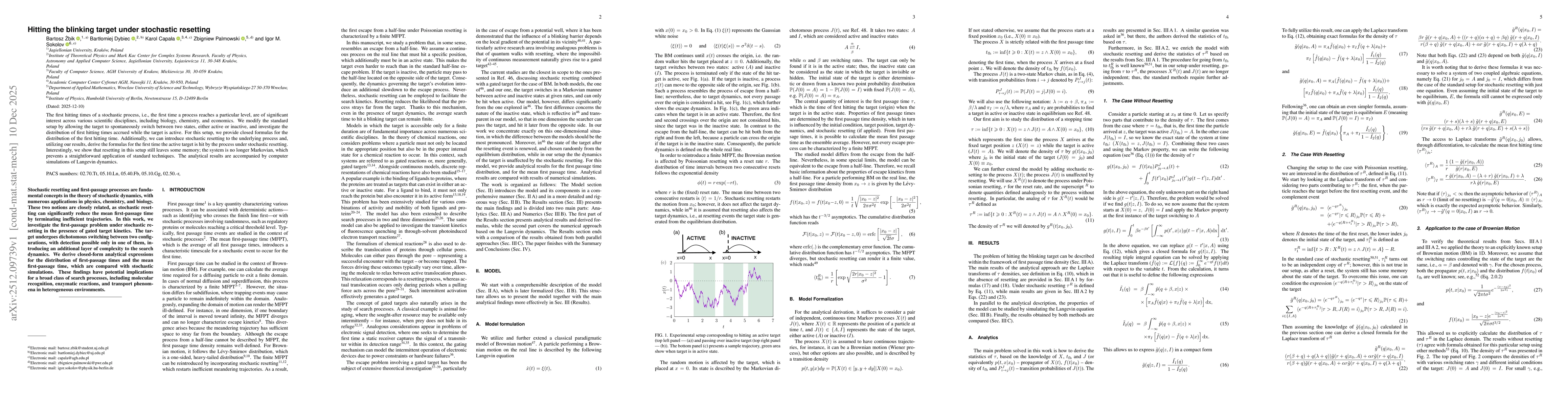

The first hitting times of a stochastic process, i.e., the first time a process reaches a particular level, are of significant interest across various scientific disciplines, including biology, chemis...

Emergency Department overcrowding is a critical issue that compromises patient safety and operational efficiency, necessitating accurate demand forecasting for effective resource allocation. This stud...

We establish results for the first sensitivity analysis of the stochastic fluid models (SFMs). We derive expressions for the sensitivity analysis of the key stationary and transient (time-dependent) q...

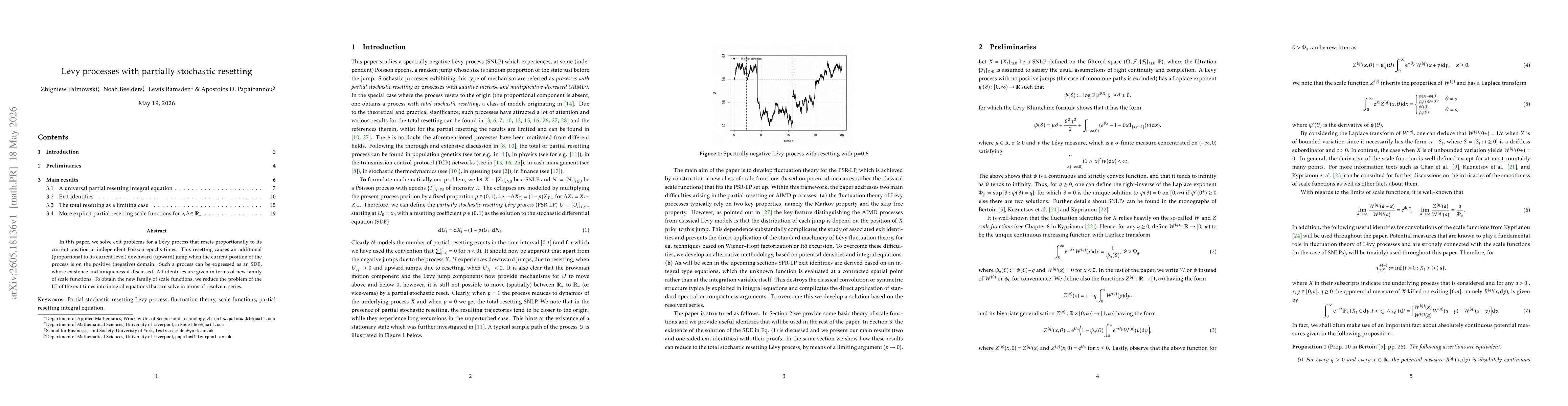

In this paper, we solve exit problems for a Lévy process that resets proportionally to its current position at independent Poisson epochs times. This resetting causes an additional (proportional to it...