Academic Profile

Statistics

Similar Authors

Papers on arXiv

We address the problem of testing conditional mean and conditional variance for non-stationary data. We build e-values and p-values for four types of non-parametric composite hypotheses with specifi...

We study an axiomatic framework for anonymized risk sharing. In contrast to traditional risk sharing settings, our framework requires no information on preferences, identities, private operations an...

The celebrated Expected Shortfall (ES) optimization formula implies that ES at a fixed probability level is the minimum of a linear real function plus a scaled mean excess function. We establish a r...

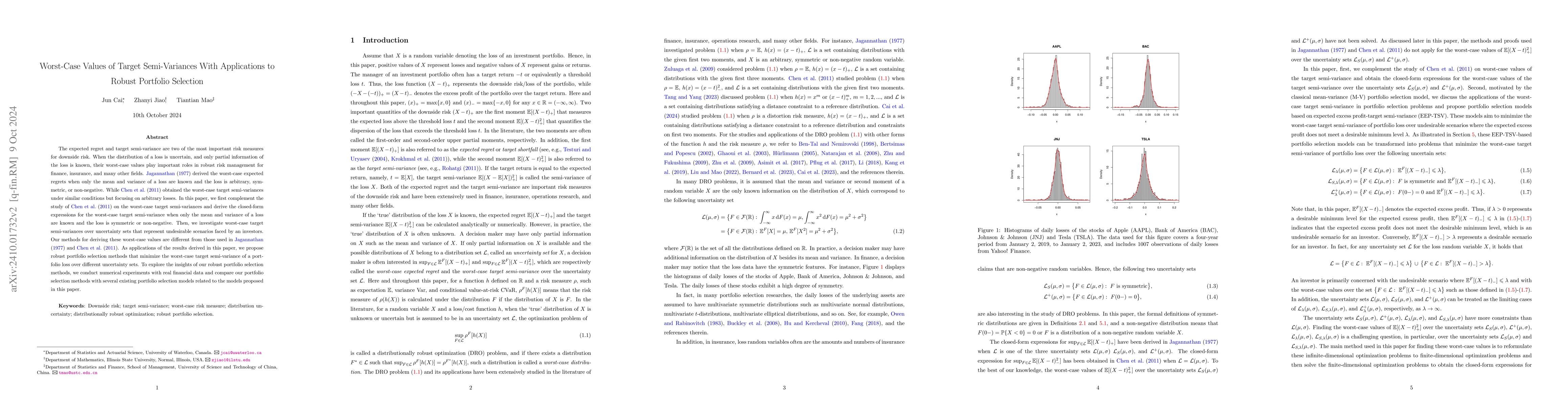

The expected regret and target semi-variance are two of the most important risk measures for downside risk. When the distribution of a loss is uncertain, and only partial information of the loss is kn...

Backtesting risk measures is a unique and important problem for financial regulators to evaluate risk forecasts reported by financial institutions. As a natural extension to standard (or traditional) ...